データセンター相互接続市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Data Center Interconnect Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 320 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801929

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

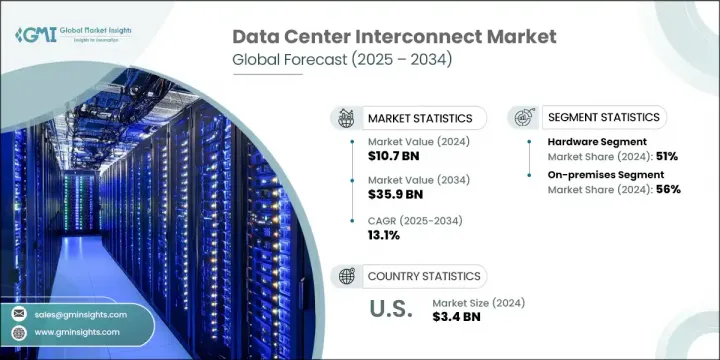

世界のデータセンター相互接続市場の2024年の市場規模は107億米ドルで、CAGR 13.1%で成長し、2034年には359億米ドルに達すると推定されています。

デジタルトランスフォーメーションが加速し、データ量が急増し続ける中、高度な相互接続ソリューションの必要性が重要になっています。ハイブリッドクラウド戦略やAI駆動アプリケーションの台頭により、高速でプログラマブルな光ネットワークに焦点が移っています。企業は、データセンター間の低遅延、スケーラブル、セキュアなデータ転送を確保するため、400Gや800Gの光ソリューションに急速に移行しています。これらの技術は、適応的な帯域幅制御、暗号化機能、待ち時間の最適化を提供します。

競合他社との差別化には、インテントベースのネットワーキング、高度な自動化、企業やクラウドネイティブのクライアントに合わせた段階的なサービスモデルが必要です。プロバイダーは、リアルタイムの遠隔測定、SLA追跡、ネットワーク・プログラマビリティを備えたインテリジェントなDCIソリューションを提供し、インフラをコンプライアンス基準や重要なワークロードに適合させています。北米は、高密度のクラウドインフラ、堅牢なインターネットエクスチェンジ、大規模なハイパースケールデプロイメントに支えられ、DCIをリードし続けています。国境を越えた光ファイバー接続と洗練された光バックボーンにより、この地域は依然としてこの市場の革新と拡大の焦点となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 107億米ドル |

| 予測金額 | 359億米ドル |

| CAGR | 13.1% |

2024年、ハードウェア・セグメントのシェアは51%で、2034年までのCAGRは12%と予測されます。物理インフラは依然としてDCI実装のバックボーンであり、施設間の信頼性の高い高速データ移動を可能にします。光トランシーバ、ルータ、マルチプレクサ、スイッチなどのコアコンポーネントは、特に400Gや800Gのコヒレントオプティクスをサポートするものへの需要が高まっています。これらのエレメントは、クラウドコンピューティング、人工知能、IoTのユースケースに欠かせないが、データセンタ投資の大部分を占めています。

オンプレミスセグメントは、2024年に56%のシェアでDCI市場をリードし、2025~2034年のCAGRは12%で成長すると予測されています。オンプレミス型では、ハイパースケーラや企業がネットワーク環境を直接制御できるため、ミッションクリティカルで低遅延なアプリケーションに不可欠です。また、このような構成では、AIモデルのトレーニング、金融アルゴリズム、科学的コンピューティングなど、計算集約的なオペレーションに対して、より高度なカスタマイズとパフォーマンスの最適化が可能になります。さらに、政府機関、BFSI、ヘルスケアなどの業界では、厳格な規制要件やデータレジデンシー要件を満たすため、オンプレミスのDCIが引き続き好まれています。

米国データセンター相互接続市場は2024年に34億米ドルを生み出し、北米市場の約85%を占める。デジタルインフラにおける同国のリーダーシップは、ハイパースケール・プロバイダー、エンタープライズ・データセンター、コロケーション施設の大きな存在によって牽引されています。ヘルスケア、eコマース、金融などの主要産業では、メトロネットワークや地域ネットワーク間の高速相互接続に対する需要が引き続き高いです。米国はまた、400Gや800Gの光技術へのアップグレードやオープンネットワーキング標準の採用でも最先端を走っており、全米でのDCI展開をさらに加速させています。

