|

市場調査レポート

商品コード

1721544

ガス給湯器の市場機会、成長促進要因、産業動向分析、2025~2034年予測Gas Water Heater Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ガス給湯器の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月08日

発行: Global Market Insights Inc.

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

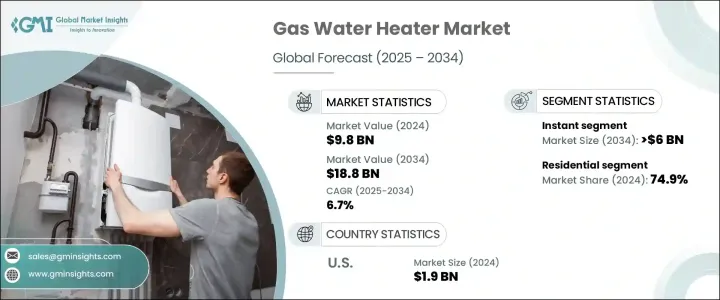

ガス給湯器の世界市場は、2024年には98億米ドルと評価され、CAGR 6.7%で成長し、2034年には188億米ドルに達すると推定されています。

この成長には、性能、利便性、持続可能性を兼ね備えた高効率暖房システムに対する消費者需要の高まりが大きく寄与しています。家庭や商業施設がますます環境に配慮したソリューションにシフトする中、ガス給湯器は、電気代替品に比べて運用コストが低く、二酸化炭素排出量を削減できる点で際立っています。エネルギー規制が厳しくなり、光熱費が変動する中、ガス給湯器の魅力はますます高まっています。加えて、スマートシティや都市型住宅プロジェクト、環境意識の高いコミュニティーの増加により、持続可能性の目標とエネルギー効率の義務付けの両方を満たす次世代機器の採用が後押しされています。

今日の消費者が求めているのは、オンデマンドの温水だけではないです。消費者が求めているのは、スマートで応答性が高く、使いやすい家電製品なのです。このような期待が、ガス給湯器の展望を再構築しています。Wi-Fi接続、音声アシスト、遠隔操作機能を提供するシステムが、現在、主導権を握っています。簡素化された温度調整やリアルタイムの診断アラートなど、使い勝手の向上はもはやオプションではなく、必要不可欠なものとなっています。製品開発は、高度な制御、自動化、ホーム・エコシステムとのシームレスな統合へとシフトしています。その結果、メーカー各社は、日常生活を向上させる信頼性と直感性を備えたシステムを提供するため、技術革新を優先しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 98億米ドル |

| 予測金額 | 188億米ドル |

| CAGR | 6.7% |

持続可能な建設とスマートビルディングの動向は、低排出ガスで高性能のガス給湯器の需要を引き続き牽引しています。これらの製品は、環境規制と現代の消費者の嗜好の両方に合致しています。天然ガスインフラが広く利用可能であることが、特に天然ガスが電気よりもコスト効率に優れている地域での市場拡大をさらに後押ししています。停電が頻繁に起こる地域では、ガス給湯器は信頼できる給湯源として機能し、市場の関連性を高めています。

製品別では、市場は瞬間式給湯器と貯湯式給湯器に区分されます。瞬間式ガス給湯器は急速に普及しており、2034年までに60億米ドルの売上が見込まれています。消費者は、省スペース設計、高速加熱、省エネ機能に惹かれています。柔軟な容量オプションと手頃な価格設定が、さらに人気を後押ししています。グリーン・インフラ・プロジェクト(新築と改修の両方)は、特にエネルギー効率の高い認証を目指す住宅開発において、採用を加速させています。

2024年には住宅セグメントが74.9%と圧倒的なシェアを占め、省エネ、暖房費低減、安定した性能からガス給湯器を選ぶ住宅所有者が増えています。ゼロ・エミッション住宅開発の台頭がこのシフトを強めています。漏水検知、スマート・モニタリング、タッチスクリーン、音声作動制御などの機能が、これらのシステムをさらに魅力的なものにしています。

北米のシェアは25%で、米国は2024年に19億米ドルを生み出します。環境意識の高まりとエネルギー規制の強化が、メーカーに低排出材料とスマートオートメーションによる技術革新を促しています。Noritz Corporation、Bosch Thermotechnology Corp.、Haier Inc.、A.O.Smithなどの大手企業は、Wi-Fi対応、アプリ制御、音声作動モデルを発表するために研究開発に多額の投資を行っています。これらの進歩は、エネルギー効率とユーザー・エクスペリエンスにおいて新たなベンチマークを設定しつつあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- イノベーションとテクノロジーの情勢

- 企業の市場シェア

第5章 市場規模・予測:製品別、2021 –2034

- 主要動向

- インスタント

- ストレージ

第6章 市場規模・予測:容量別、2021 –2034

- 主要動向

- 30リットル以下

- 30~100リットル

- 100~250リットル

- 250~400リットル

- 400リットル以上

第7章 市場規模・予測:用途別、2021 –2034

- 主要動向

- 住宅用

- 商業用

- 大学

- オフィス

- 政府/建物

- その他

第8章 市場規模・予測:燃料別、2021 –2034

- 主要動向

- 天然ガス

- LPG

第9章 市場規模・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- オーストリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- ユーラシア

- ロシア

- ベラルーシ

- カザフスタン

- キルギスタン

- アルメニア

- CIS

- アゼルバイジャン

- モルドバ

- タジキスタン

- トルクメニスタン

- ウズベキスタン

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- オマーン

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

- メキシコ

第10章 企業プロファイル

- American Water Heater

- Ariston Thermo

- A. O. Smith

- BDR Thermea Group

- Bosch Thermotechnology Corp.

