軟性内視鏡市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Flexible Endoscopes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801911

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

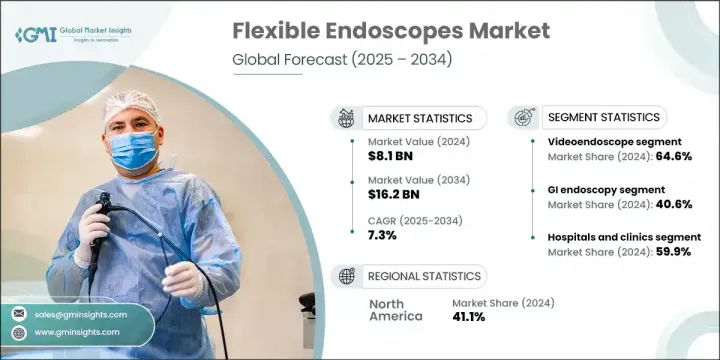

世界の軟性内視鏡市場は、2024年に81億米ドルと評価され、CAGR 7.3%で成長し、2034年には162億米ドルに達すると推定されています。

この成長軌道は、慢性疾患患者の増加、低侵襲処置へのシフトの増加、早期診断ケアへの意識の高まりによって後押しされています。より多くの患者が、より低リスク、より迅速な回復、より低コストの処置を求める中、軟性内視鏡検査はヘルスケアシステム全体で地歩を固め続けています。可視化技術、精密ツールの強化、患者の快適性の向上などの絶え間ない技術革新も、これらの機器の魅力を高めています。さらに、外来患者や外来治療の人気の高まりが新たな需要を生み出しており、軟性内視鏡は臨床分野にわたって拡張可能で費用対効果の高い診断・治療ソリューションを提供しています。

軟性内視鏡は、医師が大きな切開をすることなく、診断や外科処置の際に複雑な解剖学的構造をナビゲートできるよう、しなやかな挿入チューブを特徴としています。より侵襲の少ないヘルスケアをサポートするその役割は、急速に拡大しています。回復の早さ、外傷の軽減、全体的なコストの削減といった利点から、患者および医師の間でこれらの器具に対する嗜好が高まっています。これらの機器は、特に複雑な症例において正確かつ効率的な治療提供を可能にすることで、現代の治療ワークフローの基本となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 81億米ドル |

| 予測金額 | 162億米ドル |

| CAGR | 7.3% |

2024年、ビデオ内視鏡セグメントは世界市場の64.6%を占める。この優位性は、その優れた画像の鮮明さ、リアルタイムの視覚化、幅広い臨床専門分野への適応性に起因します。ビデオ内視鏡は、小型化されたカメラと高度な光学系を使用し、高解像度の映像を外部ディスプレイに映し出すことで、診断精度を大幅に高め、複雑な介入をサポートします。その使用範囲は、消化器科、呼吸器科、婦人科、泌尿器科に及ぶ。これらの機能により、低侵襲治療における精密医療に不可欠なツールとして、その地位は確固たるものとなっています。

消化器(GI)内視鏡検査セグメントは2024年に40.6%のシェアを占めました。消化管疾患の発生率の増加や定期的なスクリーニングに対する社会的関心の高まりが、このセグメントを押し上げる主な要因です。GI内視鏡検査は、入院期間を短縮し、患者の快適性を向上させることができるため、好ましい診断方法として成長を続けています。このセグメントの成長は、手技をより効率的で安全なものにする内視鏡技術の継続的な進歩も反映しており、世界中のヘルスケアプロバイダーで採用が進んでいます。

2024年の米国の軟性内視鏡市場規模は32億米ドルとなり、同地域は、強固なヘルスケアインフラ、先進医療機器の普及、医療ニーズの高まる高齢者人口の増加といったメリットを享受しています。米国は、早期診断と頻繁なスクリーニングに対する高い需要に支えられ、同地域における成長の主要な貢献者であり続けています。病院や外来センターへの最新内視鏡システムの普及は、成熟しつつも成長するこの市場の拡大を後押しし続けています。

軟性内視鏡世界市場の主要企業には、CooperSurgical、XION、PENTAX Medical、STORZ、RICHARD WOLF、町田製作所、ボストン・サイエンティフィック、富士フイルム、BD、ENDOMED SYSTEMS、Laborie、OLYMPUSなどがあります。軟性内視鏡市場で事業を展開する企業は、技術的に先進的でユーザーフレンドリーなシステムの製品ラインナップの拡充に注力しています。研究開発への戦略的投資は、操作性を向上させ、AI支援による視覚化を備えた超薄型高精細スコープの開発を目指しています。メーカー各社はまた、病院や専門クリニックとのパートナーシップを活用し、さまざまな医療現場での製品アクセスと展開を強化しています。さらに、規制当局の承認や新興国における現地製造拠点を通じて、地理的なリーチを拡大する取り組みも進められています。市場リーダーは、ブランド・ロイヤルティを強化するため、アフターセールス・サポート、メンテナンス・サービス、医師トレーニング・プログラムに投資しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の増加

