|

市場調査レポート

商品コード

1684113

脊椎ロボット手術:市場シェア分析、産業動向&統計、成長予測(2025年~2030年)Spine Robotic Surgery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 脊椎ロボット手術:市場シェア分析、産業動向&統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 113 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

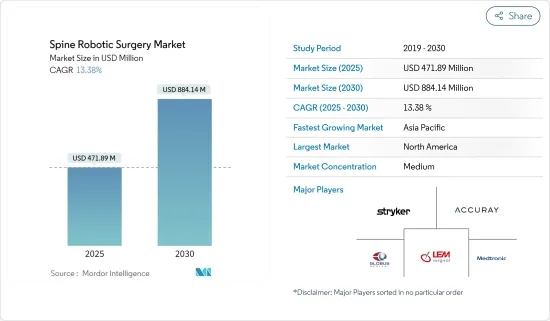

脊椎ロボット手術市場規模は、2025年に4億7,189万米ドルと推定され、予測期間(2025年~2030年)のCAGRは13.38%で、2030年には8億8,414万米ドルに達すると予測されます。

脊椎ロボット手術市場は、技術の進歩、新規参入、低侵襲手術への嗜好の高まりといった要因の中で、堅調な成長機会が見込まれています。また、脊椎疾患の負担が増加していることから、調査期間中の市場拡大がさらに加速すると予想されます。

ロボット工学の技術的進歩の増加は、調査期間中の市場成長を促進すると予想される主な要因の1つです。脊椎手術における支援技術の大幅な進歩は、器具装着時の精度、正確さ、信頼性を高めるために行われてきました。脊椎外科手術では、血管や神経系の合併症を回避し、癒合のための固定を最大化するために、正確なスクリューの配置が重要です。

ロボット工学の応用により、スクリュー留置の精度を含む脊椎手術の手順全体が大幅に改善され、より良い治療成績につながっています。従って、このような進歩は調査期間中の市場成長を押し上げると予想されます。

さらに、脊椎ロボットの新興企業の台頭や、脊椎ロボットを変革するためのいくつかの戦略的買収が、市場成長をさらに押し上げると予想されます。例えば、2023年4月、Alphatec Holdings Inc.は、非上場の医療技術Accelus Inc.からREMI Robotic Navigation Systemを5,500万米ドルで買収しました。REMI(Robotic-Enabled Minimally Invasive)システムは、3D画像スキャンまたは2D透視患者画像のいずれかを利用することで、脊椎手術にナビゲーションとロボティクスを統合する術中プラットフォームです。このように、脊椎外科ロボットを変革するための戦略的買収は、調査期間中の市場成長を促進すると予測されます。

さらに、脊椎手術におけるロボット脊椎プラットフォームに関連するその他の特典も、調査期間中の市場成長を加速すると予測される要因です。例えば、中国国家自然科学基金(National Natural Science Foundation of China)の助成金によって支援され、EFORT Open Reviewsに掲載された2023年11月の研究によると、従来技術のペディクル・スクリューの誤配置率は腰椎と胸椎でそれぞれ30%と55%であるのに対し、ロボット支援によるペディクル・スクリューの配置では91.5%~94.4%の成功率が報告されています。このように、ロボットプラットフォームは精度が高く、利点が多いため、予測期間中に普及が進むと予想されます。

さらに、市場参入企業が事業強化のために行っているいくつかの戦略的イニシアチブは、市場成長を加速させると予測されています。例えば、2023年10月、Spine Wave社とeCential Robotics社は、新しいロボットベースの脊椎手術プラットフォームを開発、市場開拓、商業化するための協働契約に調印しました。したがって、このような開発は、調査期間中の市場成長を後押しすると予想されます。

このように、技術の進歩、低侵襲手術に対する需要の高まり、市場参入企業によるいくつかの戦略的イニシアティブなど、上記の要因は、予測期間中の市場成長を押し上げると予想されます。しかし、新興国での手術費用の高さや普及の遅れが、調査期間中の業界拡大を妨げると予測されています。

脊椎ロボット手術市場の動向

システムセグメントは予測期間中に指数関数的な成長が見込まれる

システムセグメントには、手術ロボットとナビゲーションシステムが含まれます。ロボット技術の進歩や主要な市場参入企業による取り組みなどの要因が、予測期間中の市場成長を増加させると予想されます。

