オート麦フレークの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Oat Flakes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801840

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

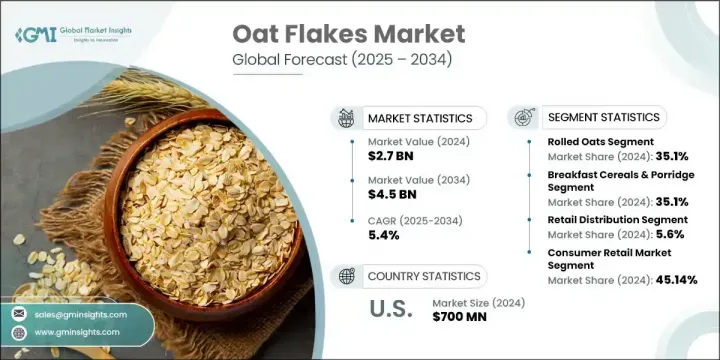

オート麦フレークの世界市場は、2024年には27億米ドルと評価され、CAGR5.4%で成長し、2034年までには45億米ドルに達すると推定されています。

オート麦フレークは、オート麦の全粒粉を蒸し、丸め、平らにして製造されます。これらのフレークは朝食の主食として人気があり、様々な包装食品や焼成食品の機能性原料となっています。消費者の間で健康とウェルネスへの関心が高まっていることが、この市場の成長を促す大きな要因となっています。食物繊維、必須ミネラル、ビタミンを豊富に含むことで知られるオート麦フレークは、健康志向の高い人々が、健康的で便利な食事やスナックの代替品を求めていることをアピールしています。

製品革新は業界の形成に重要な役割を果たしています。多くのトップブランドは、インスタントオーツ、フレーバーオプション、多忙なライフスタイルや多様な食事ニーズに対応した栄養強化処方など、製品の多様化を進めています。ホットブレックファスト、スムージーボウル、お菓子作りのレシピなど、その使い勝手の良さは、世界の家庭で愛用される製品としてオート麦フレークを定着させるのに役立っています。北米が世界市場で圧倒的なシェアを占めているのは、消費者の強い認知度、確立された朝食文化、高品質なオート麦ベースの製品への幅広いアクセスに支えられているからです。同地域の高度な小売ネットワークと堅調な国内オート麦生産も安定した需要に貢献しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 27億米ドル |

| 予測金額 | 45億米ドル |

| CAGR | 5.4% |

ロールドオーツ分野は2024年に35.1%のシェアを占め、2034年までにCAGR5.5%で成長すると予測されます。ロールドオーツが広く支持されている理由は、適度な調理時間と強い栄養価のバランスにあります。消費者は、親しみやすい食感と、朝食用ボウルから焼き菓子まで幅広いレシピに対応できる汎用性から、これらのオーツ麦に引き寄せられます。加工レベルが比較的低いため、主要な栄養素が保持され、健康志向のバイヤーの間でその地位が強化されています。

用途別では、朝食用シリアルとお粥の分野が2024年に35.1%のシェアを占め、2034年までのCAGRは5.5%と予想されます。朝に高繊維質で心臓に良い食事を好む傾向が強まっているため、このカテゴリーのオーツ麦の消費量が増加しています。コレステロールを管理し、エネルギーを長時間持続させるという役割が認められているため、栄養価の高い一日の始まりを優先する消費者にとって、オーツ麦は最良の選択肢となっています。さらに、製パン・加工食品業界でも需要が伸びており、マフィン、クッキー、パンなどの食感や栄養価を向上させるためにオート麦フレークが使用されることが増えています。

米国のオート麦フレーク市場は2024年に7億米ドルを生み出しました。米国における市場の成長軌道を支えているのは、健康意識の高まり、植物性食品やグルテンフリー食品への関心の高まり、旺盛な国内供給です。オーツ麦の栽培地域の改善と効率的な製造オペレーションも主要な貢献要因です。米国の消費者は、消化の改善や心臓の健康など、機能的な健康効果を提供する製品に対する一貫した需要を示しており、これはオート麦フレークの栄養プロファイルとよく合致しています。

