抵抗スポット溶接機の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Resistance Spot Welding Machines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801851

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

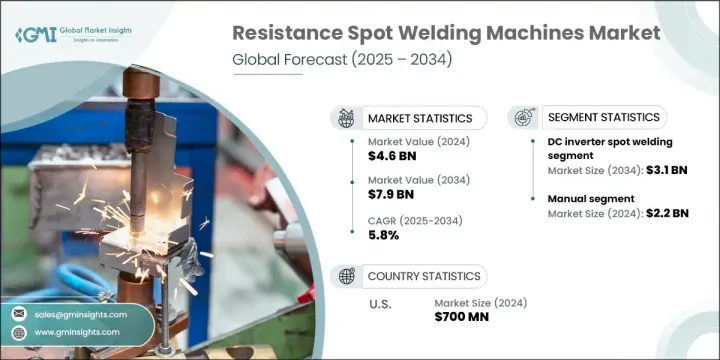

抵抗スポット溶接機の世界市場規模は、2024年に46億米ドルとなり、CAGR 5.8%で成長し、2034年には79億米ドルに達すると予測されています。

この成長は、特に自動車、航空宇宙、民生用電子機器製品生産などの高出力産業における製造自動化の継続的な進歩によって促進されています。メーカーは、品質、効率、スループットを最適化するために、デジタル制御とロボット溶接システムを統合しています。好意的な産業施策とアジア太平洋の製造業の拡大は、抵抗スポット溶接を大量生産環境における重要なプロセスとしてさらに位置づけています。

電気自動車の普及が進むにつれて、軽量、多金属構造とバッテリーコンポーネントの組み立てにおけるその関連性から、抵抗スポット溶接の需要が高まっています。抵抗スポット溶接は、その高速動作、信頼性、費用対効果により、構造接合用途に不可欠な溶接方法となっています。抵抗溶接はまた、高強度鋼やアルミニウムのような軽量材料へのエンジニアリングシフトをサポートし、熱歪みが少なく、溶接接合部の強度が高いという、最新の設計要件に不可欠な特性を記載しています。その結果、OEMとTier-1サプライヤーは、生産と材料の柔軟性の要求を満たすために、従来型RSW装置と先進的なRSW装置の両方への投資を世界的に続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 46億米ドル |

| 予測金額 | 79億米ドル |

| CAGR | 5.8% |

DCインバータセグメントは2024年に18億米ドルを生み出し、2034年には31億米ドルに達すると予測されています。これらの装置は、ACベース装置と比較して、精度の向上、電流応答の高速化、溶接サイクルの短縮を実現します。インバータ技術は一貫性を高め、運用コストを下げ、消費エネルギーを最大30%削減するため、持続可能性と効率性を追求するメーカーにとってますます魅力的なものとなっています。

手動スポット溶接セグメントは2024年に22億米ドルを占め、49.1%のシェアを確保しました。この需要の大部分は、ラテンアメリカ、アジア、東欧などの地域の中小企業によるものです。こうした事業では、手頃な価格、操作の容易さ、最小限のメンテナンスの必要性から、手動機に頼ることが多いです。手動スポット溶接機は、少量生産、多様な部品サイズ、頻繁なセットアップ変更が必要な産業で広く使用されています。HVAC製造、カスタム金属加工、家具製造などのセグメントでは、少量生産や特殊な作業における適応性と低運用コストから、引き続き手動システムが支持されています。

米国の抵抗スポット溶接機2024年の市場規模は7億米ドルで、2034年のCAGRは4.9%と予想されています。米国は、構造溶接が重要な自動車と防衛用途の世界の製造拠点であり続けています。電気自動車の生産が加速度的に伸びていることも国内需要を強化しており、大手自動車メーカーはバッテリーモジュールやBIW構造などの主要部品にスポット溶接機を導入しています。さらに、連邦政府による防衛への投資と生産能力の再調達が、現地OEMやサプライヤーによるRSWシステム需要の着実な増加を支えています。

