|

|

市場調査レポート

商品コード

1620481

ドライバー眠気モニタリングシステム市場の成長機会、成長促進要因、産業動向分析、2024~2032年予測Driver Drowsiness Monitoring System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 to 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ドライバー眠気モニタリングシステム市場の成長機会、成長促進要因、産業動向分析、2024~2032年予測 |

|

出版日: 2024年10月25日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

ドライバー眠気モニタリングシステムの世界市場は、2023年に26億米ドルの評価額に達し、交通安全への関心の高まりとドライバーの疲労に関連する事故発生率の増加が拍車をかけて、2024~2032年にかけてCAGR 9.8%で成長すると予測されています。

予防安全対策の重要性に対する意識の高まりにより、ドライバーの注意力を高め、事故リスクを低減するこれらのシステムの採用が急増しています。コンポーネントに基づき、市場はハードウェアとソフトウェアに分けられます。ハードウェアセグメントが大きなシェアを占め、2023年には14億米ドルを超えます。この成長は、最新の自動車に先進的カメラシステムが統合されたことが主因です。

先進的画像処理アルゴリズムと赤外線技術を搭載したこれらのカメラは、目の動き、まばたき速度、顔の合図を追跡し、眠気の兆候を正確に検出します。カメラ技術の絶え間ない革新、特に解像度や様々な照明条件下での性能が、これらのシステムの有効性を高めています。大手自動車部品メーカーは、多様な環境下で信頼性の高い動作を保証するため、高性能カメラソリューションの開発に多額の投資を行っています。車両別では、市場は乗用車と商用車に分けられます。

乗用車セグメントは、自動車の安全機能に対する消費者の意識の高まりに牽引され、2024~2032年にかけてCAGR 8%以上で成長すると予測されます。交通安全が消費者の最優先事項となる中、ドライバーの眠気モニタリングシステムは重要な安全機能として支持を集めています。特に中級車や高級車にADAS(先進運転支援システム)が広く採用されていることが、自動車メーカーが車両の差別化を図り、安全志向のイノベーションに対する需要の高まりに対応しようとしているため、この動向をさらに後押ししています。地域別では、北米が2023年の世界シェアの35%以上を占め、市場をリードしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2023年 |

| 予測年 | 2024~2032年 |

| 開始金額 | 26億米ドル |

| 予測金額 | 60億米ドル |

| CAGR | 9.8% |

この優位性は、この地域が最先端の自動車技術をいち早く採用し、強固な安全規制を設けていることに起因します。北米は研究開発に多額の投資を行っているため、ドライバーモニタリングの進歩が促進され、眠気検出技術の最前線に位置しています。さらに、交通安全に対する需要の高まりと商用車車両の拡大が、特にドライバーの注意力が重要な車両管理、物流、旅客輸送において、こうしたシステムの採用を加速させています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- サプライヤーの状況

- コンポーネントプロバイダー

- メーカー

- ソフトウェアプロバイダー

- 流通業者

- エンドユーザー

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- ケーススタディ

- 居眠り運転の事故と死亡者数の統計

- 規制状況

- 影響要因

- 促進要因

- 交通安全への関心の高まり

- ADAS採用の増加

- AIとMLの技術進歩

- 商用車の増加

- 産業の潜在的リスク・課題

- レガシー車両との統合

- データプライバシーとセキュリティへの懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

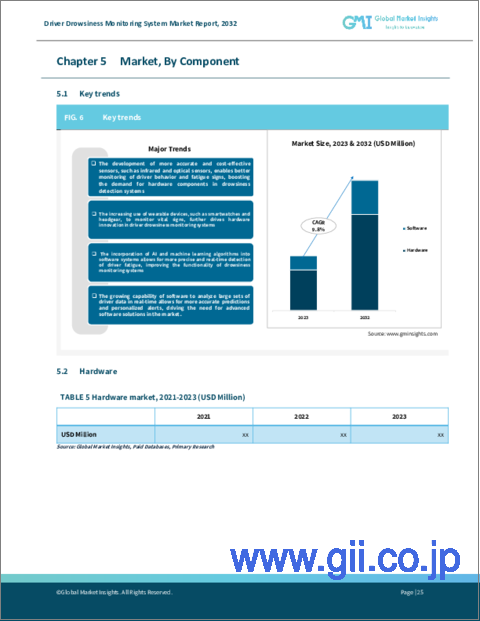

第5章 市場推定・予測:コンポーネント別、2021~2032年

- 主要動向

- ハードウェア

- センサー

- カメラ

- 電子制御ユニット(ECU)

