吸収性外科手術用縫合糸市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Absorbable Surgical Sutures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801828

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

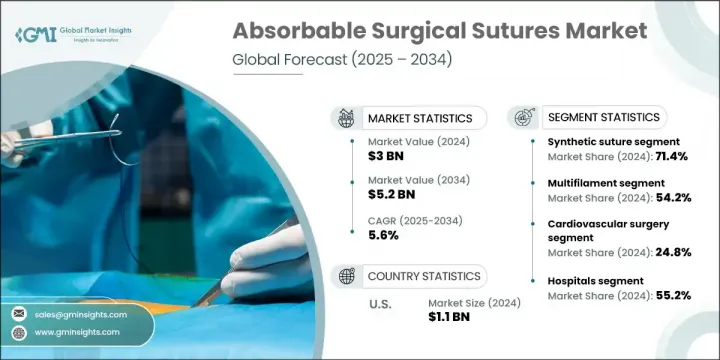

世界の吸収性外科手術用縫合糸市場は2024年に30億米ドルと評価され、CAGR 5.6%で成長し、2034年には52億米ドルに達すると推定されます。

市場成長の原動力となっているのは、世界の外科手術件数の急増、慢性疾患の増加、縫合技術の進歩、婦人科手術の急増などです。吸収性縫合糸の需要も、ヘルスケアシステムが低侵襲技術、回復期間の短縮、患者の転帰の改善を重視するにつれて増加しています。コーティングや糸構造の革新など、素材や技術の絶え間ない改良が、世界中の病院、手術センター、外来施設での使用拡大に大きな役割を果たしています。

吸収性外科手術用縫合糸は、体内で自然に分解されるように設計されており、手作業による除去の必要性をなくし、術後のケアを簡素化します。抗菌特性、有刺糸構造、高性能ポリマーブレンドなどの強化された機能は、感染リスクの軽減と治癒の促進に役立っています。このような先進的なツールを採用する臨床現場が増えるにつれて、全体的な効率と患者の体感が向上し、現代ヘルスケアにおける製品の関連性が強化されています。患者の快適性と手技の最適化への注目が高まるにつれ、吸収性縫合糸は複数の外科専門分野で好まれる選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 30億米ドル |

| 予測金額 | 52億米ドル |

| CAGR | 5.6% |

合成縫合糸セグメントは2024年に71.4%のシェアを占め、信頼性の高い吸収プロファイル、高い強度保持力、生物学的反応性の低減に支えられています。ポリジオキサノン(PDO)、ポリ乳酸(PLA)、ポリグリコール酸(PGA)のような素材は、外科医が劣化のタイミングを正確にコントロールできるため、創傷治癒の各段階に合わせたサポートが可能になります。開腹手術と低侵襲手術の両方に適応できるため、高精度の環境で信頼されるソリューションとなっています。

2024年の病院セグメントのシェアは55.2%でした。この優位性は、慢性疾患負担の増加や手術技術へのアクセス強化とともに、特に高成長国における病院インフラの拡大に関連しています。ヘルスケアシステムの進化に伴い、新設および既存の病院は、転帰を改善し、合併症発生率を低減し、最新の外科手術基準を満たすために、高度な縫合オプションを優先しています。

米国の吸収性外科手術用縫合糸の市場規模は2024年に11億米ドルとなりました。慢性疾患の増加と高度な外科治療の必要性が引き続き需要を高めています。心臓血管外科、腫瘍外科、一般外科の年間手術件数は増加しており、回復を早め、感染リスクを低減し、自然吸収により患者の不快感を最小限に抑える縫合糸へのシフトが進んでいます。

吸収性外科手術用縫合糸世界市場を独占している主要企業には、Demetech、Corza Medical、Futura Surgicare、B. Braun、Medtronic、Unisur、Vitrex Medical Group、Healthium Medtech、Genesis MedTech、Vital Sutures、Advanced Medical Solutions、Lotus Surgicals、Integra Lifesciences、Johnson &Johnson、CONMEDなどがあります。吸収性外科手術用縫合糸市場に参入している企業は、生体材料設計と抗菌技術の革新を通じて、その地位を強化しています。各社は、引張強度を高め、分解速度を制御し、低侵襲技術に適合する縫合糸を開発するための研究開発に注力しています。合併、買収、戦略的提携は、製品ポートフォリオを拡大し、世界に展開するために進められています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の有病率の増加

- 世界中で増加している外科手術

- 縫合材料の進歩

- 婦人科手術の増加

- 業界の潜在的リスク&課題

- 手続きにかかる費用が高め

- 厳格な規制枠組み

- 市場機会

- 低侵襲手術の需要増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 技術的進歩

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 天然縫合糸

- 合成縫合糸

- ビクリル

- ポリジオキサノン縫合糸(PDS)

- ポリグレカプロン縫合糸(モノクリル)