また、手術ロボットやナビゲーションシステムに関連するその他の特典や、ヘルスケア施設全体への設置が増加していることは、業界の拡大を加速すると予想される重要な要因の一部です。例えば、2023年11月、Mercy Hospital Northwest Arkansasは、脊椎手術を支援し、ヒューマンエラーの可能性を低減するMazor Xロボットの追加を発表しました。外科医は、ロボットが手術前にネジの配置を計画するのにも役立ち、手術室でのワークフローを大幅に改善できると期待しています。

さらに2023年8月、アラバマ大学バーミンガム校(UAB)は、器具の設置や脊椎の変性疾患の治療のために、グローバス・メディカル社のExcelsiusGPS脊椎ロボットを導入したと発表しました。UABはまた、2023年初頭にロボット手術件数が20,000件を突破したと主張しています。このような動向は、脊椎手術におけるロボットの利用が増加していることを示しており、セグメント成長の原動力にもなると予想されています。

さらに、脊椎ロボットナビゲーションシステムの進歩や資金調達機会の増加は、調査期間中にセグメントの取り込みをさらに加速させると予想されています。例えば、2024年4月、SpinEM Roboticsは脊椎手術のイノベーションに注力するSpineartから1,100万米ドルの戦略的投資を受けました。この戦略的パートナーシップにより、前者の高度なナビゲーションとロボット支援技術と後者の手術ソリューションの専門知識が融合されると期待されています。このような開発により、予測期間中に同分野の市場拡大が加速するものと思われます。

このように、ロボット技術の進歩や主要市場プレイヤーの取り組みなど、上記の要因は予測期間中の市場成長を増加させると予想されます。

北米は予測期間中に脊椎ロボット手術市場の健全な成長を示すと予測される

北米は、脊髄損傷や変形の有病率の上昇、技術進歩の増加、低侵襲手術に対する需要の高まり、業界参加者によるいくつかの戦略的イニシアチブの中で、有利な成長機会になることが期待されます。

変性疾患、脊椎変形、脊髄損傷、脊椎外傷などの脊椎疾患の有病率は北米地域で上昇傾向にあります。このため、これらの症状を効果的に治療するための高度な外科的介入に対する需要が高まっています。例えば、Spinal Cord, Inc.の2023年5月の報告書によると、米国では毎年約18,000件の脊髄損傷が新たに発生しており、年間発生率は100万人当たり54件です。

このように、同国における脊髄損傷の負担が憂慮すべきほど増加していることから、このような状態を管理するための革新的な外科的介入に対する需要が促進されると予想され、その結果、調査期間中の市場成長が加速すると予測されます。

加えて、脊椎外傷やその他の奇形の管理における脊椎ロボット手術の役割が証明されていることから、調査期間中の市場成長はさらに加速すると予測されます。例えば、2023年9月にNorth American Spine Society Journalによって発表された論文によると、脊椎手術におけるロボット支援は、外傷性骨折の患者に安全に実施することができ、ロボット支援による器具固定は、そのような脊椎外傷に役立ちます。このように、脊椎手術におけるロボットプラットフォームの役割は実証されており、今後数年間で業界の成長が加速すると予測されます。

さらに、低侵襲手術(MIS)の需要が高まっており、ロボット脊椎手術の応用が増加しています。例えば、2022年11月にCanadian Journal for Surgeryが発表したレポートによると、低侵襲手術は入院期間、痛み、手術部位感染などの合併症を減少させる。そのため、患者はより小さな切開、より早い回復時間、痛みの軽減を提供する手術をますます求めるようになっています。このように、低侵襲手術の普及は、調査期間中の市場成長を加速させると予測されています。

また、主要な市場参入企業による最近の動向は、調査期間中の市場成長をさらに加速させると予想されます。例えば、2022年9月、Stryker社は米国で脊椎用Q Guidance Systemを発売しました。新しく発売されたシステムは、脊椎手術のための強固なナビゲーションとプランニング機能を備えています。したがって、このような開発は、調査期間中の市場成長を後押しすると予想されます。

このように、脊椎疾患の大きな負担、技術の進歩、低侵襲手術の需要の増加、市場参入企業によるいくつかの戦略的イニシアティブなど、上記の要因は、調査期間にわたってこの地域の市場成長を促進すると予想されます。

脊椎ロボット手術産業の概要

脊椎ロボット手術市場の競争は中程度で、複数の大手企業が参入しています。これらの企業は、戦略的提携を確立し、この世界市場で事業展開している他の企業と協力しています。したがって、市場参入企業によるこのような戦略的イニシアチブは、調査期間中、業界の市場成長を促進すると予測されます。同市場で事業を展開している主要企業には、Stryker、Accuray Incorporated、Medtronic、Lem Surgical Ag、Zimmer Biometなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 技術的進歩の高まりと新規市場企業の参入

- 低侵襲手術に対する嗜好の高まり

- 市場抑制要因

- 厳しい規制プロセスおよびデバイスの高コスト

- 業界の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- システム

- 手術ロボット

- ナビゲーションシステム

- 消耗品およびアクセサリー

- ソフトウェアとサービス

- システム

- 用途別

- 融合手術

- 非融合手術

- エンドユーザー別

- 病院

- 外来手術センター

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Stryker

- Accuray Incorporated

- Medtronic

- Lem Surgical Ag

- Brainlab Ag

- Globus Medical, Inc.