抵抗スポット溶接機市場の主要企業には、ミヤチユニテック(AMADA WELD TECH)、CenterLine(Windsor)Ltd.、パナソニック溶接システムズ株式会社、Nimak GmbH、Automation International, Inc.などがあり、いずれもこのセグメントで主導的地位を維持しています。市場競争の主要企業は、自動化、エネルギー効率、高度制御システムへの投資を通じて競合を強化しています。自動車OEMや工業メーカーとの戦略的パートナーシップにより、進化する材料や設計のニーズに対応した溶接ソリューションの共同開発が可能になっています。いくつかのメーカーは、スマートモニタリング、予知保全、AI主導の溶接精度を備えた次世代インバータベースシステムを導入するため、研究開発活動を拡大しています。さらに、サービスネットワークの拡大と高成長地域における生産の現地化により、迅速なサポートと流通コストの削減が可能になります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 機会

- 成長可能性分析

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別・溶接材料別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:技術別、2021~2034年

- 主要動向

- 交流抵抗スポット溶接

- DCインバータスポット溶接

- コンデンサ放電スポット溶接

- サーボガンスポット溶接

第6章 市場推定・予測:溶接材料別、2021~2034年

- 主要動向

- 軟鋼

- ステンレス

- アルミニウム

- 亜鉛メッキ鋼

- 銅と合金

- その他(高強度低合金鋼(HSLA)、異種金属複合鋼、その他)

第7章 市場推定・予測:溶接厚さ別、2021~2034年

- 主要動向

- 最大2mm

- 2~5mm

- 5mm以上

第8章 市場推定・予測:電源別、2021~2034年

- 主要動向

- 単相電源

- 三相電源

- 直流電源

第9章 市場推定・予測:自動化レベル別、2021~2034年

- 主要動向

- 手動

- 半自動

- 自動

第10章 市場推定・予測:最終用途産業別、2021~2034年

- 主要動向

- 自動車

- 製造業

- 航空宇宙と防衛

- エレクトロニクスと半導体

- 建設

- 農業機器

- その他

第11章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- 直接

- 間接

第12章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第13章 企業プロファイル

- ARO Welding Technologies SAS

- Automation International, Inc.

- CenterLine(Windsor)Ltd.

- Dengensha Manufacturing Co., Ltd.

- Guangzhou CEA Welding Equipment Co., Ltd.

- Heron Intelligent Equipment Co., Ltd.

- Janda Company, Inc.

- Miyachi Unitek(AMADA WELD TECH)

- Nimak GmbH

- Panasonic Welding Systems Co., Ltd.

- T. J. Snow Company, Inc.

- TECNA S.p.A.

目次

The Global Resistance Spot Welding Machines Market was valued at USD 4.6 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 7.9 billion by 2034. This growth is being fueled by continued advancements in manufacturing automation, especially in high-output industries such as automotive, aerospace, and appliance production. Manufacturers are integrating digital controls and robotic welding systems to optimize quality, efficiency, and throughput. Favorable industrial policies and the expansion of manufacturing in the Asia-Pacific region have further positioned resistance spot welding as a key process in high-volume production environments.

As electric vehicle adoption rises, demand for resistance spot welding intensifies due to its relevance in assembling lightweight, multi-metal structures and battery components. The method's high-speed operation, reliability, and cost-effectiveness continue to make it indispensable in structural joining applications. Resistance welding also supports engineering shifts toward lightweight materials like high-strength steel and aluminum, offering low thermal distortion and strong weld joints-attributes crucial to modern design requirements. As a result, OEMs and Tier-1 suppliers globally continue to invest in both traditional and advanced RSW machines to meet production and material flexibility demands.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.6 Billion |

| Forecast Value | $7.9 Billion |

| CAGR | 5.8% |

The DC inverter segment generated USD 1.8 billion during 2024 and is projected to reach USD 3.1 billion by 2034. These machines provide enhanced precision, faster current response, and shorter weld cycles compared to AC-based equipment. Inverter technology improves consistency, lowers operational costs, and consumes up to 30% less energy, making it increasingly attractive for manufacturers pursuing sustainability and efficiency.

The manual spot-welding segment accounted for USD 2.2 billion in 2024, securing a 49.1% share. A significant portion of this demand stems from small and medium enterprises in regions such as Latin America, Asia, and Eastern Europe. These operations often rely on manual machines for their affordability, ease of operation, and minimal maintenance needs. Manual spot welders are widely used in small-batch production, varied part sizes, and industries require frequent setup changes. Sectors such as HVAC fabrication, custom metalwork, and furniture production continue to favor manual systems for their adaptability and low operating cost in low-volume or specialized tasks.