- Bradford White Corporation

- FERROLI S.p.A

- Hubbell Heaters

- Havells India Ltd.

- Haier Inc.

- Lennox International Inc.

- Noritz Corporation

- Parker Boiler Company

- Rheem Manufacturing Company

- Rinnai America Corporation

- State Industries

- Vaillant

- Westinghouse Electric Corporation

The Global Gas Water Heater Market was valued at USD 9.8 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 18.8 billion by 2034. This growth is largely fueled by rising consumer demand for high-efficiency heating systems that combine performance, convenience, and sustainability. As households and commercial facilities increasingly shift toward environmentally responsible solutions, gas water heaters stand out for their lower operational costs and reduced carbon footprint compared to electric alternatives. With energy regulations getting stricter and utility prices fluctuating, the appeal of gas-powered systems continues to strengthen. In addition, the growing number of smart cities, urban housing projects, and eco-conscious communities are supporting the adoption of next-gen appliances that meet both sustainability goals and energy-efficiency mandates.

Consumers today expect more than just hot water on demand. They want appliances that are smart, responsive, and easy to use. This expectation is reshaping the gas water heater landscape. Systems that offer Wi-Fi connectivity, voice assistance, and remote control features are now leading the charge. Enhanced usability, such as simplified temperature adjustments and real-time diagnostic alerts, is no longer optional-it's essential. Product development is shifting toward advanced controls, automation, and seamless integration with home ecosystems. As a result, manufacturers are prioritizing innovation to deliver reliable, intuitive systems that enhance everyday living.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.8 Billion |

| Forecast Value | $18.8 Billion |

| CAGR | 6.7% |

The trend toward sustainable construction and smart buildings continues to drive demand for low-emission, high-performance gas water heaters. These products align with both environmental regulations and modern consumer preferences. The widespread availability of natural gas infrastructure further supports market expansion, especially in regions where natural gas remains more cost-effective than electricity. In areas with frequent power disruptions, gas water heaters serve as a dependable source of hot water, reinforcing their market relevance.

By product, the market is segmented into instant and storage water heaters. Instant gas water heaters are rapidly gaining traction, with the segment expected to generate USD 6 billion by 2034. Consumers are drawn to their space-saving design, faster heating, and energy-saving capabilities. Flexible capacity options and affordable pricing further boost their popularity. Green infrastructure projects-both new builds and retrofits-are accelerating adoption, especially in residential developments aiming for energy-efficient certifications.

The residential segment accounted for a dominant 74.9% share in 2024, with more homeowners opting for gas water heaters due to their energy savings, lower heating costs, and consistent performance. The rise of zero-emission housing developments is reinforcing this shift. Features like leak detection, smart monitoring, touchscreens, and voice-activated controls make these systems even more attractive.

North America held a 25% share, with the U.S. generating USD 1.9 billion in 2024. Growing environmental awareness and tighter energy regulations are pushing manufacturers to innovate with low-emission materials and smart automation. Leading players such as Noritz Corporation, Bosch Thermotechnology Corp., Haier Inc., and A. O. Smith are investing heavily in R&D to introduce Wi-Fi-enabled, app-controlled, and voice-activated models. These advancements are setting new benchmarks in energy efficiency and user experience.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

- 4.4 Company market share

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 Instant

- 5.3 Storage

Chapter 6 Market Size and Forecast, By Capacity, 2021 – 2034 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Below 30 liters

- 6.3 30 – 100 liters

- 6.4 100 – 250 liters

- 6.5 250 – 400 liters

- 6.6 >400 liters

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.3.1 College/University

- 7.3.2 Offices

- 7.3.3 Government/Building

- 7.3.4 Others

Chapter 8 Market Size and Forecast, By Fuel, 2021 – 2034 (USD Million & ‘000 Units)

- 8.1 Key trends

- 8.2 Natural gas

- 8.3 LPG

Chapter 9 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Germany

- 9.3.4 Italy

- 9.3.5 Austria

- 9.3.6 Spain

- 9.3.7 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 India

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.5 Eurasia

- 9.5.1 Russia

- 9.5.2 Belarus

- 9.5.3 Kazakhstan

- 9.5.4 Kyrgyzstan

- 9.5.5 Armenia

- 9.6 CIS

- 9.6.1 Azerbaijan

- 9.6.2 Moldova

- 9.6.3 Tajikistan

- 9.6.4 Turkmenistan

- 9.6.5 Uzbekistan

- 9.7 Middle East & Africa

- 9.7.1 Saudi Arabia

- 9.7.2 UAE

- 9.7.3 Qatar

- 9.7.4 Kuwait

- 9.7.5 Oman

- 9.8 Latin America

- 9.8.1 Brazil

- 9.8.2 Argentina

- 9.8.3 Chile

- 9.8.4 Mexico

Chapter 10 Company Profiles

- 10.1 American Water Heater

- 10.2 Ariston Thermo

- 10.3 A. O. Smith

- 10.4 BDR Thermea Group

- 10.5 Bosch Thermotechnology Corp.

- 10.6 Bradford White Corporation

- 10.7 FERROLI S.p.A

- 10.8 Hubbell Heaters

- 10.9 Havells India Ltd.

- 10.10 Haier Inc.

- 10.11 Lennox International Inc.

- 10.12 Noritz Corporation

- 10.13 Parker Boiler Company

- 10.14 Rheem Manufacturing Company

- 10.15 Rinnai America Corporation

- 10.16 State Industries

- 10.17 Vaillant

- 10.18 Westinghouse Electric Corporation