世界のオート麦フレーク市場を形成している企業には、Richardson International Limited、Great River Organic Milling、McCann's Irish Oatmeal、Blue Lake Milling、Kellogg Company、Grain Millers Inc、Nature's Path Foods、Jordans Dorset Ryvita、Flahavan's、PepsiCo(Quaker Oats)、Mornflake、Morning Foods Limited、Arrowhead Mills(Hain Celestial Group)、Hodgson Mill、Honeyville Food Products、Avena Foods Limited、Cream Hill Estates、General Mills、Country Choice Organic、Gluten Free Oats LLC、Bob's Red Mill Natural Foods、Hamlyns of Scotlandなどがあります。オート麦フレーク分野で事業を展開する企業は、イノベーション、持続可能性、市場セグメンテーションを優先し、プレゼンスを拡大しています。主な戦略のひとつは、進化する消費者選好に対応するため、オーガニックやグルテンフリーのものから、フレーバー付きや調理済みのものまで、多様な製品ラインを発売することです。多くの企業は、味と食感を改善しながら栄養成分を保持する高度な加工技術に投資しています。ブランディングとパッケージングも重要な役割を担っており、クリーンラベルや健康訴求を強調する取り組みが行われています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 成長促進要因

- 業界の潜在的リスク・題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 価格動向

- 地域別

- 製品タイプ別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ロールドオーツ(昔ながらのオーツ麦)

- 通常のロールドオーツ

- オーガニックロールドオーツ

- 風味豊かなロールドオーツ

- クイックオーツ(クイッククッキングオーツ)

- 標準的なクイックオーツ

- オーガニッククイックオーツ

- 強化クイックオーツ

- インスタントオーツ麦

- プレーンインスタントオーツ

- フレーバー付きインスタントオーツ

- プレミアムインスタントオーツ

- スティールカットオーツ麦(アイリッシュオーツ麦)

- 伝統的なスチールカット

- クイッククッキングスチールカット

- オーガニックスティールカットオーツ

- 特性プレミアムオート麦フレーク

- 古代穀物ブレンド

- グルテンフリー認証オート麦

- 伝統品種と伝統文化

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 朝食用シリアルとお粥

- 温かい朝食用シリアル

- 冷たい朝食のアプリケーション

- オーバーナイトオートミールと調理済みオートミール

- ベーキング・食品製造

- 家庭でのベーキング用途

- 商業食品製造

- 食品加工産業

- 飲料・スムージー

- スムージー・シェイク用途

- 植物由来のミルク代替品

- 機能性飲料

- スナック食品とバー

- グラノーラとエネルギーバー

- スナックミックスとトレイルミックス

- クラッカーとチップス

- ベビーフードと乳児の栄養

- 幼児用シリアル製品

- 幼児と子供の栄養

第7章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 小売流通

- スーパーマーケットとハイパーマーケット

- 健康食品・専門店

- コンビニエンスストア

- オンラインとeコマース

- 主要なeコマースプラットフォーム

- 消費者直販チャネル

- モバイルコマース

- 食品サービス流通

- レストランとカフェの売上

- 施設内飲食サービス

- ホスピタリティと観光

- 卸売・B2B流通

- 食品卸売業者

- 工業・商業販売

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 消費者小売市場

- 家計消費

- 健康志向の消費者

- 家族と子供向けのマーケット

- 高齢者

- 食品製造業

- 朝食用シリアルメーカー

- 焼き菓子製造業者

- スナック食品会社

- ベビーフードメーカー

- 外食産業

- レストランやカフェの運営者

- 施設内飲食サービス

- ケータリングとイベントサービス

- ヘルスケアフードサービス

- 産業用途

- 原料供給業界

- 栄養補助食品製造

- 動物飼料産業

- 輸出と国際貿易

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- PepsiCo Inc.(Quaker Oats)

- Kellogg Company

- General Mills Inc.

- Bob's Red Mill Natural Foods

- Nature's Path Foods

- Arrowhead Mills(Hain Celestial Group)

- Country Choice Organic

- Grain Millers Inc.

