欧州のデータセンターインターコネクト:市場シェア分析、産業動向、成長予測(2025年~2030年)

Europe Data Center Interconnect - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1630370

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

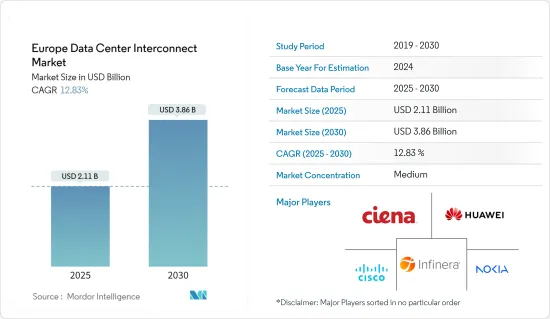

欧州のデータセンター相互接続市場規模は、2025年に21億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは12.83%で、2030年には38億6,000万米ドルに達すると予測されます。

データの急増とAIやハイパフォーマンス・コンピューティング(HPC)などの技術の拡大に伴い、データセンター資産を迅速、確実かつコスト効率よく接続する必要性が著しく高まっています。スループット、レイテンシー、運用の簡素化、メンテナンス、インテリジェンス、セキュリティといった要素は、データセンター・ベンダーにとって重要な優先事項となっています。データセンター間の帯域幅を拡大し、待ち時間を短縮し、パケットロスを排除するデータセンター間相互接続(DCI)技術の採用は、これが大きな要因の1つとなっています。

主要ハイライト

- 西欧と北欧では、ハイパースケールデータセンターの建設に多くの投資家を誘致するため、政府機関が減税などの優遇措置を提供しています。膨大な再生可能エネルギー資源、低い電力価格、良好な気候条件、優れたインフラ、熟練した労働力により、北欧諸国はデータセンター、ひいてはDCIに適しており、長年にわたって外国からの投資が急増しています。

- クラウドコンピューティング産業の成長と、全国的なサービス停止によるOTTサービス利用の最近の増加により、調査対象市場は拡大しています。さらに、5Gサービスの導入により、相互接続データセンターソリューションの範囲が広がる可能性があります。自律走行車、スマートシティ、デジタルツイン、バーチャルリアリティ、バーチャルアシスタント、ビデオモニタリング・モニタリング、ゲームなどが市場の需要を促進しています。

- クラウドコンピューティングは、データセンター相互接続市場を大きく牽引すると推定されるセグメントの1つです。クラウドコンピューティングは、企業が直面する運用コストの削減により、ここ数年で増加しています。コロケーションとクラウドを組み合わせることで、レイテンシーを削減し、セキュリティを高め、クラウド相互接続の機会を創出することができます。クラウドプロバイダー企業は、広帯域幅で回復力のある専用ネットワークと、堅牢なデータセンター・プロバイダーのサポートを必要としています。

- 特に中小企業にとって大きな課題は、データセンター接続サービスのコストです。データセンターの新設には、建設とメンテナンスの両面で多額の投資が必要となります。さらに、データセンター間の距離は、データセンターの効率を低下させ、データセンター相互接続産業の成長を制限する可能性があるため、重要です。

- 特に近年では、COVID-19の大流行によってインターネット・アプリケーションへのアクセスが必須となったため、オンライン活動の急速な成長によってデータセンター相互接続の需要が高まっています。仕事、ソーシャルネットワーキング、eコマース、バンキング、エンターテインメントをインターネットに依存する人が増えているため、ほぼ無制限のアップタイムと相互接続に対する需要が高まっている

欧州のデータセンター相互接続市場の動向

クラウド移行への継続的な動向が市場を牽引する見込み

- 国内外の企業やクラウドコンピューティング顧客からの需要の高まりが、企業のデータセンター設備拡大を後押ししています。欧州のデータセンター市場は、パブリッククラウドサービスが大半を占めています。政府機関では、予測期間中に行政でのクラウドサービスの利用拡大を計画しているため、プライベート・クラウドサービスの利用が拡大しています。しかし、ハイブリッド・クラウドサービスは、プライベート・クラウドサービスやパブリック・クラウドサービスよりも大きな成長の可能性を秘めています。クラウド技術の成長は、ひいては同地域におけるデータセンター相互接続技術の市場拡大につながっています。

- さらに、クラウドコンピューティングの採用拡大(COVID-19の大流行によりさらに拡大)、欧州全域における外資系クラウドベンダーの普及拡大、地域のデータセキュリティに関する政府の規則や規制、欧州の国内企業による投資の増加は、同地域における相互接続データセンターの需要を促進している主要要因のひとつです。