- その他

- ソフトウェア

- 画像処理アルゴリズム

- 機械学習モデル

- データ分析プラットフォーム

- 統合ソフトウェア

- その他

第6章 市場推定・予測:車両別、2021~2032年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第7章 市場推定・予測:流通チャネル別、2021~2032年

- 主要動向

- OEM

- アフターマーケット

第8章 市場推定・予測:用途別、2021~2032年

- 主要動向

- 顔認識

- ステアリングパターンモニタリング

- 心拍数モニタリング

- その他

第9章 市場推定・予測:地域別、2021~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Aisin Seiki

- Aptiv

- Autoliv

- Continental

- Delphi Automotive

- Denso

- Faurecia

- General Motors

- Hella GmbH

- Magna International

- Mercedes-Benz

- Panasonic

- Robert Bosch

- Seeing Machines

- TRW Automotive

- Valeo

- Visteon

- Volkswagen

- Volvo Trucks

- ZF Friedrichshafen

The Global Driver Drowsiness Monitoring System Market reached a valuation of USD 2.6 billion in 2023 and is projected to grow at a CAGR of 9.8% from 2024 to 2032, spurred by a rising focus on road safety and the growing incidence of accidents linked to driver fatigue. Increased awareness of the importance of preventative safety measures has led to a surge in the adoption of these systems, as they enhance driver attentiveness and reduce accident risks. Based on component, the market is divided into hardware and software. The hardware segment held a significant share, exceeding USD 1.4 billion in 2023. This growth is largely due to the integration of sophisticated camera systems in modern vehicles.

Equipped with advanced image processing algorithms and infrared technology, these cameras track eye movements, blink rates, and facial cues to detect signs of drowsiness accurately. Continuous innovation in camera technology, especially around resolution and performance under varying lighting conditions, has elevated the effectiveness of these systems. Leading automotive suppliers are investing significantly in developing high-performance camera solutions to ensure reliable operation in diverse environments. In terms of vehicle type, the market is divided into passenger cars and commercial vehicles.

The passenger car segment is anticipated to grow at a CAGR of over 8% between 2024 and 2032, driven by increasing consumer awareness about vehicle safety features. With road safety becoming a top priority for consumers, driver drowsiness monitoring systems have gained traction as a key safety feature. The widespread adoption of Advanced Driver Assistance Systems (ADAS), especially in mid-range and premium passenger vehicles, has further supported this trend, as automotive manufacturers aim to differentiate their vehicles and respond to rising demand for safety-oriented innovations. Regionally, North America led the market in 2023 with over 35% of the global share.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $2.6 Billion |

| Forecast Value | $6 Billion |

| CAGR | 9.8% |

This dominance is attributed to the region's early adoption of cutting-edge automotive technologies and robust safety regulations. North America's substantial investment in research and development has facilitated advancements in driver monitoring, placing it at the forefront of drowsiness detection technology. Additionally, the increasing demand for road safety and the expanding commercial vehicle fleet have accelerated the adoption of these systems, especially in fleet management, logistics, and passenger transport, where driver alertness is crucial.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 Manufacturers

- 3.2.3 Software providers

- 3.2.4 Distributors

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Case study

- 3.7 Statistics of drowsy driving crashes and fatalities

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing focus on road safety

- 3.9.1.2 Rising adoption of ADAS

- 3.9.1.3 Technological advancement in AI and ML

- 3.9.1.4 Growing commercial vehicle fleet

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Integration with legacy vehicles

- 3.9.2.2 Data privacy and security concerns

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2032 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.2 Cameras

- 5.2.3 Electronic control units (ECUs)

- 5.2.4 Others

- 5.3 Software

- 5.3.1 Image processing algorithms

- 5.3.2 Machine learning models

- 5.3.3 Data analytics platforms

- 5.3.4 Integration software

- 5.3.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2032 ($Bn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2032 ($Bn)

- 7.1 Key trends

- 7.2 OEMs

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2032 ($Bn)

- 8.1 Key trends

- 8.2 Facial recognition

- 8.3 Steering pattern monitoring

- 8.4 Heart rate monitoring

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2032 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aisin Seiki

- 10.2 Aptiv

- 10.3 Autoliv

- 10.4 Continental

- 10.5 Delphi Automotive

- 10.6 Denso

- 10.7 Faurecia

- 10.8 General Motors

- 10.9 Hella GmbH

- 10.10 Magna International

- 10.11 Mercedes-Benz

- 10.12 Panasonic

- 10.13 Robert Bosch

- 10.14 Seeing Machines

- 10.15 TRW Automotive

- 10.16 Valeo

- 10.17 Visteon

- 10.18 Volkswagen

- 10.19 Volvo Trucks

- 10.20 ZF Friedrichshafen