United States Resistance Spot Welding Machines Market generated USD 700 million in 2024 and is expected to grow at a CAGR of 4.9% through 2034. The US remains a global manufacturing hub for automotive and defense applications, where structural welding is critical. The accelerated growth of electric vehicle production has also strengthened domestic demand, with major automotive manufacturers deploying spot welding machines for key components like battery modules and BIW structures. Additionally, federal investments in defense and reshoring production capacity have supported a steady increase in demand for RSW systems from local OEMs and suppliers.

Major Resistance Spot Welding Machines Market players include Miyachi Unitek (AMADA WELD TECH), CenterLine (Windsor) Ltd., Panasonic Welding Systems Co., Ltd., Nimak GmbH, and Automation International, Inc., all of which continue to hold leading positions in this space. Leading companies in the resistance spot welding machines market are enhancing their competitive edge through investments in automation, energy efficiency, and advanced control systems. Strategic partnerships with automotive OEMs and industrial manufacturers allow for collaborative development of tailored welding solutions that meet evolving material and design needs. Several manufacturers are scaling up their R&D activities to introduce next-generation inverter-based systems with smart monitoring, predictive maintenance, and AI-driven welding precision. Additionally, expanding service networks and localization of production in high-growth regions enable faster support and lower distribution costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Material Welded

- 2.2.4 Welding Thickness

- 2.2.5 Power Supply

- 2.2.6 Automation Level

- 2.2.7 End Use Industry

- 2.2.8 Distribution Channel

- 2.3 CXO perspective: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region and materials welded

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Middle East and Africa

- 4.2.1.5 Latin America

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 AC Resistance Spot Welding

- 5.3 DC Inverter Spot Welding

- 5.4 Capacitor Discharge Spot Welding

- 5.5 Servo-Gun Spot Welding

Chapter 6 Market Estimates & Forecast, By Material Welded, 2021 - 2034, (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Mild Steel

- 6.3 Stainless Steel

- 6.4 Aluminum

- 6.5 Galvanized Steel

- 6.6 Copper & Alloys

- 6.7 Others (High Strength Low Alloy (HSLA) Steel, Dissimilar Metal Combination, etc.)

Chapter 7 Market Estimates & Forecast, By Welding Thickness, 2021 - 2034, (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Up to 2 mm

- 7.3 2 - 5 mm

- 7.4 Above 5 mm

Chapter 8 Market Estimates & Forecast, By Power Supply, 2021 - 2034, (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Single-phase Power Supply

- 8.3 Three-phase Power Supply

- 8.4 Direct Current Power Supply

Chapter 9 Market Estimates & Forecast, By Automation Level, 2021 - 2034, (USD Billion) (Units)

- 9.1 Key trends

- 9.2 Manual

- 9.3 Semi-automatic

- 9.4 Automatic

Chapter 10 Market Estimates & Forecast, By End Use Industry, 2021 - 2034, (USD Billion) (Units)

- 10.1 Key trends

- 10.2 Automotive

- 10.3 Manufacturing

- 10.4 Aerospace and Defense

- 10.5 Electronics and Semiconductors

- 10.6 Construction

- 10.7 Agricultural Equipment

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Units)

- 11.1 Key trends

- 11.2 Direct

- 11.3 Indirect

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 U.K.

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 UAE

- 12.6.2 Saudi Arabia

- 12.6.3 South Africa

Chapter 13 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 13.1 ARO Welding Technologies SAS

- 13.2 Automation International, Inc.

- 13.3 CenterLine (Windsor) Ltd.

- 13.4 Dengensha Manufacturing Co., Ltd.

- 13.5 Guangzhou CEA Welding Equipment Co., Ltd.

- 13.6 Heron Intelligent Equipment Co., Ltd.

- 13.7 Janda Company, Inc.

- 13.8 Miyachi Unitek (AMADA WELD TECH)

- 13.9 Nimak GmbH

- 13.10 Panasonic Welding Systems Co., Ltd.

- 13.11 T. J. Snow Company, Inc.

- 13.12 TECNA S.p.A.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日