- さらに、Microsoftはノルウェーで複数のデータセンター拠点に投資し、GoogleLLCはフィンランドで事業を拡大しています。クラウド事業者だけでなく、企業や相互接続プロバイダーも北欧への投資を増やしています。このため、予測期間中に同地域のデータセンター相互接続市場の成長が促進されると予想されます。

- 2022年7月、米国の通信インフラプロバイダーであるZayoは、クラウドサービスプロバイダーがより高速なインターネット接続を求める中、英国と欧州大陸を結ぶZeus海底ルートを開設したと発表しました。現在、海底ケーブルは世界のインターネット・データトラフィックのほぼすべてを伝送しており、アルファベットのGoogleやメタを含む多くの技術企業も海底ケーブルの建設に投資しています。

- クラウドソリューションの普及や、AI、5G、エッジ・コンピューティングといった産業アプリケーションの普及に伴い、データセンターの需要は高まっています。その見返りとして、データセンター相互接続市場に絶大なビジネス機会がもたらされると予想されています。Cloudsceneによると、2024年2月現在、ドイツには522のデータセンターがあり、欧州諸国の中で最多となっています。データセンターは、コンピュータシステムを収容し、組織が共有する情報技術(IT)業務を集中管理する建物です。

ドイツが大きな市場シェアを占める

- データセンター数の増加、クラウド技術への投資の増加、エンドユーザー市場の拡大が、ドイツのデータセンターによる相互接続市場への投資を促進する主要要因となっています。GDPRや個人データ保護イニシアチブ(Gaia-X)のような厳格な地域法が、この地域のデータセンター建設と開発をさらに後押ししています。

- エッジコンピューティングソリューションの開発により、大容量ネットワークへの需要が増加しています。ドイツ経済は、自律走行車、クラウドコンピューティング、IoT、高度ロボット工学などの破壊的技術により、エッジ・コンピューティングソリューションの必要性を高めています。こうした技術の利用拡大により、より高い帯域幅と優れた処理速度が必要となっています。

- これらの障害を克服するには低遅延が不可欠であり、データセンターのコロケーション需要が高まっています。クラウドサービスプロバイダーは、ネットワーク設計をユーザーの近くにコロケーションすることで、高帯域幅と低遅延を提供できます。5Gの開発により、相互接続サービスプロバイダーは、ドイツの遠隔地間でより良い接続でこれらのサービスを提供できるようになり、市場の拡大に拍車をかけています。

- 5Gや、拡張現実(AR)、仮想現実(Virtual Reality)、AIなどの没入型技術の開発により、企業間のデータ共有用に確保される帯域幅の需要も高まっています。欧州の相互接続の帯域幅容量は急速に拡大しており、この傾向は今後も続くと予想されます。通信産業の市場シェアが最も大きいのは、顧客体験を向上させるための高速接続に対するニーズが高まっているためです。さらに、この地域の相互接続サービスプロバイダーは、スマートデバイスの急速な普及による接続性の向上とデータ転送遅延の減少に対する需要の拡大から利益を得ています。

- ここ数年、5GネットワークやAI、モノのインターネットなどの破壊的技術の開発により、データセンターのワークロードは増加しています。高負荷の管理とともに、企業内でのクラウドコンピューティングやAs-a-Serviceモデルの利用が増加し、専門的なスキルセットの需要が高まっています。Ericssonによると、中東欧におけるモバイル5Gの契約数は2028年までに2億2,940万件に達すると予想されています。中欧で最も発展している国の一つであるドイツでは、モバイル5Gの契約数が大きく伸びると予想されています。

欧州のデータセンター相互接続産業概要

欧州のデータセンター相互接続市場は、Huawei Technologies、Ciena Corporation、Cisco Systems Inc.、Infinera Corporation、Nokia Corporationなどの大手企業が存在し、半固体化しています。市場の参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年、ドイツは欧州第2位のコロケーション市場です。過去5年間、ドイツのデータセンター市場の成長を牽引してきたのは、企業が採用するデジタルトランスフォーメーション戦略、クラウドコンピューティング、モノのインターネット(IoT)、AIの採用、GDPRの施行です。ドイツでは約80%の組織が1つ以上のサービスにクラウドサービスを利用しており、その割合は増加しており、今後3~5年のCAGRは3~5%を記録すると予測されています。ドイツのデータセンターサービスプロバイダーであるaixitは、サービスデータの高い成長率とネットワーク運用コストの高さを考慮し、今後10年間でデータの流れを妨げず、データセンター間をシームレスに拡大するための接続性を構築することを決定したと発表しました。