世界データセンター相互接続市場の主要企業は、アリスタネットワークス、ファーウェイ、シスコ、富士通、ノキア、エクストリームネットワークス、ジュニパーなどです。データセンター相互接続市場のトップ企業は、市場での地位を確固たるものにするため、技術革新、拡張性、ネットワークインテリジェンスに注力しています。主要ベンダーは、増大するデータ需要に対応するため、400G/800G技術をサポートする大容量光トランスポートシステムに投資しています。ハイパースケールクラウドプロバイダーとの戦略的パートナーシップは、ソリューションの範囲を拡大し、相互運用性を向上させています。企業はAIと遠隔測定ツールを統合し、リアルタイム分析、SLAコンプライアンス、自動ネットワーク調整を実現しています。柔軟性と迅速な展開を確保するため、モジュラー・ハードウェアとソフトウェア定義のソリューションが開発されています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- AIと機械学習のワークロードの増加

- 急速なクラウド導入とエッジコンピューティングの拡大

- 世界のデータトラフィックとストレージ需要の急増

- ハイパースケールデータセンターの導入増加

- 業界の潜在的リスク&課題

- DCIインフラストラクチャの初期資本支出が高額です

- 複雑なネットワーク管理と統合の問題

- 市場機会

- AIに最適化されたDCIプラットフォームの開発

- 5Gとエッジデータセンターの導入拡大

- 新興市場におけるデジタルインフラの拡大

- エネルギー効率が高く環境に優しいDCIソリューションの需要の高まり

- 促進要因

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許分析

- 価格動向と経済分析

- 歴史的な価格分析と市場の進化(2019-2024)

- 現在のDCIの価格情勢(2024-2025)

- 総所有コスト(TCO)と経済分析

- 将来の価格予測と市場動向(2025-2034)

- DCIネットワークアーキテクチャとトポロジ設計

- ネットワークトポロジモデルと設計原則

- ポイントツーポイントDCIアーキテクチャ

- ハブアンドスポーク型DCIモデル

- メッシュとany-to-any接続

- ハイブリッドおよびマルチトポロジ設計

- 距離ベースのDCIソリューションアーキテクチャ

- メトロDCI(0~100km)ソリューション

- 地域DCI(100~1000km)ソリューション

- 長距離DCI(1000km以上)ソリューション

- アプリケーション固有のDCIアーキテクチャ

- クラウドプロバイダーのDCIアーキテクチャ

- エンタープライズDCIアーキテクチャ

- 金融サービスDCIアーキテクチャ

- ネットワークトポロジモデルと設計原則

- DCI容量管理とパフォーマンス最適化

- ネットワーク容量の計画と管理

- パフォーマンス監視と分析

- サービス品質とトラフィック管理

- ユースケース

- エネルギー効率と持続可能性

- DCIネットワークにおけるエネルギー消費分析

- グリーンネットワーキングと持続可能性の取り組み

- エネルギー効率技術とイノベーション

- 持続可能性のROIとビジネス上のメリット

- 最良のシナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- 光トランシーバー

- スイッチとルーター

- ケーブルとコネクタ

- 光増幅器

- その他

- ソフトウェア

- ソフトウェア定義ネットワーク(SDN)

- ネットワーク管理ソフトウェア

- 分析および最適化ソフトウェア

- その他

- サービス

- プロ

- 管理

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 同期光ネットワーク(SONET)

- 高密度波長分割多重(DWDM)

- イーサネット

- 光伝送ネットワーク(OTN)

- その他

第7章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- クラウドベース

- オンプレミス

- ハイブリッド

第8章 市場推計・予測:帯域幅別、2021年~2034年

- 主要動向

- 低帯域幅(最大1 Gbps)

- 中帯域幅(1~10 Gbps)

- 高帯域幅(10~100 Gbps)

- 超高帯域幅(100 Gbps以上)

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 災害復旧

- コンテンツ配信

- データ複製

- 負荷分散

- クラウド接続

第10章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 通信サービスプロバイダー(CSP)

- インターネットコンテンツプロバイダーおよびキャリア中立プロバイダー(ICP/CNP)

