|

市場調査レポート

商品コード

1910563

欧州の溶接機器市場:市場シェア分析、業界動向、統計、成長予測(2026年~2031年)Europe Welding Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の溶接機器市場:市場シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

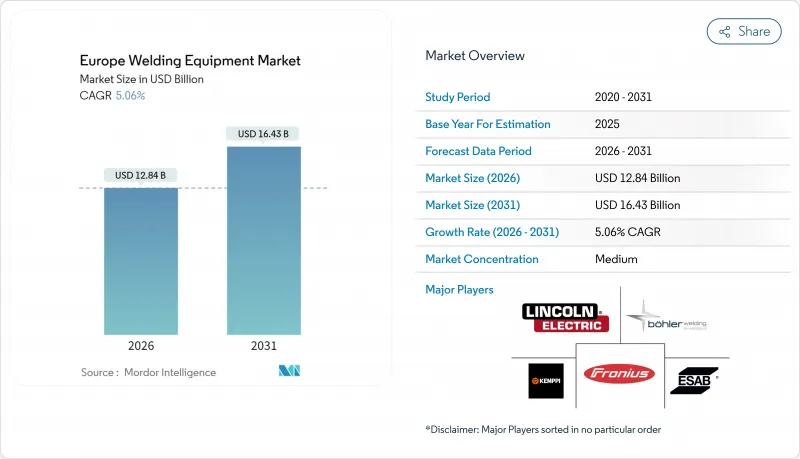

欧州の溶接機器市場の規模は、2026年に128億4,000万米ドルと推定され、2025年の122億2,000万米ドルから成長が見込まれます。

2031年の予測では164億3,000万米ドルに達し、2026年から2031年にかけてCAGR5.06%で拡大する見込みです。

市場拡大は、製造業者がセンサー・ソフトウェア・ロボット工学を統合したインダストリー4.0生産セルへ移行する中で加速する設備近代化を反映しています。需要の伸びが最も顕著なのは、電気自動車向けバッテリーパック組立と軽量アルミニウム接合分野であり、一方グリーンディールインフラ計画は公共部門における大型溶接システムの調達を支えています。サプライヤーは純粋な価格競争ではなく、ビーム品質の高いレーザー光源、電磁放射の少ないインバーター式電源装置、溶接データ分析プラットフォームといったプロセス革新で競合しています。認定溶接技師の継続的な不足が自動化投資を後押しし、中堅企業は労働力の変動リスクをヘッジするため協働ロボットセルを導入しています。

欧州の溶接機器市場の動向と洞察

欧州生産ラインにおける自動化・ロボティクスの浸透

欧州全域のメーカーは、30万人の溶接工不足を補い、ISO 3834品質要求を満たすため、ロボット溶接セルを導入しています。適応制御アルゴリズムが電流と移動速度をリアルタイムで調整し、複雑な接合形状におけるビードの一貫性を向上させます。ドイツの自動車部品サプライヤーは、人間オペレーターと作業領域を共有する協働ロボットを統合後、サイクルタイムを40%短縮したと報告しています。デジタルツインシミュレーションにより、導入前の溶接経路を最適化し、試運転サイクルを短縮するとともに、総合設備効率(OEE)を向上させています。モジュール式セルが3~5年のリース契約で手頃な価格かつ資金調達可能となったことで、採用は一次OEMから中堅サプライヤーへと波及しています。その結果もたらされる生産性の向上により、労働力不足はボトルネックから近代化の触媒へと転換しています。

EV関連溶接需要の急増

バッテリートレイや筐体の製造では、熱影響域を制限しつつアルミニウムと鋼材の接合が求められます。1,030nmで動作するファイバーレーザ光源は、毎分10mを超える速度で溶け込みを実現し、抵抗スポット溶接に取って代わり、6000系押出材の加工後処理を不要にします。この移行は、UN ECE R100安全規則が要求するバッテリーパックの厳格な公差をサポートします。欧州のシステムインテグレーターがEV生産増に対応するためラインを拡充する中、TRUMPFはマルチキロワットレーザーシステムのリードタイムを延長しました。プロセス監視モジュールは溶融池の寸法とエネルギー入力を記録し、自動車の型式認証審査に不可欠なトレーサビリティ記録を生成します。結果として、レーザー溶接への投資は生産性とコンプライアンスという二つの重要課題に合致します。