- Richardson International Limited

- Avena Foods Limited

- Blue Lake Milling

- Gluten Free Oats LLC

- Morning Foods Limited

- Mornflake

- Hamlyns of Scotland

- Jordans Dorset Ryvita

- Flahavan's

- Honeyville Food Products

- Great River Organic Milling

- Hodgson Mill

- McCann's Irish Oatmeal

- Cream Hill Estates

目次

The Global Oat Flakes Market was valued at USD 2.7 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 4.5 billion by 2034. Oat flakes are produced by steaming, rolling, and flattening whole oat groats. These flakes have become a popular breakfast staple and functional ingredient in various packaged and baked food products. The rising emphasis on health and wellness among consumers is a significant factor fueling the growth of this market. Known for being rich in fiber, essential minerals, and vitamins, oat flakes appeal to health-conscious individuals seeking wholesome and convenient meal or snack alternatives.

Product innovation is playing a key role in shaping industry. Many top brands are diversifying their offerings to include instant oats, flavored options, and nutrient-enriched formulations designed for busy lifestyles and varied dietary needs. Their ease of use-whether in a hot breakfast, smoothie bowl, or a baking recipe-has helped establish oat flakes as a go-to product across global households. North America holds the dominant share in the global market, supported by strong consumer awareness, a well-established breakfast culture, and widespread access to high-quality oat-based products. The region's advanced retail networks and robust domestic oat production also contribute to consistent demand.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 5.4% |

The rolled oats segment held 35.1% share in 2024 and is forecasted to grow at a CAGR of 5.5% by 2034. Their widespread appeal stems from a balance between moderate cook times and strong nutritional value. Consumers gravitate toward these oats for their familiar texture and versatility across recipes ranging from breakfast bowls to baked goods. Their relatively lower processing level ensures they retain key nutrients, which strengthens their position among health-minded buyers.

In terms of application, the breakfast cereals and porridge segment held 35.1% share in 2024, and is expected to grow at a CAGR of 5.5% through 2034. The growing preference for high-fiber, heart-healthy meals in the morning has increased the consumption of oats in this category. Their recognized role in managing cholesterol and providing long-lasting energy makes them a top choice for consumers prioritizing nutritious starts to the day. Additionally, demand is growing within the baking and packaged food industry, where oat flakes are increasingly used to improve texture and nutritional content in items such as muffins, cookies, and breads.

United States Oat Flakes Market generated USD 700 million in 2024. The market's growth trajectory in the US is supported by a mix of rising health awareness, growing interest in plant-based and gluten-free diets, and strong domestic supply. Improvements in local oat cultivation and efficient manufacturing operations are also key contributors. Consumers in the US are showing consistent demand for products that offer functional health benefits like improved digestion and heart health, which aligns well with oat flakes' nutritional profile.

Companies shaping the Global Oat Flakes Market include Richardson International Limited, Great River Organic Milling, McCann's Irish Oatmeal, Blue Lake Milling, Kellogg Company, Grain Millers Inc., Nature's Path Foods, Jordans Dorset Ryvita, Flahavan's, PepsiCo Inc. (Quaker Oats), Mornflake, Morning Foods Limited, Arrowhead Mills (Hain Celestial Group), Hodgson Mill, Honeyville Food Products, Avena Foods Limited, Cream Hill Estates, General Mills Inc., Country Choice Organic, Gluten Free Oats LLC, Bob's Red Mill Natural Foods, and Hamlyns of Scotland. Companies operating in the oat flakes sector are prioritizing innovation, sustainability, and market segmentation to expand their presence. One of the primary strategies is the launch of diverse product lines-ranging from organic and gluten-free variants to flavored and ready-to-cook oat flakes-to cater to evolving consumer preferences. Many players are investing in advanced processing techniques that retain nutritional content while improving taste and texture. Branding and packaging also play a critical role, with efforts aimed at highlighting clean labels and health claims.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Application

- 2.2.3 Distribution channel

- 2.2.4 End use industry

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million & Tons)

- 5.1 Key trends

- 5.2 Rolled oats (old-fashioned oats)

- 5.2.1 Regular rolled oats

- 5.2.2 Organic rolled oats

- 5.2.3 Flavored rolled oats

- 5.3 Quick oats (quick-cooking oats)

