|

市場調査レポート

商品コード

1801882

腹膜透析の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Peritoneal Dialysis Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 腹膜透析の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年08月11日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

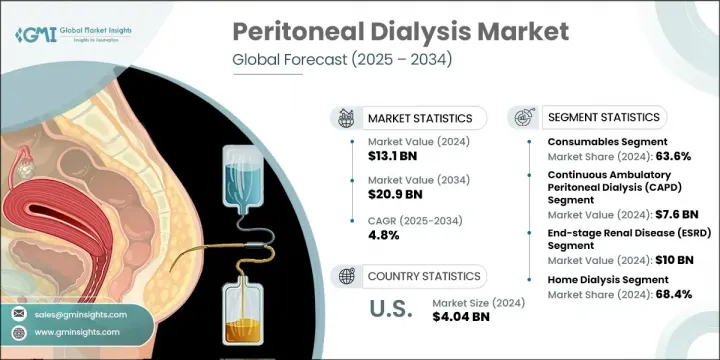

腹膜透析の世界市場規模は、2024年に131億米ドルとなり、CAGR4.8%で成長し、2034年までには209億米ドルに達すると予測されています。

この市場拡大に拍車をかけている主な要因としては、腎臓関連疾患の罹患率の上昇、在宅透析ソリューションの採用増加、透析治療を支える有利な償還制度などが挙げられます。さらに、従来の血液透析よりもコスト効率が高いこと、腎臓提供者の不足が続いていることも、市場の需要をさらに高めています。腹膜透析は、末期腎不全(ESRD)や急性腎障害に直面している人々の生命維持療法であり、腎臓が機能を失ったときに老廃物や余分な水分を効果的に除去することができます。在宅での患者管理ケアへのシフトの高まりが、業界の情勢を形成し続けています。さらに、人口の高齢化と慢性腎臓病患者の増加が、世界のPDソリューションの普及に大きく寄与しています。

2024年、消耗品セグメントのシェアは63.6%でした。この優位性は、ESRD患者の増加と、透析液、PDカテーテル、その他の関連消耗品など、PDに不可欠なコンポーネントの需要増によるところが大きいです。在宅治療へのシフトがこの傾向に大きく影響しており、患者が定期的な透析を単独で行うには、これらの製品の安定供給が必要だからです。患者の消耗品への依存の高まりは、慢性腎不全と急性腎不全の両方の有病率の上昇、特に高齢者人口の増加によって顕著になっています。このような人口動態の変化により、信頼性が高く、家庭で使用可能な透析液の需要が高まり続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 131億米ドル |

| 予測金額 | 209億米ドル |

| CAGR | 4.8% |

持続的外来透析(CAPD)分野は、2024年に76億米ドルの売上を記録し、2025年から2034年にかけてCAGR4.6%で成長すると予測されています。CAPDは、自動透析装置へのアクセスが制限されている地域では、依然として好ましい選択肢です。この方法は、患者が機械に頼らずに1日に何度も手動で透析を行うことを可能にし、手頃な価格、使いやすさ、通常の日常生活を維持できる柔軟性を提供します。人気が高まっているのは、透析センターへの依存を減らしながら、患者が自分の治療をよりコントロールできるようになることに起因しています。

米国の腹膜透析市場は2024年に40億4,000万米ドルを生み出し、2025年から2034年にかけてCAGR3.5%で成長すると予測されています。同国でPDが受け入れられつつあるのは、治療の柔軟性、在宅投与、生活の質の向上など、患者中心の利点があるためです。ヘルスケアプロバイダーは、特に医療制度がバリューベースのケアモデルを採用するにつれて、センターベースの血液透析に代わる有効な選択肢としてPDを推奨するようになってきています。この増加傾向は、在宅透析を選択する患者に対する意識の高まりとトレーニングプログラムの充実によってさらに加速しています。

世界の腹膜透析市場を積極的に形成しているトップクラスの企業は、Terumo、Vantive(Baxter)、Diaverum(M42)、BD、B. Braun、Davita Kidney Care、Polymed、Utah Medical Products、Vivance、Fresenius Medical Care、medCOMP、Mozarc Medicalです。市場ポジションを確保し競争力を強化するため、腹膜透析分野の企業はいくつかの戦略的イニシアチブを積極的に推進しています。