- 技術的進歩

- 低侵襲治療の人気の高まり

- 健康意識の高まりと早期診断の需要

- 業界の潜在的リスク&課題

- 厳格な規制プロセス

- 市場機会

- AIとロボットシステムの統合

- ヘルスケア投資の増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- 技術的進歩

- 現在の技術動向

- 新興技術

- 価格分析、2024

- 償還シナリオ

- 使い捨てへの移行軟性内視鏡

- パイプライン分析

- 起動シナリオ

- ポーターの分析

- PESTEL分析

- 将来の市場動向

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ビデオ内視鏡

- ファイバースコープ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 消化管内視鏡検査

- 肺内視鏡検査

- 耳鼻咽喉科内視鏡検査

- 泌尿器科

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院と診療所

- 外来手術センター

- その他のエンドユーザー

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- BD

- Boston Scientific

- CooperSurgical

- ENDOMED SYSTEMS

- FUJIFILM

- Laborie

- Machida

- OLYMPUS

- PENTAX Medical

- RICHARD WOLF

- STORZ

- XION

目次

The Global Flexible Endoscopes Market was valued at USD 8.1 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 16.2 billion by 2034. This growth trajectory is fueled by the rising number of chronic disease cases, the increasing shift toward minimally invasive procedures, and heightened awareness of early-stage diagnostic care. As more patients seek procedures with lower risks, faster recovery, and lower costs, flexible endoscopy continues to gain ground across healthcare systems. Continuous innovation in visualization technologies, enhanced precision tools, and improved patient comfort is also elevating the appeal of these devices. Additionally, the rising popularity of outpatient and ambulatory care settings is creating new demand, with flexible endoscopes offering scalable, cost-effective diagnostic and therapeutic solutions across clinical disciplines.

The flexible endoscopes feature a pliable insertion tube that allows physicians to navigate complex anatomical structures during diagnostic and surgical procedures without large incisions. Their role in supporting less-invasive healthcare is expanding rapidly. The preference for these devices is rising among both patients and physicians due to advantages such as faster recovery, reduced trauma, and lower overall costs. These devices have become fundamental in modern treatment workflows by enabling precise and efficient care delivery, particularly in complex cases.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.1 Billion |

| Forecast Value | $16.2 Billion |

| CAGR | 7.3% |

In 2024, the videoendoscope segment accounted for 64.6% of the global market. This dominance is attributed to their superior image clarity, real-time visualization, and adaptability across a wide range of clinical specialties. Videoendoscopes use miniaturized cameras and advanced optics that deliver high-definition visuals to external displays, greatly enhancing diagnostic accuracy and supporting complex interventions. Their use spans across gastroenterology, pulmonology, gynecology, and urology. These features have cemented their place as essential tools for precision medicine in minimally invasive care settings.

The gastrointestinal (GI) endoscopy segment held a 40.6% share in 2024. Increasing rates of digestive tract disorders and growing public interest in routine screening are key factors boosting this segment. GI endoscopy continues to grow as a preferred diagnostic method due to its ability to reduce hospital stays and improve patient comfort. This segment's growth also reflects ongoing advancements in endoscopic technology that make procedures more efficient and safer, driving increased adoption across healthcare providers globally.

U.S. Flexible Endoscopes Market was valued at USD 3.2 billion in 2024. The region benefits from a robust healthcare infrastructure, widespread use of advanced medical equipment, and a growing senior population with increasing healthcare needs. The U.S. remains a primary contributor to growth within the region, supported by high demand for early diagnostics and frequent screenings. Strong penetration of modern endoscopy systems across hospitals and outpatient centers continues to fuel expansion in this mature yet growing market.

Key players in the Global Flexible Endoscopes Market include CooperSurgical, XION, PENTAX Medical, STORZ, RICHARD WOLF, Machida, Boston Scientific, FUJIFILM, BD, ENDOMED SYSTEMS, Laborie, and OLYMPUS. Companies operating in the flexible endoscopes market are focusing on expanding their product offerings with technologically advanced and user-friendly systems. The strategic investments in R&D aim to develop ultra-thin, high-definition scopes with enhanced maneuverability and AI-assisted visualization. Manufacturers are also leveraging partnerships with hospitals and specialty clinics to boost product access and deployment across varied care settings. Additionally, efforts are underway to expand their geographic reach through regulatory approvals and local manufacturing hubs in emerging economies. Market leaders are investing in after-sales support, maintenance services, and physician training programs to strengthen brand loyalty.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic conditions

- 3.2.1.2 Technological advancements

- 3.2.1.3 Increasing popularity of minimally invasive therapies

- 3.2.1.4 Rising health awareness and demand for early-stage diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory process

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and robotic systems

- 3.2.3.2 Rising healthcare investments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Reimbursement scenario

- 3.8 Transition toward single-use/disposable flexible endoscopes

- 3.9 Pipeline analysis

- 3.10 Start-up scenario

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Future market trends

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Videoendoscope

- 5.3 Fiberscope

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 GI endoscopy

- 6.3 Pulmonary endoscopy

- 6.4 ENT endoscopy

- 6.5 Urology

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BD

- 9.2 Boston Scientific

- 9.3 CooperSurgical

- 9.4 ENDOMED SYSTEMS

- 9.5 FUJIFILM

- 9.6 Laborie

- 9.7 Machida

- 9.8 OLYMPUS

- 9.9 PENTAX Medical

- 9.10 RICHARD WOLF

- 9.11 STORZ

- 9.12 XION

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日