- 5.3.1 Standard quick oats

- 5.3.2 Organic quick oats

- 5.3.3 Fortified quick oats

- 5.4 Instant oats

- 5.4.1 Plain instant oats

- 5.4.2 Flavored instant oats

- 5.4.3 Premium instant oats

- 5.5 Steel-cut oats (irish oats)

- 5.5.1 Traditional steel-cut

- 5.5.2 Quick-cooking steel-cut

- 5.5.3 Organic steel-cut oats

- 5.6 Specialty and premium oat flakes

- 5.6.1 Ancient grain blends

- 5.6.2 Gluten-free certified oats

- 5.6.3 Heritage and heirloom varieties

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Tons)

- 6.1 Key trends

- 6.2 Breakfast cereals & porridge

- 6.2.1 Hot breakfast cereals

- 6.2.2 Cold breakfast applications

- 6.2.3 Overnight and prepared oats

- 6.3 Baking and food manufacturing

- 6.3.1 Home baking applications

- 6.3.2 Commercial food manufacturing

- 6.3.3 Industrial food processing

- 6.4 Beverages and smoothies

- 6.4.1 Smoothie and shake applications

- 6.4.2 Plant-based milk alternatives

- 6.4.3 Functional beverages

- 6.5 Snack foods and bars

- 6.5.1 Granola and energy bars

- 6.5.2 Snack mixes and trail mixes

- 6.5.3 Crackers and chips

- 6.6 Baby food and infant nutrition

- 6.6.1 Infant cereal products

- 6.6.2 Toddler and child nutrition

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Million & Tons)

- 7.1 Key trends

- 7.2 Retail distribution

- 7.2.1 Supermarkets and hypermarkets

- 7.2.2 Health food and specialty stores

- 7.2.3 Convenience stores

- 7.3 Online and e-commerce

- 7.3.1 Major e-commerce platforms

- 7.3.2 Direct-to-consumer channels

- 7.3.3 Mobile commerce

- 7.4 Food service distribution

- 7.4.1 Restaurant and cafe sales

- 7.4.2 Institutional food service

- 7.4.3 Hospitality and tourism

- 7.5 Wholesale and b2b distribution

- 7.5.1 Food distributors

- 7.5.2 Industrial and commercial sales

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million & Tons)

- 8.1 Key trends

- 8.2 Consumer retail market

- 8.2.1 Household consumption

- 8.2.2 Health-conscious consumers

- 8.2.3 Family and children's market

- 8.2.4 Senior and elderly consumers

- 8.3 Food manufacturing industry

- 8.3.1 Breakfast cereal manufacturers

- 8.3.2 Baked goods producers

- 8.3.3 Snack food companies

- 8.3.4 Baby food manufacturers

- 8.4 Food service industry

- 8.4.1 Restaurant and cafe operators

- 8.4.2 Institutional food service

- 8.4.3 Catering and event services

- 8.4.4 Healthcare food service

- 8.5 Industrial applications

- 8.5.1 Ingredient supply industry

- 8.5.2 Nutritional supplement manufacturing

- 8.5.3 Animal feed industry

- 8.5.4 Export and international trade

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 PepsiCo Inc. (Quaker Oats)

- 10.2 Kellogg Company

- 10.3 General Mills Inc.

- 10.4 Bob's Red Mill Natural Foods

- 10.5 Nature's Path Foods

- 10.6 Arrowhead Mills (Hain Celestial Group)

- 10.7 Country Choice Organic

- 10.8 Grain Millers Inc.

- 10.9 Richardson International Limited

- 10.10 Avena Foods Limited

- 10.11 Blue Lake Milling

- 10.12 Gluten Free Oats LLC

- 10.13 Morning Foods Limited

- 10.14 Mornflake

- 10.15 Hamlyns of Scotland

- 10.16 Jordans Dorset Ryvita

- 10.17 Flahavan's

- 10.18 Honeyville Food Products

- 10.19 Great River Organic Milling

- 10.20 Hodgson Mill

- 10.21 McCann's Irish Oatmeal

- 10.22 Cream Hill Estates

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日