その中には、より高度でユーザーフレンドリーな在宅用透析ソリューションによる製品ポートフォリオの拡大や、サービス提供ネットワークを強化するためのヘルスケアプロバイダーとの提携などが含まれます。多くの企業は、効率性と安全性を向上させた次世代の透析装置を開発するため、研究開発に多額の投資を行っています。さらに、戦略的なM&Aは、地理的な範囲を広げ、専門的な能力を統合するために利用されています。また、特に発展途上地域において、患者の導入とアドヒアランスを高めるためのトレーニングプログラムや啓発キャンペーンも開始されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- 末期腎疾患(ESRD)患者数の増加

- ドナー腎臓の不足

- 血液透析に比べてコスト面で有利

- 透析治療に対する有利な償還シナリオ

- 糖尿病と高血圧の増加

- 業界の潜在的リスク・課題

- 治療における合併症

- 市場機会

- 在宅透析導入の増加

- 新興国における需要の増加

- 成長促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- テクノロジーの情勢

- 歴史的タイムラインと業界の進化

- 償還シナリオ

- 償還政策が市場成長に与える影響

- 地域別の価格分析、2024年

- 透析装置/サイクラー

- 腹膜透析溶液/透析液

- サービス

- ギャップ分析

- 消費者行動分析

- 疫学展望

- ポーターの分析

- PESTEL分析

- 将来の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域(RoW)

- 地域別

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:カテゴリー別、2021年~2034年

- 主要動向

- 透析装置/サイクラー

- 消耗品

- 腹膜透析溶液/透析液

- デキストロース

- イコデキストリン

- アミノ酸

- カテーテル

- アクセス製品

- その他の消耗品

- 腹膜透析溶液/透析液

- サービス

- 慢性透析

- 急性透析

- 消耗品

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 持続歩行腹膜透析(CAPD)

- 自動腹膜透析(APD)

第7章 市場推計・予測:病状別、2021年~2034年

- 主要動向

- 末期腎疾患(ESRD)

- 急性腎障害(AKI)

- その他の条件

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 在宅透析

- センター内透析

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- グローバルプレーヤー

- B. Braun

- BD

- Davita Kidney Care

- Diaverum(M42)

- Fresenius Medical Care

- medCOMP

- Mozarc Medical

- Polymed

- Terumo Corporation

- Utah Medical Products

- Vantive(Baxter)

- Vivance

- 地域のプレーヤー

- Apollo Dialysis

- Mitra Industries

- Newsol Technologies

- Northwest Kidney Centers

The Global Peritoneal Dialysis Market was valued at USD 13.1 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 20.9 billion by 2034. Key drivers fueling this expansion include the rising incidence of kidney-related conditions, increasing adoption of home-based dialysis solutions, and favorable reimbursement structures supporting dialysis treatment. Additionally, cost efficiency over traditional hemodialysis, combined with a persistent shortfall in kidney donors, further bolsters market demand. Peritoneal dialysis, a life-sustaining therapy for individuals facing end-stage renal disease (ESRD) and acute kidney injury, allows for the effective removal of waste and excess fluid when the kidneys lose function. A growing shift toward patient-managed care at home continues to shape the industry landscape. Moreover, the aging population and a growing number of patients affected by chronic kidney issues are contributing heavily to the uptake of PD solutions globally.

In 2024, the consumables segment held a 63.6% share. This dominance is largely attributed to a higher volume of ESRD cases and increasing demand for essential PD components such as dialysate solutions, PD catheters, and other related consumables. The shift toward home-based therapies has significantly influenced this trend, as patients require a steady supply of these products to conduct regular sessions independently. This growing patient reliance on consumables is magnified by the rising prevalence of both chronic and acute kidney failures, particularly within the elderly population. These demographic changes continue to push demand for dependable, home-compatible dialysis solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.1 Billion |

| Forecast Value | $20.9 Billion |

| CAGR | 4.8% |

The continuous ambulatory peritoneal dialysis (CAPD) segment generated USD 7.6 billion in 2024 and is forecasted to grow at a 4.6% CAGR during 2025-2034. CAPD remains a preferred choice in regions where access to automated dialysis equipment is limited. This approach enables patients to perform manual exchanges multiple times a day without relying on machines, offering affordability, ease of use, and the flexibility to maintain normal routines. Its growing popularity stems from its ability to empower patients with greater control over their treatment while reducing dependence on dialysis centers.

