乳製品および大豆食品市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Dairy and Soy Food Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801797

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

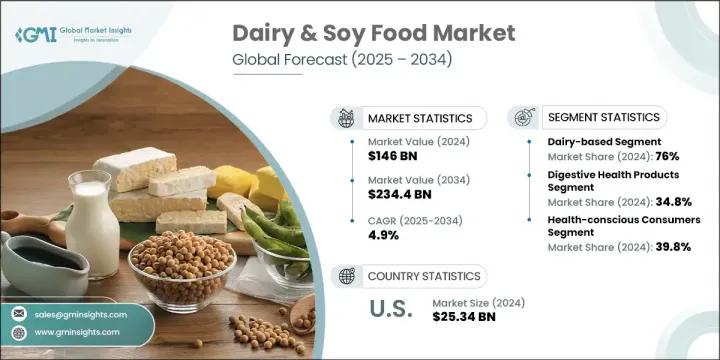

世界の乳製品および大豆食品市場の2024年の市場規模は1,460億米ドルで、CAGR 4.9%で成長し、2034年には2,344億米ドルに達すると推定されます。

この市場には、牛乳、ヨーグルト、チーズなどの乳製品、植物性飲料、大豆代替食品など、幅広い製品が含まれます。この成長の主な原動力は、消費者の間で健康とウェルネスへの関心が高まっていることです。添加物を最小限に抑え、より機能的な利点を備えた栄養価の高い製品に対する需要が高まっています。乳糖不耐症が一般的になるにつれ、多くの消費者が従来の乳製品と同じ味、食感、栄養価を提供する植物由来の選択肢に目を向けています。

植物性と菜食主義者の台頭は、この分野での大きな技術革新の火付け役となり、各社は菜食主義者、フレキシタリアン、環境意識の高い買い物客向けに、新しいタイプのヨーグルト、植物性飲料、栄養強化商品など、ポートフォリオを多様化しています。先進諸国では人口の高齢化も進んでおり、特に骨の健康、消化、総合的な活力をサポートするタンパク質、ビタミン、プロバイオティクスを強化した乳製品や大豆食品への需要が高まっています。一方、eコマースの急成長により製品へのアクセスが改善され、ブランドはより多くの消費者にリーチし、より多様な製品を提供できるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,460億米ドル |

| 予測金額 | 2,344億米ドル |

| CAGR | 4.9% |

2024年には、乳製品ベースの健康食品部門が76%の最大シェアを占め、2034年まで5.3%の成長率を維持すると予想されます。腸の健康、免疫力、骨の強さに重点を置く健康志向の消費者にアピールするこれらの製品は、食事制限のある個人の利用しやすさを高めながら、脂肪分と糖分の含有量を減らすことを目的とした革新的技術で開発されています。

消化器系健康製品セグメントは、2024年に市場で34.8%のシェアを獲得し、2034年までの成長率は5.5%と予想されています。この目覚しい拡大は、腸の健康と免疫システムの強化に消費者の関心が高まっていることが主因であり、栄養と機能性の両方のメリットを提供する製品を求める個人が増加しているためです。膨満感や消化不良からIBSのような複雑な症状まで、消化器系の健康問題が世界的に広まるにつれて、消費者はより良い消化と全体的な腸内細菌叢のバランスを促進する食品やサプリメントに注目するようになっています。

米国の乳製品および大豆食品市場規模は2024年に253億4,000万米ドルとなりました。同国の市場は、安全性、栄養表示の透明性、利便性の高い製品形態を優先するブランドに対する消費者の信頼が原動力となり、2034年までにCAGR 6.4%の成長が見込まれます。オーガニック、グルテンフリー、植物由来の製品の人気が高まっていることも、米国市場をさらに前進させています。

世界乳製品および大豆食品市場の主要企業には、Danone S.A.、Unilever PLC、Lactalis Group、Fonterra Co-operative Group、Hain Celestial Group, Inc.、FrieslandCampina、General Mills, Inc.、Dean Foods Company、Arla Foods amba、Silk(Danone)、Nestle S.A.、The Kraft Heinz Company、株式会社ヤクルト本社、WhiteWave Foods(Danone)、Kellogg Companyなどがあります。競争の激しい乳製品および大豆食品分野で地位を固めるため、各社は様々な戦略を実施しています。これには、低糖質、高タンパク質、乳糖不使用の選択肢の提供など、進化する消費者の嗜好に対応するための継続的な製品改良が含まれます。多くの企業は、植物由来の代替品を含む製品ラインを拡大し、ビーガンやフレキシタリアン向けの選択肢に対する需要の高まりを取り込んでいます。パートナーシップ、買収、生産プロセスの革新も、ポートフォリオを多様化し、製品の入手しやすさを向上させるための重要な戦略となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 健康とウェルネス意識の高まり

- 乳糖不耐症の有病率の上昇

- 植物由来の食事の採用とビーガン主義の拡大

- タンパク質強化と栄養強化の需要

- 業界の潜在的リスク&課題

- 伝統的な酪農業界の競合

- 専門健康製品の価格プレミアム

- 市場機会

- 新興市場における健康意識の向上

- 機能性食品と栄養補助食品の統合

- パーソナライズされた栄養とカスタマイズ

- eコマースと消費者直販の成長

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 価格動向

- 地域別

- 製品カテゴリー別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:商品カテゴリー別、2021年~2034年