第6章 市場推計・予測:構造別、2021年~2034年

- 主要動向

- モノフィラメント

- マルチフィラメント

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 心臓血管外科

- 婦人科手術

- 整形外科

- 眼科手術

- 神経外科

- その他の外科手術用途

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 専門クリニック

- 外来手術センター

- その他の用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Advanced Medical Solutions

- B. Braun

- Corza Medical

- CONMED

- Demetech

- Futura Surgicare

- Genesis MedTech

- Healthium Medtech

- Integra Lifesciences

- Johnson &Johnson

- Medtronic

- Lotus Surgicals

- Unisur

- Vital Sutures

- Vitrex Medical Group

目次

The Global Absorbable Surgical Sutures Market was valued at USD 3 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 5.2 billion by 2034. Market growth is being driven by a sharp rise in the number of surgical procedures worldwide, increasing incidences of chronic illnesses, advancements in suture technology, and a surge in gynecological surgeries. The demand for absorbable sutures is also growing as healthcare systems focus more on minimally invasive techniques, faster recovery timelines, and improved patient outcomes. Continuous improvements in materials and technologies, including innovations in coatings and thread structures, are playing a major role in expanding usage across hospitals, surgical centers, and outpatient facilities globally.

Absorbable surgical sutures are designed to naturally break down within the body, removing the need for manual removal and simplifying postoperative care. Enhanced features such as antimicrobial properties, barbed thread structures, and high-performance polymer blends are helping reduce infection risks and accelerate healing. As more clinical practices adopt these advanced tools, the overall efficiency and patient experience improve, reinforcing the product's relevance in modern healthcare. Increasing focus on patient comfort and procedure optimization is positioning absorbable sutures as a preferred choice across multiple surgical specialties.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 5.6% |

The synthetic sutures segment held 71.4% share in 2024, supported by their reliable absorption profiles, high strength retention, and reduced biological reactivity. Materials like polydioxanone (PDO), polylactic acid (PLA), and polyglycolic acid (PGA) offer surgeons precise control over degradation timelines, allowing tailored support during each phase of wound healing. Their adaptability in both open and minimally invasive procedures makes them a trusted solution in high-precision environments.

The hospitals segment held a 55.2% share in 2024. This dominance is linked to expanding hospital infrastructure, especially in high-growth countries, alongside rising chronic disease burdens and enhanced access to surgical technologies. As healthcare systems evolve, newly built and existing hospitals are prioritizing advanced suturing options to improve outcomes, reduce complication rates, and meet modern surgical standards.

United States Absorbable Surgical Sutures Market generated USD 1.1 billion in 2024. Rising chronic conditions and the need for advanced surgical care continue to elevate demand. With a growing number of cardiovascular, oncological, and general surgeries performed annually, there's a strong shift toward sutures that promote faster recovery, lower infection risks, and minimize patient discomfort through natural absorption.

Key players dominating the Global Absorbable Surgical Sutures Market include Demetech, Corza Medical, Futura Surgicare, B. Braun, Medtronic, Unisur, Vitrex Medical Group, Healthium Medtech, Genesis MedTech, Vital Sutures, Advanced Medical Solutions, Lotus Surgicals, Integra Lifesciences, Johnson & Johnson, and CONMED. Companies operating in the absorbable surgical sutures market are strengthening their positions through innovation in biomaterial design and antimicrobial technologies. Firms are focusing on R&D to develop sutures with enhanced tensile strength, controlled degradation rates, and compatibility with minimally invasive techniques. Mergers, acquisitions, and strategic collaborations are being pursued to expand product portfolios and global reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Material trends

- 2.2.3 Structure trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Rising surgical procedures worldwide

- 3.2.1.3 Advancements in suture materials

- 3.2.1.4 Increasing number of gynecological procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of procedures

- 3.2.2.2 Stringent regulatory framework

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for minimally invasive surgeries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Natural suture

- 5.3 Synthetic suture

- 5.3.1 Vicryl

- 5.3.2 Polydioxanone suture (PDS)

- 5.3.3 Poliglecaprone suture (Monocryl)

Chapter 6 Market Estimates and Forecast, By Structure, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Monofilament

- 6.3 Multifilament

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Cardiovascular surgery

- 7.3 Gynaecology surgery

- 7.4 Orthopaedic surgery

- 7.5 Ophthalmic surgery

- 7.6 Neurological surgery

- 7.7 Other surgical applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty clinics

- 8.4 Ambulatory surgical centres

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Advanced Medical Solutions

- 10.2 B. Braun

- 10.3 Corza Medical

- 10.4 CONMED

- 10.5 Demetech

- 10.6 Futura Surgicare

- 10.7 Genesis MedTech

- 10.8 Healthium Medtech

- 10.9 Integra Lifesciences

- 10.10 Johnson & Johnson

- 10.11 Medtronic

- 10.12 Lotus Surgicals

- 10.13 Unisur

- 10.14 Vital Sutures

- 10.15 Vitrex Medical Group

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日