- 2022年10月、Nokiaは欧州最大の分散型インターネット・エクスチェンジ・プロバイダーであるNL-ixとの提携拡大を発表しました。Nokiaは、画期的なルーティング・シリコンであるFP5を搭載した先進的な7750 SR-sプラットフォームを記載しています。この展開により、NL-ixは400GEと800GEのアクセスと相互接続サービスを、同社の国立研究教育ネットワーク(NREN)とクラウドプロバイダーの顧客に提供することができます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の産業への影響評価

第5章 市場力学

- クラウド移行への継続的動向

- 最近のネットワーク消費の変化と予想される5Gの導入が市場成長を牽引

- 市場課題

- 容量と設置に関する課題

第6章 市場セグメンテーション

- 国別

- ドイツ

- 英国

- フランス

- アイルランド

- スペイン

- その他の欧州

第7章 競合情勢

- 企業プロファイル

- Huawei Technologies

- Ciena Corporation

- Cisco Systems Inc.

- Infinera Corporation

- Nokia Corporation

- ZTE Corporation

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Europe Data Center Interconnect Market size is estimated at USD 2.11 billion in 2025, and is expected to reach USD 3.86 billion by 2030, at a CAGR of 12.83% during the forecast period (2025-2030).

With the proliferation of data and expansion of technologies like AI and high-performance computing (HPC), the need to connect data center assets quickly, reliably, and cost-effectively is growing significantly. Factors such as throughput, latency, simplified operations, maintenance, intelligence, and security are becoming significant priorities for data center vendors. This is one of the major factors driving the adoption of data center interconnect (DCI) technology, owing to its ability to boost inter-data center bandwidth, reduce latency, and eliminate packet loss.

Key Highlights

- Government agencies offer tax breaks and other benefits to attract the maximum number of investors to construct a hyperscale data center market in Western Europe & the Nordics. Due to vast resources of renewable energy, low power prices, favorable climate conditions, good infrastructure, and a skilled workforce, Nordic countries are well suited for data centers and, therefore, for DCI and have resulted in a surge of foreign investments over the years.

- The market studied is expanding due to the growing cloud computing industry and the recent increase in OTT service use due to a nationwide shutdown. Furthermore, introducing 5G services may broaden the scope of interconnected data center solutions. Autonomous cars, smart cities, digital twins, virtual reality, AI virtual assistants, video surveillance and monitoring, and gaming are fueling market demand.

- Cloud computing is one sector estimated to be a significant driver of the data center interconnect market. Cloud computing has been increasing over the past few years, owing to lower operational expenses faced by enterprises. Combining colocation with the cloud can reduce latency, increase security, and create cloud interconnection opportunities. Cloud provider companies require high bandwidth and resiliency private networks and support from a robust data center provider.

- The major challenge, especially for small and medium-sized businesses, is the cost of data center connectivity services. A new data center necessitates a significant investment in both construction and maintenance. Furthermore, the distance between data centers is important since it might reduce a data center's efficiency, limiting the growth of the data center interconnect industry.

- The fast growth of online activity has raised the demand for data center interconnection, particularly in recent years, as the COVID-19 pandemic made access to internet applications a requirement. With more people relying on the Internet for work, social networking, e-commerce, banking, and entertainment, the demand for almost limitless uptime and interconnection is growing.

Europe Data Center Interconnect Market Trends

Ongoing Trend Toward Cloud Migration is Expected to Drive the Market

- The growing demand from domestic and international enterprises and cloud computing customers has pushed companies to expand data center facilities. Public cloud services dominate the data center market in Europe. The use of private cloud services by government agencies is growing as they plan to make greater use of cloud services in public administration during the forecast period. However, hybrid cloud services have more substantial growth potential than private and public cloud services. The growth in cloud technology is, in turn, a growing market for data center interconnect technology in the region.

- Moreover, the growing adoption of cloud computing (which further escalated due to the COVID-19 pandemic), increasing penetration of foreign cloud vendors across Europe, governmental rules and regulations for local data security, and the increasing investments by domestic European players are some of the major factors that are driving the demand for interconnected data centers in the region.

- Furthermore, Microsoft Corporation has invested in multiple data center locations in Norway, while Google LLC has expanded its operations in Finland. It is not just the cloud enterprise players; enterprises and interconnection providers are also increasingly investing in the Nordics. This is expected to boost the growth of the data center interconnect market in the region over the forecast period.