先進システムおよびレーザーシステムの高額設備投資

レーザー溶接セルの単価は20万~200万ユーロに上り、付帯設備(換気装置や防護装置)によりプロジェクト総費用は倍増する可能性があります。スループット向上のメリットがあるにもかかわらず、5年以上の回収期間が中小企業による導入を躊躇させています。リース会社が高出力レーザー資産に対し、不確実な残存価値を理由に高いリスクプレミアムを適用するため、資金調達ギャップは拡大傾向にあります。光学部品、冷却装置、ソフトウェア更新のための年間5万ユーロの保守契約が総所有コストを押し上げます。その結果、精度要求がレーザーソリューションを推奨する場合でも、多くの小規模製造業者は半自動MAG装置の使用を継続しています。

セグメント分析

2025年時点でアーク溶接は欧州の溶接機器市場シェアの56.12%を占め、2031年までCAGR4.94%で拡大が見込まれます。アーク溶接の規模は、携帯性と厚肉加工能力が依然として不可欠な土木建設、造船、プラント保守分野に支えられています。レーザーおよびプラズマシステムは、アルミニウムボディ部品や薄板電子機器筐体向けに狭い熱影響域と高速ライン速度を求めるユーザーにより、最も速い収益拡大を記録しています。はんだ付け、ろう付け、鍛造溶接といった「その他」プロセスに関連する欧州の溶接機器市場規模は、電子機器の小型化と歴史的建造物修復を背景に7.92%のCAGRを示しています。消耗品ベンダーは異種金属接合用のアルミニウム・ニッケル系溶加材で対応し、監視スタートアップ企業はビード形状を記録する光学センサーを組み込み、リアルタイム品質アラートを実現しています。溶接ヒューム規制の強化により、ガス溶接から堆積効率の高いインバーター式MIG装置への移行がさらに促進されています。積層造形技術の普及に伴い、ワイヤアーク堆積ヘッドが既存ロボットにボルト固定可能となり、セル全体を交換せずに増分収益の創出を可能にしています。

第二世代アーク電源は、MIG・TIG・スティック溶接モードをシームレスに切り替え可能なマルチプロセスファームウェアを搭載し、請負工場の設備柔軟性を向上させます。抵抗スポット溶接は自動車量産ラインでのシェアを維持しますが、アルミニウム製バッテリー筐体では遠隔シームレーザーが一部工程を代替し始めています。プラズマ溶接のニッチ市場は、ニッケル超合金への深い溶け込みと最小限の歪みを要求する航空宇宙エンジンプログラム内で拡大しています。したがって、プロセスの多様化は、重鋼構造物から精密医療機器まで多岐にわたる欧州の多速度製造基盤を反映しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 欧州の生産ラインにおける自動化・ロボット技術の普及

- 電気自動車関連溶接需要の急増(バッテリートレイ及び軽量アルミニウム)

- EUグリーンディールに基づくインフラ更新支出

- EU電磁界曝露指令2013/35/EUに基づくコンプライアンス改修

- ハンドヘルドファイバーレーザー溶接機が中小企業での採用を拡大

- ESG監査に対応したトレーサビリティプラットフォーム(溶接データ分析)

- 市場抑制要因

- 高度なレーザーシステムの高額な設備投資

- 認定溶接工および指導員の不足

- 鉄鋼・アルミニウム価格の変動性

- 電磁界(EMF)及び煙粉塵曝露限界値に関するコンプライアンスコストの上昇

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- 業界の魅力度- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- プロセス別

- アーク溶接

- 抵抗溶接

- レーザー溶接

- プラズマ溶接

- ガス溶接

- その他- はんだ付け・ろう付け、鍛接など

- エンドユーザー別

- 建設・インフラ

- 石油・ガス・石油化学

- エネルギー・発電

- 自動車・輸送機器

- 重工業・産業機器

- 航空宇宙・防衛

- その他(専門用途- 小規模製造ワークショップ、保守・修理、カスタム溶接サービス)

- 自動化レベル別

- 手動

- 半自動

- 自動/ロボット制御

- 地域別

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベネルクス(ベルギー、オランダ、ルクセンブルク)

- 北欧諸国(デンマーク、フィンランド、アイスランド、ノルウェー、スウェーデン)

- その他の欧州

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Lincoln Electric Holdings Inc.

- ESAB Corp.

- Fronius International GmbH

- Kemppi Oy

- voestalpine Bohler Welding

- Carl Cloos SchweiBtechnik GmbH

- AMADA WELD TECH

- EWM AG

- Hobart Welders

- Denyo Co. Ltd

- W.W. Grainger Inc.

- Obara Corporation

- Polysoude SAS

- CEBORA S.p.A

- TRUMPF Group

- Air Liquide SA

- Panasonic Industry Europe GmbH

- Daihen Corp.

- IPG Photonics(EU operations)

- Plansee SE