- 政府

- 企業

- BFSI

- ヘルスケア

- メディア&エンターテイメント

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- 北欧諸国

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- フィリピン

- インドネシア

- シンガポール

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- 世界企業

- ADVA Optical Networking

- Arista Networks

- Broadcom

- Ciena

- Cisco

- Fujitsu

- Huawei

- IBM

- Infinera

- Juniper

- Nokia

- ZTE

- 地域企業

- Brocade Communication Systems

- Colt Technology Services

- CoreSite Realty

- Digital Realty Trust

- Evoque Data Center Solutions

- Fiber Mountain

- Flexential

- Megaport

- Zayo Group

- 新興企業

- Cologix

- Cyxtera Technologies

- Dolphin Interconnect Solutions

- Ekinops

- Eoptolink

- Innolight

- Macom Technology Solutions

- Pluribus Networks

- XKL

目次

The Global Data Center Interconnect Market was valued at USD 10.7 billion in 2024 and is estimated to grow at a CAGR of 13.1% to reach USD 35.9 billion by 2034. As digital transformation accelerates and data volumes continue to surge, the need for advanced interconnect solutions becomes critical. The rise of hybrid cloud strategies and AI-driven applications has shifted focus toward high-speed, programmable optical networks. Enterprises are rapidly moving to 400G and 800G optical solutions to ensure low-latency, scalable, and secure data transfers between data centers. These technologies offer adaptive bandwidth control, encryption capabilities, and latency optimization.

Competitive differentiation now requires intent-based networking, advanced automation, and tiered service models tailored to enterprise and cloud-native clients. Providers are offering intelligent DCI solutions with real-time telemetry, SLA tracking, and network programmability, aligning infrastructure with compliance standards and critical workloads. North America continues to lead the DCI landscape, supported by dense cloud infrastructure, robust internet exchanges, and large-scale hyperscale deployments. With cross-border fiber connectivity and sophisticated optical backbones, the region remains a focal point for innovation and expansion in this market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.7 Billion |

| Forecast Value | $35.9 Billion |

| CAGR | 13.1% |

In 2024, the hardware segment accounted for 51% share and is expected to grow at a CAGR of 12% through 2034. Physical infrastructure remains the backbone of DCI implementations, enabling reliable and high-speed data movement between facilities. Core components like optical transceivers, routers, multiplexers, and switches are seeing increased demand-especially those supporting 400G and 800G coherent optics. These elements are vital for powering cloud computing, artificial intelligence, and IoT use cases, although they also command a significant portion of data center investment.

The on-premises segment led the DCI market in 2024 with 56% share and is anticipated to grow at a CAGR of 12% during 2025-2034. On-premise deployments offer hyperscalers and enterprises direct control over their networking environment, which is essential for mission-critical, low-latency applications. These configurations also allow deeper customization and performance optimization for compute-intensive operations such as AI model training, financial algorithms, and scientific computing. Moreover, industries like government, BFSI, and healthcare continue to prefer on-premise DCI to meet strict regulatory and data residency requirements.

United States Data Center Interconnect Market generated USD 3.4 billion in 2024, capturing around 85% of the North American market. The country's leadership in digital infrastructure is driven by its large presence of hyperscale providers, enterprise data centers, and colocation facilities. Demand for high-speed interconnection across metro and regional networks remains strong across key industries such as healthcare, e-commerce, and finance. The US is also at the forefront of upgrading to 400G and 800G optical technologies and adopting open networking standards, further accelerating DCI deployment across the nation.

The leading players in the Global Data Center Interconnect Market include Arista Networks, Huawei, Cisco, Fujitsu, Nokia, Extreme Networks, and Juniper. Top companies in the data center interconnect market are focusing on innovation, scalability, and network intelligence to solidify their market position. Major vendors are investing in high-capacity optical transport systems that support 400G/800G technology to meet growing data demands. Strategic partnerships with hyperscale cloud providers are expanding solution reach and improving interoperability. Firms are integrating AI and telemetry tools to deliver real-time analytics, SLA compliance, and automated network adjustments. Modular hardware and software-defined solutions are being developed to ensure flexibility and quick deployment.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 Bandwidth

- 2.2.6 Deployment mode

- 2.2.7 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in AI and machine learning workloads

- 3.2.1.2 Rapid cloud adoption and edge computing expansion

- 3.2.1.3 Surge in global data traffic and storage demands

- 3.2.1.4 Increasing hyperscale data center deployments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital expenditure for DCI infrastructure.

- 3.2.2.2 Complex network management and integration issues.

