脊椎ロボット手術市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Spine Robotic Surgery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801823

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

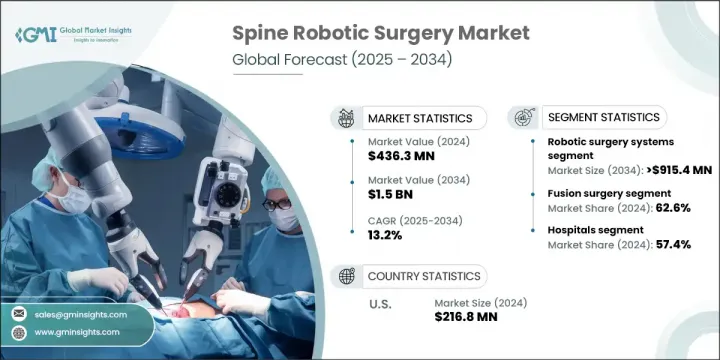

世界の脊椎ロボット手術市場は、2024年には4億3,630万米ドルと評価され、CAGR 13.2%で成長し、2034年には15億米ドルに達すると推定されています。

この大幅な成長は、脊椎疾患の罹患率の上昇、ヘルスケア投資の増加、低侵襲手術への世界のシフトが主な要因です。患者も医療従事者も同様に、回復時間を短縮し、より安全で正確な手技を求めるため、高度な手術オプションに対するニーズは高まり続けています。高齢化が進み、ヘルスケアシステムが進化するにつれて、ロボット支援脊椎手術の需要はさまざまな地域で拡大しています。

手術用ロボットの技術革新は、人工知能、ナビゲーション、リアルタイム画像の開発と相まって、これらのシステムの信頼性を高め、広く採用されるようになっています。これらの技術により、複雑な脊椎手術の精度が向上し、従来の手術法では困難であった治療成績が達成されつつあります。このような進化を遂げる医療現場において、ロボットシステムは安全性と効率性の両方を向上させ、脊椎手術に不可欠な要素になりつつあります。病院や手術センターにおけるロボットシステムの存在感の高まりは、今後10年間の市場の堅調な推移を示唆しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 4億3,630万米ドル |

| 予測金額 | 15億米ドル |

| CAGR | 13.2% |

脊椎ロボット手術は、脊椎手術の実施方法を劇的に改善する制御と精度のレベルを提供します。その低侵襲性は、治癒を早め、合併症のリスクを低減し、外科医と患者の双方にアピールします。ロボットシステムを使用することで、臨床医はより小さく正確な切開を行うことができ、周辺組織への外傷を最小限に抑えることができます。これらのシステムは、手作業では困難な微調整を可能にし、手術ミスの可能性を減らし、より良い結果をもたらします。ヘルスケアは、回復時間の短縮や患者の在院日数の短縮といった恩恵を受け、ひいては医療費全体の削減や手術ワークフローの効率化につながります。

ロボット手術システム部門は2024年に58.3%のシェアを占めました。専門家は、この業績の主な促進要因として、技術的進歩と強力な臨床成果を指摘しています。最新の手術用ロボットは、強化された画像処理、AI主導のプランニング、リアルタイムのナビゲーションを備えており、外科医が非常に複雑な手技を容易に行えるよう支援しています。これは、より正確な手術と再手術のリスクの軽減につながり、多くの施設でロボットプラットフォームが好まれる選択肢となっています。さらに、ロボットシステムは低侵襲手技をサポートするように構築されており、繊細で複雑な作業を支援する高度なツールを提供しています。この精度は手術の質を向上させるだけでなく、外科医の信頼性を高める。

2024年のシェアは62.6%で、これは脊椎治療における融合の継続的な人気を反映しています。脊椎固定術は、特に高齢化やライフスタイルの変化によって脊椎に関連する問題がより一般的になっているため、依然として最も頻繁に行われている手術の1つです。ロボット支援による脊椎固定術は、精度が高く、合併症が少なく、再手術率が低いです。ロボット工学の統合により、これらの手術はより洗練され、慢性的な脊椎疾患を抱える患者にとって、より安全で予知性の高いものとなっています。

