|

市場調査レポート

商品コード

1801806

アナログフロントエンドIC市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Analog Front-End (AFE) IC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| アナログフロントエンドIC市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年08月07日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

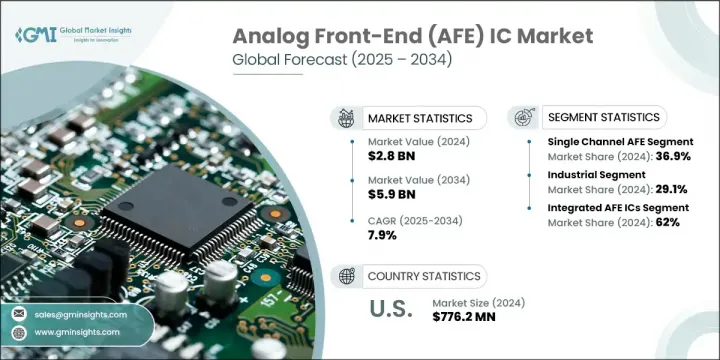

世界のアナログフロントエンドIC市場は、2024年には28億米ドルとなり、CAGR 7.9%で成長し、2034年には59億米ドルに達すると推定されます。

この成長の主な要因は、ウェアラブル携帯医療機器、産業オートメーション、無線通信システムの進歩に対する需要の高まりです。プログラマブルでマルチチャネルのAFE ICへの依存度が高まっていることが、ヘルスケア、自動車、産業分野でのよりスマートなセンサーシステムの開発に寄与しています。IoTシステムの高度化に伴い、リアルタイムのアナログ信号処理が重要になっています。

小型でエネルギー効率に優れたAFE ICの登場により、ウェアラブル医療機器や埋め込み型医療機器での採用が加速しており、電力を節約しながら継続的な生体信号モニタリングを可能にし、患者の快適性を高めています。自動車や輸送機関では、ADASや電子車両システムの進化により、過酷な環境条件下で動作する高信頼性、高精度重視のAFE ICへの需要が高まっています。さらに、航空宇宙分野の電動化と自動化の動向は、センサー・フュージョンとレーダー・インターフェイス・ソリューションへの要求を高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 28億米ドル |

| 予測金額 | 59億米ドル |

| CAGR | 7.9% |

マルチチャネルAFE分野はAFE IC市場で最も急成長を遂げており、2025~2034年のCAGRは9.4%と予測されます。この加速は、自動車安全システム、産業用モニタリング、高度医療診断などの分野で複雑なセンサーネットワークの統合が進んでいることが主な要因です。このようなニーズに対応するため、開発者はデジタル・インターフェイスを内蔵したコンフィギュラブルで低ノイズのAFE ICに注力する必要があります。ミッションクリティカルな分野に合わせた小型で電力効率の高いマルチチャネル・ソリューションを設計するメーカーは、競争力を維持し、より広範な採用を獲得できると思われます。

自動車・輸送分野は、2034年までCAGR 10%で成長すると予想されます。電気自動車とADAS技術の急速な進歩により、レーダー、カメラ、ライダーシステムからの正確なデータ取得を可能にする低ノイズ、マルチチャネルAFE ICの需要が高まっています。さらに、正確なバッテリ・モニタリング・システムは電気自動車に不可欠であり、厳しい安全性と信頼性の基準を満たすように構築された車載グレードのアナログフロントエンドソリューションの必要性が高まっています。

米国のアナログフロントエンド(AFE)IC市場は、2024年に7億7,620万米ドルを創出しました。同国の成長は、半導体技術革新におけるリーダーシップと、ヘルスケア診断、オートメーション、自動車エレクトロニクス分野からの強い需要が後押ししています。ウェアラブル医療技術や車載センサーの市場が拡大する中、米国のメーカーは、小型で規制基準に準拠した低消費電力、高集積のAFEを開発することを優先しなければならないです。製品開発、ローカライゼーション、市場開拓の迅速化には、国内OEMやヘルスケア技術プロバイダーとの戦略的協力が不可欠です。

世界のアナログフロントエンド(AFE)IC市場で事業を展開する主要企業には、NXPセミコンダクターズ、Monolithic Power Systems, Inc.、Texas Instruments Incorporated、Analog Devices Inc.、Infineon Technologies AG、STマイクロエレクトロニクス、Microchip Technology Inc.、日清紡マイクロデバイスなどがあります。アナログフロントエンドIC市場の主要企業は、小型化と消費電力の削減を図りながら、製品性能の向上に注力しています。デジタル統合をサポートし、優れた信号忠実度を実現するマルチチャネル、低ノイズAFEによるポートフォリオの拡大が優先課題となっています。

また、ウェアラブルや車載モジュールなど、スペースに制約のあるアプリケーション向けの高密度集積を可能にするため、先進パッケージング技術への投資も進めています。多様なエンドユーザー要件に対応するため、各社は産業用IoT、ヘルスケア診断、電気自動車など特定の垂直分野向けに製品をカスタマイズしています。さらに、サプライチェーンの効率を最適化し、市場へのリーチを向上させるため、企業はOEM、半導体鋳造、地域ディストリビューターと戦略的提携を結んでいます。これらの戦略は、技術革新サイクルの加速、顧客の設計の複雑さの軽減、主要成長地域におけるブランドポジショニングの強化に役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 影響要因