- Zimmer Biomet

- Curexo, Inc

- Point Robotics Medtech Inc.

- Beijing Tinavi Medical Technologies Co., Ltd.

- Nanjing Perlove Medical Equipment Co., Ltd.

第7章 市場機会と今後の動向

The Spine Robotic Surgery Market size is estimated at USD 471.89 million in 2025, and is expected to reach USD 884.14 million by 2030, at a CAGR of 13.38% during the forecast period (2025-2030).

The spine robotic surgery market is expected to witness robust growth opportunities amid factors such as rising technological advancements, the entry of new market players, and the rising preference for minimally invasive surgeries. In addition, the growing burden of spinal disorders is further expected to accelerate market expansion over the study period.

The increasing technological advancements in robotics are one of the major factors expected to foster market growth over the study period. Significant advancements in assistive technology in spine surgery have been made to enhance accuracy, precision, and reliability during instrumentation. Accurate screw placement is critical in spinal surgery to avoid vascular or neurologic complications and to maximize fixation for fusion.

The application of robotics has significantly improved the entire procedure of spinal surgery, including accuracy of screw placements, leading to better outcomes. Thus, such advancements are expected to boost market growth over the study period.

Moreover, the rise of spine robotic start-ups and several strategic acquisitions to transform spinal robotics are further expected to boost market growth. For instance, in April 2023, Alphatec Holdings Inc. acquired the REMI Robotic Navigation System from the privately held medtech Accelus Inc. for USD 55 million. REMI (Robotic-Enabled Minimally Invasive) System is an intra-operative platform that integrates navigation and robotics into spine procedures by utilizing either a 3D imaging scan or 2D fluoroscopic patient images. Thus, such strategic acquisitions to transform spine surgical robotics are projected to facilitate market growth over the study period.

In addition, several benefits associated with robotic spine platforms in spine surgeries are another factor projected to accelerate market growth over the study period. For instance, as per the November 2023 study supported by a grant from the National Natural Science Foundation of China and published in EFORT Open Reviews, the pedicle screw misplacement rates of conventional techniques are 30% and 55% in the lumbar and thoracic spines, respectively, while robot-assisted pedicle screw placement reported a success rate of 91.5% to 94.4%. Thus, the greater precision and benefits associated with robotic platforms are expected to bolster their adoption over the forecast period.

Furthermore, several strategic initiatives undertaken by industry participants to strengthen their business avenues are projected to accelerate market growth. For instance, in October 2023, Spine Wave and eCential Robotics signed a collaboration agreement to develop, market, and commercialize novel robotics-based spine surgery platforms. Thus, such developments are expected to boost market growth over the study period.

Thus, the above-mentioned factors, like technological advancements, growing demand for minimally invasive surgeries, and several strategic initiatives undertaken by market players, are expected to boost market growth over the forecast period. However, the high cost of procedures and slow uptake in in emerging economies is projected to hinder industry expansion over the study period.

Spine Robotic Surgery Market Trends

System Segment is Expected to Register an Exponential Growth Over the Forecast Period

The system segment includes surgical robots and navigation systems. Factors such as advancements in robotic technology and initiatives undertaken by key market players are expected to increase market growth over the forecast period.

In addition, several benefits associated with surgical robots and navigation systems and their increasing installation across healthcare facilities are some of the significant factors expected to accelerate industry expansion. For instance, in November 2023, Mercy Hospital Northwest Arkansas announced the addition of a Mazor X robot to assist with spinal surgeries and reduce the chances of human error. The surgeons anticipate that the robot can also aid with planning the placement of the screws before surgery and can create a much better workflow in the operating room.

Moreover, in August 2023, the University of Alabama at Birmingham (UAB) announced the addition of an ExcelsiusGPS spine robot from Globus Medical for instrument placement and treating degenerative conditions in the spine. UAB also claimed that the institution surpassed 20,000 robotic surgeries in early 2023. Such trends indicate the rising usage of robots for spine surgery and are also anticipated to drive segmental growth.