米国脊椎ロボット手術2024年の市場規模は2億1,680万米ドル。同地域の優位性は、先進的な病院システム、革新的技術の迅速な導入、研究開発への投資の増加によって後押しされています。米国は、脊椎疾患に罹患する患者が多いことに加え、確立されたインフラと償還の状況により、力強い成長を示しています。これらの要因から、北米はロボット脊椎手術における技術革新の中心地であり、商業上のリーダー的存在となっています。

世界の脊椎ロボット手術市場に影響を与える主要企業には、ジョンソン・エンド・ジョンソン、ジンマー・バイオメット、シーメンス・ヘルティニアーズ、メドトロニック、インテュイティブ・サージカル・オペレーションズ、ストライカー、ブレインラボ、CUREXO、オルソフィックス・メディカル、R2サージカル、Bブラウン、グローバス・メディカルなどがあります。研究開発への継続的な投資と製品革新への注力が、脊髄手術技術の未来を形成しています。市場での存在感を高めるため、脊椎ロボット手術分野の主要企業は継続的なイノベーションと戦略的パートナーシップに注力しています。AI統合、次世代ナビゲーションツール、高度な画像処理機能に多額の投資を行い、精度を高めたシステムを提供しています。その多くは、世界市場でより早く規制当局の承認を得るため、臨床試験パイプラインを拡大しています。病院や学術機関との協働は、トレーニングやデモ施設を提供することで、ロボットプラットフォームの採用を加速するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 脊椎疾患の有病率の増加

- 技術的進歩

- 低侵襲手術の急増

- ヘルスケア費の増加

- 業界の潜在的リスク&課題

- ロボットデバイスの複雑さ

- 厳格な規制要件

- 市場機会

- 新興経済諸国の成長ポテンシャル

- 製品開発のための研究開発への継続的な投資

- 促進要因

- 成長の可能性

- 成長可能性分析

- 償還シナリオ

- 規制情勢

- 米国

- 欧州

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- 新製品開発の情勢

- 起動シナリオ

- 価格分析、2024

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ロボット手術システム

- 完全ロボットシステム

- ロボットアーム支援システム

- 手術ナビゲーションシステム

- 電磁航法システム

- 光学航法システム

- ハイブリッドナビゲーションシステム

- ソフトウェアソリューション

- アクセサリーと消耗品

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 固定手術

- 非固定手術

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- B Braun

- Brainlab

- CUREXO

- Globus Medical

- Intuitive Surgical Operations

- Johnson &Johnson

- Medtronic

- Orthofix Medical

- R2 Surgical

- Siemens Healthineers

- Stryker

- Zimmer Biomet

目次

The Global Spine Robotic Surgery Market was valued at USD 436.3 million in 2024 and is estimated to grow at a CAGR of 13.2% to reach USD 1.5 billion by 2034. This substantial growth is largely driven by the rising incidence of spinal disorders, increased healthcare investment, and a global shift toward minimally invasive surgical procedures. The need for advanced surgical options continues to grow as patients and providers alike seek safer, more accurate procedures that also reduce recovery time. As the aging population increases and healthcare systems evolve, the demand for robot-assisted spinal procedures is expanding across various regions.

Innovations in surgical robotics-combined with developments in artificial intelligence, navigation, and real-time imaging-are making these systems more reliable and widely adopted. These technologies are improving precision during complex spine procedures and enabling outcomes that traditional surgical methods struggle to achieve. In this evolving medical landscape, robotic systems are becoming an essential component of spinal surgery, enhancing both safety and efficiency. Their growing presence in hospitals and surgical centers signals a strong market trajectory through the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $436.3 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 13.2% |

Spine robotic surgery offers a level of control and accuracy that dramatically improves the way spinal procedures are performed. Its minimally invasive nature supports faster healing and lowers complication risks, which appeals to both surgeons and patients. By using robotic systems, clinicians can make smaller, more precise incisions, which helps minimize trauma to surrounding tissue. These systems enable fine-tuned maneuvers that are difficult to replicate manually, reducing the potential for surgical error and delivering better results. Hospitals benefit from reduced recovery times and shorter patient stays, which in turn lowers overall healthcare costs and increases efficiency in surgical workflows.