- 促進要因

- ポータブルおよびウェアラブル医療機器の成長

- 産業オートメーションとIIoTの拡大

- より高いチャネル密度と柔軟性に対するニーズの高まり

- 無線通信と高速通信の進歩

- 車載エレクトロニクスとADASの拡大

- 業界の潜在的リスク&課題

- 設計の複雑さとコスト圧力が高め

- サプライチェーンの不安定さと半導体不足

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 特許および知的財産分析

- 地政学と貿易のダイナミクス

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 市場集中分析

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダーたち

- 課題者たち

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- シングルチャンネルAFE

- デュアルチャンネルAFE

- マルチチャンネルAFE

第6章 市場推計・予測:アーキテクチャ別、2021年~2034年

- 主要動向

- ディスクリートAFE IC

- 統合AFE IC

- ハイブリッドAFE IC

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 産業

- プロセス自動化および制御システム

- ロボット工学とモーションシステム

- エネルギーおよび電力監視システム

- 産業用データ収集および計測

- その他

- 自動車・輸送

- ADAS

- EVバッテリー管理システム

- 車載インフォテインメントとテレマティクス

- モーター制御とパワートレイン

- その他

- 医療・ヘルスケア機器

- 患者モニタリング機器

- 診断画像システム

- 埋め込み型およびウェアラブルデバイス

- 研究室および臨床機器

- その他

- 通信機器

- 無線基地局とスモールセル

- RFフロントエンドとトランシーバー

- 光通信モジュール

- ネットワーク監視およびテスト機器

- その他

- 家電製品とウェアラブル

- オーディオと音声処理

- イメージングおよびカメラモジュール

- 健康とフィットネスのウェアラブル

- スマートホームとIoTデバイス

- その他

- 航空宇宙および防衛

- レーダーおよび電子戦システム

- 航空電子機器および飛行制御システム

- 安全な通信モジュール

- ナビゲーションおよび測位システム

- その他

- 試験、測定、計測機器

- オシロスコープとアナライザ

- データロガーとハンドヘルドテストデバイス

- 科学・環境機器

- 校正システム

- その他

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- 世界の主要企業

- Analog Devices Inc.

- Texas Instruments Incorporated

- STMicroelectronics

- Infineon Technologies AG

- NXP Semiconductors

- ROHM Co., Ltd.

- Microchip Technology Inc.

- 地域別主要企業

- 北米

- Cirrus Logic, Inc.

- Monolithic Power Systems, Inc.

- Onsemi

- MaxLinear

- 欧州

- ams-OSRAM AG

- Ricoh

- アジア太平洋地域

- Nisshinbo Micro Devices Inc.

- Renesas Electronics Corporation

- Hycon Technology Corp

- SINOWEALTH Electronic Ltd.

- 北米

- ディスラプター/ニッチ企業

- Qorvo

- Asahi Kasei Microdevices Corporation

- Trusignal Microelectronics

The Global Analog Front-End IC Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 5.9 billion by 2034. This growth is primarily driven by rising demand for wearable and portable medical devices, industrial automation, and advancements in wireless communication systems. Increasing reliance on programmable and multi-channel AFE ICs is contributing to the development of smarter sensor systems across healthcare, automotive, and industrial sectors. As IoT systems become more advanced, real-time analog signal processing is becoming critical.

The emergence of compact, energy-efficient AFE ICs is accelerating adoption in wearable and implantable medical devices, enabling continuous biosignal monitoring while conserving power and enhancing patient comfort. In automotive and transportation, the evolution of ADAS and electronic vehicle systems is intensifying demand for high-reliability, precision-focused AFE ICs that perform under extreme environmental conditions. Additionally, the aerospace sector's electrification and automation trends are boosting requirements for sensor fusion and radar interface solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 7.9% |

The multi-channel AFE segment is experiencing the fastest growth in the AFE IC market, projected to grow at a CAGR of 9.4% between 2025 and 2034. This acceleration is largely driven by rising integration of complex sensor networks in sectors such as automotive safety systems, industrial monitoring, and advanced medical diagnostics. To meet these needs, developers must focus on configurable, low-noise AFE ICs with built-in digital interfaces. Manufacturers that design compact, power-efficient multi-channel solutions tailored to mission-critical sectors will remain competitive and gain broader adoption.

The automotive and transportation segment is expected to grow at a CAGR of 10% throughout 2034. Rapid advancements in electric vehicles and ADAS technologies are fueling the demand for low-noise, multi-channel AFE ICs that enable precise data acquisition from radar, camera, and lidar systems. Additionally, accurate battery monitoring systems are essential in EVs, driving the need for automotive-grade analog front-end solutions built to meet stringent safety and reliability standards.