Furthermore, advancements in spinal robotic navigation systems and increasing funding opportunities are further expected to accelerate segment uptake over the study period. For instance, in April 2024, SpinEM Robotics secured a USD 11 million strategic investment from Spineart, which focuses on spine surgery innovation. This strategic partnership is expected to combine the former's advanced navigation and robotic assistance technology with the latter's expertise in surgical solutions. Thus, such developments are poised to accelerate segment uptake over the forecast period.

Thus, the above-mentioned factors, such as advancements in robotic technology and initiatives undertaken by key market players, are expected to increase market growth over the forecast period.

North America is Projected to Witness Healthy Growth in The Spine Robotic Surgery Market During the Forecast Period

North America is expected to witness lucrative growth opportunities amid a rise in the prevalence of spinal cord injuries and deformities, the increase in technological advancements, the growing demand for minimally invasive surgery procedures, and several strategic initiatives undertaken by industry participants.

The prevalence of spine disorders, such as degenerative conditions, spinal deformities, spinal cord injuries, and spinal trauma, is on the rise in the North American region. This has led to a growing demand for advanced surgical interventions to treat these conditions effectively. For instance, according to a May 2023 report of Spinal Cord, Inc., around 18,000 new spinal cord injuries occur each year in the United States, with an annual incidence rate of 54 per 1 million.

Thus, such an alarming increase in the burden of spinal cord injuries in the country is expected to foster demand for innovative surgical interventions to manage such conditions, which, in turn, is projected to accelerate market growth over the study period.

In addition, the proven role of spinal robotic surgeries in the management of spinal trauma and other deformities is further projected to accelerate market growth over the study period. For instance, according to an article published by the North American Spine Society Journal in September 2023, robotic assistance in spinal surgery can be safely implemented in patients with traumatic fractures, and robot-assisted instrumented fusion can be helpful in such spinal traumas. Thus, the proven role of robotic platforms in spine surgeries is projected to accelerate industry growth over the coming years.

Furthermore, there is a growing demand for Minimally Invasive Surgery (MIS), leading to a rise in the application of robotic spinal surgeries. For instance, according to a report published by the Canadian Journal for Surgery in November 2022, minimally invasive surgery decreases length of stay, pain, and complications such as surgical site infection. Therefore, patients increasingly seek procedures offering smaller incisions, faster recovery times, and reduced pain. Thus, the increasing uptake of minimally invasive surgical procedures is projected to accelerate market growth over the study period.

Also, several recent developments undertaken by key industry participants are further expected to accelerate market growth over the study period. For instance, In September 2022, Stryker launched the Q Guidance System for spine applications in the United States. The newly launched system has robust navigation and planning capabilities for spinal surgeries. Thus, such developments are expected to boost market growth over the study period.

Thus, the above-mentioned factors, like the significant burden of spinal disorders, growing technology advancements, increasing demand for minimally invasive procedures, and several strategic initiatives undertaken by market participants, are expected to foster the region's market growth over the study period.

Spine Robotic Surgery Industry Overview

The spine robotic surgery market is moderately competitive and consists of several major players. They are engaged in establishing a strategic alliance and collaborating with other companies operating in this global market. Thus, such strategic initiatives undertaken by market participants are projected to foster the industry's market growth over the study period. Some of the key players operating in the market are, Stryker, Accuray Incorporated, Medtronic, Lem Surgical Ag, Zimmer Biomet among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Technological Advancements And Entry Of New Market Players

- 4.2.2 Rising Preference For Minimally Invasive Surgeries

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Processes And High Cost Of Devices

- 4.4 Industry Attractiveness- Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product Type

- 5.1.1 System

- 5.1.1.1 Surgical Robot

- 5.1.1.2 Navigation System

- 5.1.2 Consumables And Accessories

- 5.1.3 Software And Services

- 5.1.1 System

- 5.2 By Application

- 5.2.1 Fusion Surgery

- 5.2.2 Non-fusion Surgery

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle-East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Stryker

- 6.1.2 Accuray Incorporated

- 6.1.3 Medtronic

- 6.1.4 Lem Surgical Ag

- 6.1.5 Brainlab Ag

- 6.1.6 Globus Medical, Inc.

- 6.1.7 Zimmer Biomet

- 6.1.8 Curexo, Inc

- 6.1.9 Point Robotics Medtech Inc.

- 6.1.10 Beijing Tinavi Medical Technologies Co., Ltd.

- 6.1.11 Nanjing Perlove Medical Equipment Co., Ltd.