- 3.2.3 Market opportunities

- 3.2.3.1 Development of AI-optimized DCI platforms

- 3.2.3.2 Growth in 5G and edge data center deployments

- 3.2.3.3 Expansion of digital infrastructure in emerging markets

- 3.2.3.4 Rising demand for energy-efficient and green DCI solutions

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Pricing trends and economic analysis

- 3.8.1 Historical pricing analysis and market evolution (2019-2024)

- 3.8.2 Current DCI pricing landscape (2024-2025)

- 3.8.3 Total cost of ownership (TCO) and economic analysis

- 3.8.4 Future pricing projections and market trends (2025-2034)

- 3.9 DCI network architecture and topology design

- 3.9.1 Network topology models and design principles

- 3.9.1.1 Point-to-point DCI architecture

- 3.9.1.2 Hub-and-spoke dci models

- 3.9.1.3 Mesh and any-to-any connectivity

- 3.9.1.4 Hybrid and multi-topology designs

- 3.9.2 Distance-based DCI solution architecture

- 3.9.2.1 Metro DCI (0-100km) solutions

- 3.9.2.2 Regional DCI (100-1000km) solutions

- 3.9.2.3 Long-haul DCI (1000km+) solutions

- 3.9.3 Application-specific dci architecture

- 3.9.3.1 Cloud provider DCI architecture

- 3.9.3.2 Enterprise DCI architecture

- 3.9.3.3 Financial services dci architecture

- 3.9.1 Network topology models and design principles

- 3.10 DCI capacity management and performance optimization

- 3.10.1 Network capacity planning and management

- 3.10.2 Performance monitoring and analytics

- 3.10.3 Quality of service and traffic management

- 3.11 Use cases

- 3.12 Energy efficiency and sustainability

- 3.12.1 Energy consumption analysis in DCI networks

- 3.12.2 Green networking and sustainability initiatives

- 3.12.3 Energy efficiency technologies and innovations

- 3.12.4 Sustainability ROI and business benefits

- 3.13 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Optical transceivers

- 5.2.2 Switches & routers

- 5.2.3 Cables & connectors

- 5.2.4 Optical amplifiers

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Software-Defined Networking (SDN)

- 5.3.2 Network management software

- 5.3.3 Analytics & optimization software

- 5.3.4 Others

- 5.4 Service

- 5.4.1 Professional

- 5.4.2 Managed

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Synchronous optical network (SONET)

- 6.3 Dense wavelength division multiplexing (DWDM)

- 6.4 Ethernet

- 6.5 Optical transport network (OTN)

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Cloud-based

- 7.3 On-premises

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Bandwidth, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Low bandwidth (Up to 1 Gbps)

- 8.3 Medium bandwidth (1-10 Gbps)

- 8.4 High bandwidth (10-100 Gbps)

- 8.5 Ultra-high bandwidth (Above 100 Gbps)

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Disaster recovery

- 9.3 Content delivery

- 9.4 Data replication

- 9.5 Load balancing

- 9.6 Cloud connectivity

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 Communications service providers (CSPs)

- 10.3 Internet content providers and carrier-neutral providers (ICPs/CNPs)

- 10.4 Government

- 10.5 Enterprises

- 10.5.1 BFSI

- 10.5.2 Healthcare

- 10.5.3 Media & Entertainment

- 10.5.4 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.3.7 Nordics

- 11.3.8 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Philippines

- 11.4.7 Indonesia

- 11.4.8 Singapore

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 ADVA Optical Networking

- 12.1.2 Arista Networks

- 12.1.3 Broadcom

- 12.1.4 Ciena

- 12.1.5 Cisco

- 12.1.6 Fujitsu

- 12.1.7 Huawei

- 12.1.8 IBM

- 12.1.9 Infinera

- 12.1.10 Juniper

- 12.1.11 Nokia

- 12.1.12 ZTE

- 12.2 Regional Players

- 12.2.1 Brocade Communication Systems

- 12.2.2 Colt Technology Services

- 12.2.3 CoreSite Realty

- 12.2.4 Digital Realty Trust

- 12.2.5 Evoque Data Center Solutions

- 12.2.6 Fiber Mountain

- 12.2.7 Flexential

- 12.2.8 Megaport

- 12.2.9 Zayo Group

- 12.3 Emerging Players

- 12.3.1 Cologix

- 12.3.2 Cyxtera Technologies

- 12.3.3 Dolphin Interconnect Solutions

- 12.3.4 Ekinops

- 12.3.5 Eoptolink

- 12.3.6 Innolight

- 12.3.7 Macom Technology Solutions

- 12.3.8 Pluribus Networks

- 12.3.9 XKL

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 320 Pages

- 納期

- 2~3営業日