U.S. Analog Front-End (AFE) IC Market generated USD 776.2 million in 2024. Growth across the country is fueled by its leadership in semiconductor innovation, and strong demand from healthcare diagnostics, automation, and automotive electronics sectors. With the growing market for wearable health tech and automotive sensors, manufacturers in the U.S. must prioritize developing low-power, highly integrated AFEs that are both compact and compliant with regulatory standards. Strategic collaboration with domestic OEMs and healthcare technology providers is essential to accelerate product development, localization, and faster time-to-market.

Key players operating in the Global Analog Front-End (AFE) IC Market include NXP Semiconductors, Monolithic Power Systems, Inc., Texas Instruments Incorporated, Analog Devices Inc., Infineon Technologies AG, STMicroelectronics, Microchip Technology Inc., and Nisshinbo Micro Devices Inc. Leading companies in the analog front-end IC market are focusing on enhancing product performance while reducing size and power consumption. Priorities include expanding portfolios with multi-channel, low-noise AFEs that support digital integration and deliver superior signal fidelity.

Firms are also investing in advanced packaging technologies to enable high-density integration for space-constrained applications like wearables and automotive modules. To address diverse End user requirements, players are tailoring products for specific verticals such as industrial IoT, healthcare diagnostics, and electric vehicles. Additionally, companies are forming strategic alliances with OEMs, semiconductor foundries, and regional distributors to optimize supply chain efficiency and improve market reach. These strategies help accelerate innovation cycles, reduce design complexity for clients, and strengthen brand positioning across key growth regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Architecture trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of portable & wearable medical devices

- 3.2.1.2 Expansion of industrial automation & IIoT

- 3.2.1.3 Rising need for higher channel density & flexibility

- 3.2.1.4 Advancements in wireless & high-speed communications

- 3.2.1.5 Expansion of automotive electronics and ADAS

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High design complexity and cost pressure

- 3.2.2.2 Supply chain volatility and semiconductor shortages

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates & Forecast, By Product, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Single channel AFE

- 5.3 Dual channel AFE

- 5.4 Multi channel AFE

Chapter 6 Market Estimates & Forecast, By Architecture, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Discrete AFE ICs

- 6.3 Integrated AFE ICs

- 6.4 Hybrid AFE ICs

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Industrial

- 7.2.1 Process automation & control systems

- 7.2.2 Robotics & motion systems

- 7.2.3 Energy & power monitoring systems

- 7.2.4 Industrial data acquisition & instrumentation

- 7.2.5 Others

- 7.3 Automotive & transportation

- 7.3.1 ADAS

- 7.3.2 EV battery management systems

- 7.3.3 In-vehicle infotainment & telematics

- 7.3.4 Motor control & powertrain

- 7.3.5 Others

- 7.4 Medical & healthcare devices

- 7.4.1 Patient monitoring equipment

- 7.4.2 Diagnostic imaging systems

- 7.4.3 Implantable & wearable devices

- 7.4.4 Laboratory & clinical instrumentation

- 7.4.5 Others

- 7.5 Telecom & communication equipment

- 7.5.1 Wireless base stations & small cells

- 7.5.2 RF front-ends & transceivers

- 7.5.3 Optical communication modules

- 7.5.4 Network monitoring & test equipment

- 7.5.5 Others

- 7.6 Consumer electronics & wearables

- 7.6.1 Audio & voice processing

- 7.6.2 Imaging & camera modules

- 7.6.3 Health & fitness wearables

- 7.6.4 Smart home & IoT devices

- 7.6.5 Others

- 7.7 Aerospace & defense

- 7.7.1 Radar & electronic warfare systems

- 7.7.2 Avionics & flight control systems

- 7.7.3 Secure communication modules

- 7.7.4 Navigation & positioning systems

- 7.7.5 Others

- 7.8 Test, measurement & instrumentation

- 7.8.1 Oscilloscopes & analyzers

- 7.8.2 Data loggers & handheld test devices

- 7.8.3 Scientific & environmental instruments

- 7.8.4 Calibration systems

- 7.8.5 Others

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Analog Devices Inc.

- 9.1.2 Texas Instruments Incorporated

- 9.1.3 STMicroelectronics

- 9.1.4 Infineon Technologies AG

- 9.1.5 NXP Semiconductors

- 9.1.6 ROHM Co., Ltd.

- 9.1.7 Microchip Technology Inc.

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Cirrus Logic, Inc.

- 9.2.1.2 Monolithic Power Systems, Inc.

- 9.2.1.3 Onsemi

- 9.2.1.4 MaxLinear

- 9.2.2 Europe

- 9.2.2.1 ams-OSRAM AG

- 9.2.2.2 Ricoh

- 9.2.3 Asia Pacific

- 9.2.3.1 Nisshinbo Micro Devices Inc.

- 9.2.3.2 Renesas Electronics Corporation

- 9.2.3.3 Hycon Technology Corp

- 9.2.3.4 SINOWEALTH Electronic Ltd.

- 9.2.1 North America

- 9.3 Disruptors/Niche Players

- 9.3.1 Qorvo

- 9.3.2 Asahi Kasei Microdevices Corporation

- 9.3.3 Trusignal Microelectronics