脊椎固定装置市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Spinal Fusion Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801935

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

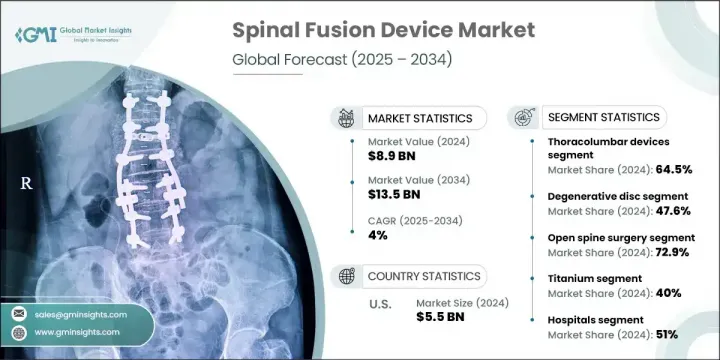

世界の脊椎固定装置市場は2024年に89億米ドルと評価され、CAGR 4%で成長し、2034年には135億米ドルに達すると推定されています。

市場の上昇の勢いは、脊椎疾患の増加、対象患者の増加、より高度で低侵襲な固定術を開発するための研究開発への継続的な投資によって後押しされています。前向きな見通しとは裏腹に、いくつかの新興国では償還の選択肢が限られており、市場の本格的な拡大には課題が残る。とはいえ、脊椎外科手術の進歩や世界の高齢化率の上昇は、引き続き需要を高めています。特に術中画像診断、ロボット工学、ナビゲーションなどの技術進化は、手術合併症の軽減と治療成績の向上に役立っています。

胸腰椎デバイスセグメントは2024年に64.5%のシェアを占めたが、これは胸椎と腰椎の両方で外科的安定化を必要とする腰椎変性疾患や脊椎損傷の頻度が高いためです。このセグメントの成長は、高齢者における衝撃性の高い外傷や脊椎変性の割合が増加していることが大きな要因となっています。さらに、脊椎骨折や脊椎すべり症のような症状には、安定性と回復を向上させる精密工学機器が使用されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 89億米ドル |

| 予測金額 | 135億米ドル |

| CAGR | 4% |

2024年には、椎間板変性疾患分野が47.6%のシェアを占める。この優位性は、加齢に伴う椎間板変性症例の急増と、侵襲性の低い脊椎固定術の幅広い採用によるものです。椎間板関連の問題を経験する高齢者が増えるにつれ、効率的で低リスクの治療に対するニーズは高まり続けています。早期発見、患者の意識、低侵襲手術への信頼の高まりも、このセグメントの業績を押し上げる上で重要な役割を果たしています。

米国の脊椎固定装置市場規模は2024年に55億米ドルとなり、この成長は、革新的な手術ツールや手技が広く受け入れられていることに加え、高齢者患者の増加や脊椎疾患の負担が大きいことに起因しています。この地域は、強固なヘルスケアシステム、高度な手術インフラ、最新の脊椎インプラントとナビゲーションシステムの好意的な採用から利益を得ています。2021年の市場規模は42億米ドル、2022年には47億米ドルとなり、臨床需要と技術向上により毎年着実に増加しています。

世界脊椎固定装置市場のトップ企業は、Stryker、Globus Medical、Medtronic、NuVasive、DePuy Synthesなどです。市場プレゼンスを強化するため、脊椎固定装置の主要メーカーはロボット支援手術、AI搭載ナビゲーションシステム、低侵襲製品開発に多額の投資を行っています。これらの企業は、研究開発や的を絞った買収を通じて製品ポートフォリオを拡大し、エンド・ツー・エンドの脊椎ソリューションを提供しています。また、病院や手術センターとの戦略的パートナーシップにより、先進機器の迅速な導入が可能になっています。いくつかの企業は、高成長市場により良いサービスを提供するため、生産の現地化と販売網の強化を進めています。継続的な外科医トレーニングプログラムとデジタルプラットフォームの統合により、地域全体で手術の精度と導入率がさらに向上しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 脊椎疾患の有病率の増加

- 技術的進歩

- 外傷および傷害件数の増加

- 高齢化人口の増加と低侵襲手術の需要の高まり

- 業界の潜在的リスク&課題

- 厳しい規制シナリオ

- 脊椎手術の高額な費用

- 市場機会

- 外来手術センター(ASC)の成長

- ロボット手術やナビゲーション支援手術の導入増加

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 現在の技術動向

- ナビゲーションシステムとロボットシステムの統合

- PEEKおよびチタンケージの普及

- 新興技術

- 3Dプリンティングと脊椎インプラントの進歩

- センサー統合型スマートインプラント

- 現在の技術動向

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

- バリューチェーン分析

- 償還シナリオ

- 消費者行動分析

- 比較分析:前方アプローチと後方アプローチ

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 胸腰椎デバイス

- 椎弓根スクリュー

- 椎間体固定装置(IBFD)

- ロッド

- プレート

- その他の胸腰椎デバイス

- 頸椎固定装置

- 椎間体固定装置(IBFD)

- プレート

- ロッド

- フック

- その他の頸部デバイス

第6章 市場推計・予測:疾患タイプ別、2021年~2034年

- 主要動向

- 変性椎間板

- 脊椎変形

- 外傷と骨折

- 脊椎腫瘍

- その他の病気の種類

第7章 市場推計・予測:手術別、2021年~2034年

- 主要動向

- 開胸脊椎手術

- 低侵襲脊椎手術

第8章 市場推計・予測:材料タイプ別、2021年~2034年

- 主要動向

- チタン

- ポリエーテルエーテルケトン(PEEK)