The robotic surgery systems segment held a 58.3% share in 2024. Experts pointed to technological advancement and strong clinical outcomes as key drivers for this performance. Modern surgical robotics are equipped with enhanced imaging, AI-driven planning, and real-time navigation, helping surgeons perform highly complex procedures with ease. This translates into more precise surgeries and less risk of revision, making robotic platforms a preferred choice in many facilities. Additionally, robotic systems are built to support minimally invasive techniques, offering advanced tools that assist with delicate and intricate tasks. This precision not only improves surgical quality but also boosts surgeon confidence.

The fusion surgery segment accounted for a 62.6% share in 2024, reflecting its continued popularity in spinal treatment. Spinal fusion remains one of the most frequently performed procedures, particularly as spine-related issues become more common with aging populations and lifestyle factors. Robotic-assisted fusion surgeries offer heightened precision, fewer complications, and lower revision rates, all of which contribute to their dominance in this space. The integration of robotics has helped refine these procedures, making them safer and more predictable for patients dealing with chronic spine conditions.

United States Spine Robotic Surgery Market generated USD 216.8 million in 2024. The region's dominance is fueled by advanced hospital systems, quick adoption of innovative technologies, and increasing investments in research and development. The US shows strong growth due to its established infrastructure and reimbursement landscape, alongside a large patient population affected by spine disorders. These factors make North America an innovation hub and commercial leader in robotic spine surgery, drawing interest from companies aiming to expand their global footprint.

Major players influencing the Global Spine Robotic Surgery Market include Johnson & Johnson, Zimmer Biomet, Siemens Healthineers, Medtronic, Intuitive Surgical Operations, Stryker, Brainlab, CUREXO, Orthofix Medical, R2 Surgical, B Braun, Globus Medical, and others. Their continued R&D investments and focus on product innovation are shaping the future of spinal surgery technologies. To build a strong market presence, leading companies in the spine robotic surgery space are focusing on continual innovation and strategic partnerships. They're investing heavily in AI integration, next-gen navigation tools, and advanced imaging capabilities to offer precision-enhanced systems. Many are expanding their clinical trial pipelines to gain regulatory approvals faster across global markets. Collaborations with hospitals and academic institutions are helping accelerate the adoption of robotic platforms by providing training and demonstration facilities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of spinal disorders

- 3.2.1.2 Technological advancements

- 3.2.1.3 Surge in minimally invasive surgical procedures

- 3.2.1.4 Increased healthcare spending

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complexity of robotic devices

- 3.2.2.2 Stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Growth potential in developing economies

- 3.2.3.2 Continued investment in research and development for product development

- 3.2.1 Growth drivers

- 3.3 Growth potential

- 3.4 Growth potential analysis

- 3.5 Reimbursement scenario

- 3.6 Regulatory landscape

- 3.6.1 U.S.

- 3.6.2 Europe

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Future market trends

- 3.9 New product development landscape

- 3.10 Start-up scenario

- 3.11 Pricing analysis, 2024

- 3.12 Gap analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Robotic surgery systems

- 5.2.1 Fully robotic systems

- 5.2.2 Robotic arm-assisted systems

- 5.3 Surgical navigation systems

- 5.3.1 Electromagnetic navigation systems

- 5.3.2 Optical navigation systems

- 5.3.3 Hybrid navigation systems

- 5.4 Software solutions

- 5.5 Accessories and consumables

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Fusion surgery

- 6.3 Non-fusion surgery

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B Braun

- 9.2 Brainlab

- 9.3 CUREXO

- 9.4 Globus Medical

- 9.5 Intuitive Surgical Operations

- 9.6 Johnson & Johnson

- 9.7 Medtronic

- 9.8 Orthofix Medical

- 9.9 R2 Surgical

- 9.10 Siemens Healthineers

- 9.11 Stryker

- 9.12 Zimmer Biomet

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日