United States Peritoneal Dialysis Market was valued at USD 4.04 billion in 2024 and is expected to grow at a 3.5% CAGR from 2025 through 2034. The rising acceptance of PD in the country is due to its patient-centric benefits, including treatment flexibility, at-home administration, and improved quality of life. Healthcare providers are increasingly recommending PD as a viable alternative to center-based hemodialysis, especially as the healthcare system embraces value-based care models. This upward trend is further fueled by growing awareness and better training programs for patients opting for home dialysis.

The top-tier companies actively shaping the Global Peritoneal Dialysis Market are Terumo Corporation, Vantive (Baxter), Diaverum (M42), BD, B. Braun, Davita Kidney Care, Polymed, Utah Medical Products, Vivance, Fresenius Medical Care, medCOMP, and Mozarc Medical. To secure their market positions and enhance competitiveness, companies operating in the peritoneal dialysis sector are actively pursuing several strategic initiatives.

These include expanding their product portfolios with more advanced and user-friendly dialysis solutions tailored for home use, as well as forming partnerships with healthcare providers to strengthen service delivery networks. Many firms are investing heavily in R&D to develop next-generation PD devices with improved efficiency and safety profiles. Additionally, strategic mergers and acquisitions are being used to widen geographic reach and integrate specialized capabilities. Training programs and awareness campaigns are also being launched to boost patient adoption and adherence, particularly in developing regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Category trends

- 2.2.3 Type trends

- 2.2.4 Disease condition trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising number of end stage renal diseases (ESRD) patients

- 3.2.1.2 Shortage of donor kidneys

- 3.2.1.3 Cost advantages over hemodialysis

- 3.2.1.4 Favourable reimbursement scenario for dialysis treatment

- 3.2.1.5 Growing prevalence of diabetes and hypertension

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complications in the treatment

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in home dialysis adoption

- 3.2.3.2 Increasing demand in emerging countries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.6 Historical timeline and industry evolution

- 3.7 Reimbursement scenario

- 3.7.1 Impact of reimbursement policies on market growth

- 3.8 Pricing analysis by region, 2024

- 3.8.1 Dialysis machines/cyclers

- 3.8.2 Peritoneal dialysis solution/Dialysate

- 3.8.3 Services

- 3.9 Gap analysis

- 3.10 Consumer behaviour analysis

- 3.11 Epidemiology outlook

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Future market trends

- 3.15 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By Region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1.4 Rest of the world (RoW)

- 4.3.1 By Region

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Category, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dialysis machines/Cyclers

- 5.2.1 Consumables

- 5.2.1.1 Peritoneal dialysis solution/Dialysate

- 5.2.1.1.1 Dextrose

- 5.2.1.1.2 Icodextrin

- 5.2.1.1.3 Amino Acid

- 5.2.1.2 Catheters

- 5.2.1.3 Access products

- 5.2.1.4 Other consumables

- 5.2.1.1 Peritoneal dialysis solution/Dialysate

- 5.2.2 Services

- 5.2.2.1 Chronic dialysis

- 5.2.2.2 Acute dialysis

- 5.2.1 Consumables

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Continuous ambulatory peritoneal dialysis (CAPD)

- 6.3 Automated peritoneal dialysis (APD)

Chapter 7 Market Estimates and Forecast, By Disease Condition, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 End-stage renal disease (ESRD)

- 7.3 Acute kidney injury (AKI)

- 7.4 Other conditions

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Home dialysis

- 8.3 In-center dialysis

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 B. Braun

- 10.1.2 BD

- 10.1.3 Davita Kidney Care

- 10.1.4 Diaverum (M42)

- 10.1.5 Fresenius Medical Care

- 10.1.6 medCOMP

- 10.1.7 Mozarc Medical

- 10.1.8 Polymed

- 10.1.9 Terumo Corporation

- 10.1.10 Utah Medical Products

- 10.1.11 Vantive (Baxter)

- 10.1.12 Vivance

- 10.2 Regional players

- 10.2.1 Apollo Dialysis

- 10.2.2 Mitra Industries

- 10.2.3 Newsol Technologies

- 10.2.4 Northwest Kidney Centers