- コバルトクロム

- ステンレス鋼

- その他の材料

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- 整形外科クリニック

- その他の用途

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- ATEC

- B. Braun

- Captiva Spine

- ChoiceSpine

- DePuy Synthes

- Globus Medical

- K2M

- Life Spine

- Medtronic

- NuVasive

- Orthofix

- Premia Spine

- Stryker

- Xtant Medical

- Zimmer Biomet

目次

The Global Spinal Fusion Device Market was valued at USD 8.9 billion in 2024 and is estimated to grow at a CAGR of 4% to reach USD 13.5 billion by 2034. The market's upward momentum is fueled by the rising number of spinal disorders, a growing pool of target patients, and ongoing investments in R&D to develop more advanced and minimally invasive fusion procedures. Despite the positive outlook, limited reimbursement options in several emerging countries remain a challenge for full market scalability. Nevertheless, advancements in spinal surgery and the rise in aging populations worldwide continue to elevate demand. Technological evolution, particularly in intraoperative imaging, robotics, and navigation, is helping reduce surgical complications and improve outcomes.

The thoracolumbar devices segment held 64.5% share in 2024, owing to the high frequency of lumbar degenerative disorders and spinal injuries that necessitate surgical stabilization in both the thoracic and lumbar spine. Growth in this segment is largely driven by increasing rates of high-impact trauma and spine degeneration among older adults. Additionally, conditions like spinal fractures and spondylolisthesis are being addressed with precision-engineered devices to improve stability and recovery.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.9 Billion |

| Forecast Value | $13.5 Billion |

| CAGR | 4% |

In 2024, the degenerative disc disorder segment held a 47.6% share. This dominance is attributed to a surge in cases of age-related disc degeneration and the broader adoption of less invasive spinal fusion methods. As more elderly individuals experience disc-related issues, the need for efficient, lower-risk treatment continues to climb. Earlier detection, patient awareness, and growing trust in minimally invasive procedures also play vital roles in boosting the segment's performance.

US Spinal Fusion Device Market generated USD 5.5 billion in 2024. This growth stems from an increasing number of geriatric patients and a high burden of spinal disorders, along with broader acceptance of innovative surgical tools and techniques. The region benefits from a robust healthcare system, advanced surgical infrastructure, and favorable adoption of modern spinal implants and navigation systems. The market was valued at USD 4.2 billion in 2021 and USD 4.7 billion in 2022, showing steady annual increases fueled by clinical demand and technological improvements.

Top companies in the Global Spinal Fusion Device Market include Stryker, Globus Medical, Medtronic, NuVasive, and DePuy Synthes. To strengthen their market presence, leading spinal fusion device manufacturers are investing heavily in robotic-assisted surgery, AI-powered navigation systems, and minimally invasive product development. These firms are expanding their product portfolios through R&D and targeted acquisitions to offer end-to-end spinal solutions. Strategic partnerships with hospitals and surgical centers are also enabling quicker adoption of advanced devices. Several companies are localizing production and strengthening distribution networks to better serve high-growth markets. Continuous surgeon training programs and digital platform integration are further enhancing procedural precision and adoption rates across geographies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Disease type trends

- 2.2.3 Surgery trends

- 2.2.4 Material type trends

- 2.2.5 End use trends

- 2.2.6 Region trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of spinal diseases

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rise in number of trauma and injury cases

- 3.2.1.4 Rising geriatric population coupled with high demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 High cost of spinal procedures

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of ambulatory surgical centers (ASCs)

- 3.2.3.2 Increasing adoption of robotic and navigation-assisted surgery

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Integration of navigation and robotic systems

- 3.5.1.2 Widespread use of PEEK and titanium cages

- 3.5.2 Emerging technologies

- 3.5.2.1 3D Printing, and advances in spinal implants

- 3.5.2.2 Smart implants with sensor integration

- 3.5.1 Current technological trends

- 3.6 Future market trends

- 3.7 Spinal Fusion Device Market, By Region, 2021 - 2034 (Units)

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 Middle East and Africa

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Value chain analysis

- 3.12 Reimbursement scenario

- 3.13 Consumer behaviour analysis

- 3.14 Comparative analysis: anterior Vs posterior surgical approach

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Thoracolumbar devices

- 5.2.1 Pedicle screws

- 5.2.2 Intervertebral body fusion device (IBFD)

- 5.2.3 Rods

- 5.2.4 Plates

- 5.2.5 Other thoracolumbar devices

- 5.3 Cervical fixation devices

- 5.3.1 Intervertebral body fusion device (IBFD)

- 5.3.2 Plates

- 5.3.3 Rods

- 5.3.4 Hooks

- 5.3.5 Other cervical devices

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Degenerative disc

- 6.3 Spinal deformity

- 6.4 Trauma and fractures

- 6.5 Spinal tumors

- 6.6 Other disease types

Chapter 7 Market Estimates and Forecast, By Surgery, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Open spine surgery

- 7.3 Minimally invasive spine surgery

Chapter 8 Market Estimates and Forecast, By Material Type, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Titanium

- 8.3 Polyether ether ketone (PEEK)

- 8.4 Cobalt chrome

- 8.5 Stainless steel

- 8.6 Other materials

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Orthopedic clinics

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ATEC

- 11.2 B. Braun

- 11.3 Captiva Spine

- 11.4 ChoiceSpine

- 11.5 DePuy Synthes

- 11.6 Globus Medical

- 11.7 K2M

- 11.8 Life Spine

- 11.9 Medtronic

- 11.10 NuVasive

- 11.11 Orthofix

- 11.12 Premia Spine

- 11.13 Stryker

- 11.14 Xtant Medical

- 11.15 Zimmer Biomet

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日