- In July 2022, the US communications infrastructure provider Zayo announced that it had launched the Zeus subsea route that connects the United Kingdom and continental Europe as cloud service providers seek faster internet connections. Currently, undersea cables transmit nearly all the world's internet data traffic, and many technology companies, including Alphabet's Google and Meta, have also invested in building their subsea cables.

- The demand for data centers is growing with the popularity of cloud solutions and industry applications, such as AI, 5G, and edge computing. In return, it is anticipated to give immense opportunities to the data center interconnect market. According to Cloudscene, as of February 2024, there are 522 data centers located in Germany, the most in any European nation. Data centers are buildings that house computer systems and centralize organizations' shared information technology (IT) operations.

Germany to Hold a Significant Market Share

- The growing number of data centers, increasing investment in cloud technologies, and expanding end-user markets are major factors driving the German data centers' investment in the interconnect market. The stringent regional laws, like GDPR and Personal Data Protection Initiatives (Gaia-X), further boost the region's local data center construction and development.

- With the development of edge computing solutions, there has been an increase in the demand for high-capacity networks. The German economy has increased the need for edge computing solutions due to disruptive technologies like autonomous vehicles, cloud computing, IoT, and advanced robotics. Higher bandwidths and better processing speeds are now necessary due to the expanding use of these technologies.

- Low latency is crucial to overcoming these obstacles, raising the demand for colocation in data centers. Cloud service providers can offer high bandwidth and low latency by colocating their network design close to the users. The development of 5G has allowed interconnection service providers to deliver these services with better connections across remote German locations, fueling the market's expansion.

- The development of 5G and immersive technologies like augmented reality, virtual reality, and AI has also increased the demand for more bandwidth to be set aside for data sharing across businesses. The bandwidth capacity of Europe's interconnections is growing quickly, and this trend is expected to continue. The telecommunications industry has the most significant market share because of the rising need for high-speed connectivity to improve client experiences. In addition, the region's interconnection service providers benefit from expanding demand for enhanced connectivity and decreased data transfer latency due to the rapid uptake of smart devices.

- Over the past few years, data center workloads have increased due to the development of 5G networks and other disruptive technologies like AI and the Internet of Things. Along with managing high workloads, the rising use of cloud computing and As-a-Service models within businesses has boosted the demand for specialized skill sets. According to Ericsson, the number of mobile 5G subscriptions in Central and Eastern Europe is expected to reach 229.40 million by 2028. Germany, being one of the most developed countries in Central Europe, is expected to witness a significant growth in the number of mobile 5G subscriptions.

Europe Data Center Interconnect Industry Overview

The European data center interconnect market is semi-consolidated with the presence of major players like Huawei Technologies, Ciena Corporation, Cisco Systems Inc., Infinera Corporation, and Nokia Corporation. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- In 2023, Germany was Europe's second-largest colocation market. Over the past five years, the growth of the data center market in Germany has been driven by the digital transformation strategies adopted by enterprises, the introduction of cloud computing, the Internet of Things (IoT), AI, and the implementation of the GDPR. About 80% of the organizations in Germany use cloud services for one or more services, which has increased and is projected to register a CAGR of 3-5% over the next 3-5 years. Given the high growth rate of service data as well as the high cost of the network operation, German data center service provider aixit announced that it has decided to create connectivity for non-blocking the data flow and seamless expansion across the data centers in the next decade. aixit announced that it would build its own DCI network with Huawei's DC OptiX.

- In October 2022, Nokia announced an expanded partnership with NL-ix, Europe's largest distributed internet exchange provider. Nokia would supply its advanced 7750 SR-s platforms powered by its ground-breaking routing silicon, FP5. With this deployment, NL-ix can provide 400GE and 800GE access and interconnection services to its national research and education network (NREN) and cloud provider clients.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Ongoing Trend Toward Cloud Migration

- 5.1.1 Recent Changes in Network Consumption Coupled with Anticipated Adoption of 5G to Drive Market Growth

- 5.2 Market Challenges

- 5.2.1 Capacity and Installation Related Challenges

6 MARKET SEGMENTATION

- 6.1 By Country

- 6.1.1 Germany

- 6.1.2 United Kingdom

- 6.1.3 France

- 6.1.4 Ireland

- 6.1.5 Spain

- 6.1.6 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Huawei Technologies

- 7.1.2 Ciena Corporation

- 7.1.3 Cisco Systems Inc.

- 7.1.4 Infinera Corporation

- 7.1.5 Nokia Corporation

- 7.1.6 ZTE Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日