- 主要動向

- 乳製品ベースの健康食品

- プロバイオティクス乳製品

- タンパク質強化乳製品

- 機能性乳製品

- 大豆ベースの食品

- 伝統的な大豆食品

- 豆乳と飲料

- 大豆タンパク質製品

- 複合製品とハイブリッド製品

- 乳製品と大豆のブレンド製品

- マルチタンパク質配合

- 機能性食品の組み合わせ

- 特殊栄養製品

第6章 市場推計・予測:健康効果別、2021年~2034年

- 主要動向

- 消化器系の健康製品

- プロバイオティクスとプレバイオティクス食品

- 消化酵素強化

- 腸の健康をサポートする製品

- 骨と関節の健康

- カルシウム強化製品

- ビタミンD強化食品

- 骨の健康をサポート調剤

- 心臓の健康製品

- コレステロール管理食品

- オメガ3強化製品

- 心臓健康向け調剤

- タンパク質と筋肉の健康

- 高タンパク製品

- 筋肉回復処方

- スポーツ栄養統合

- 体重管理

- 低カロリー、低脂肪

- 満腹感強化製品

- 代謝サポート製剤

第7章 市場推計・予測:消費者セグメント別、2021年~2034年

- 主要動向

- 健康志向の消費者

- 食事制限セグメント

- 年齢別セグメント

- 子どもと青少年の栄養

- 成人の健康とウェルネス

- 高齢者の栄養とケア

- ライフスタイルベースのセグメント

- 忙しいプロフェッショナル

- オーガニックとナチュラル志向

- 高級品と職人技の消費者

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- Arla Foods amba

- Danone S.A.

- Dean Foods Company

- Fonterra Co-operative Group

- FrieslandCampina

- General Mills, Inc.

- Hain Celestial Group, Inc.

- Kellogg Company

- Lactalis Group

- Nestle S.A.

- Silk(Danone)

- The Kraft Heinz Company

- Unilever PLC

- WhiteWave Foods(Danone)

- Yakult Honsha Co., Ltd.

目次

The Global Dairy & Soy Food Market was valued at USD 146 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 234.4 billion by 2034. This market spans a broad range of products, including dairy items like milk, yogurt, and cheese, as well as plant-based beverages and soy alternatives. A key driver behind this growth is the increasing focus on health and wellness among consumers. There is a growing demand for nutritious products with minimal additives and more functional benefits. As lactose intolerance becomes more common, many consumers are turning to plant-based options that offer the same taste, texture, and nutritional value as traditional dairy products.

The rise of plant-based and vegan diets has sparked significant innovation in this space, with companies diversifying their portfolios to include new types of yogurt, plant-based beverages, and fortified goods aimed at vegans, flexitarians, and environmentally conscious shoppers. The aging population in developed countries is also fueling demand for fortified dairy and soy foods, particularly those enriched with proteins, vitamins, and probiotics to support bone health, digestion, and overall vitality. Meanwhile, the rapid growth of e-commerce is improving product accessibility, allowing brands to reach more consumers and offer a wider variety of products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $146 Billion |

| Forecast Value | $234.4 Billion |

| CAGR | 4.9% |

In 2024, dairy-based health foods segment held the largest share at 76% and is expected to maintain a growth rate of 5.3% through 2034. These products, which appeal to health-conscious consumers focused on gut health, immunity, and bone strength, are being developed with innovations aimed at reducing fat and sugar content while increasing accessibility for individuals with dietary restrictions.

The digestive health products segment captured a significant 34.8% share of the market in 2024, with an anticipated growth rate of 5.5% through to 2034. This impressive expansion is largely driven by an increasing consumer focus on gut health and immune system enhancement, as more individuals seek products that offer both nutritional and functional benefits. As digestive health issues become more prevalent globally, from bloating and indigestion to more complex conditions like IBS, consumers are turning to foods and supplements that promote better digestion and overall gut flora balance.

United States Dairy and Soy Food Market generated USD 25.34 billion in 2024. The country's market is expected to grow at a CAGR of 6.4% by 2034, driven by consumer trust in brands that prioritize safety, transparency in nutritional labeling, and convenient product formats. The increasing popularity of organic, gluten-free, and plant-based products has further propelled the U.S. market forward.

Leading companies in the Global Dairy and Soy Food Market include Danone S.A., Unilever PLC, Lactalis Group, Fonterra Co-operative Group, Hain Celestial Group, Inc., FrieslandCampina, General Mills, Inc., Dean Foods Company, Arla Foods amba, Silk (Danone), Nestle S.A., The Kraft Heinz Company, Yakult Honsha Co., Ltd., WhiteWave Foods (Danone), and Kellogg Company. To solidify their position in the competitive dairy and soy food sector, companies have implemented various strategies. These include continuous product reformulations to meet evolving consumer preferences, such as offering lower sugar, high-protein, and lactose-free options. Many companies have expanded their product lines to include plant-based alternatives, tapping into the growing demand for vegan and flexitarian choices. Partnerships, acquisitions, and innovation in production processes have also been key strategies to diversify portfolios and improve product accessibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product category

- 2.2.3 Health benefit

- 2.2.4 Consumer segment

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing health and wellness consciousness

- 3.2.1.2 Rising prevalence of lactose intolerance

- 3.2.1.3 Plant-based diet adoption and veganism growth

- 3.2.1.4 Protein enrichment and nutritional enhancement demands

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Traditional dairy industry competition

- 3.2.2.2 Price premium for specialty health products

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging market health awareness growth

- 3.2.3.2 Functional food and nutraceutical integration

- 3.2.3.3 Personalized nutrition and customization

- 3.2.3.4 E-commerce and direct-to-consumer growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product category

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Category, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Dairy-based health foods

- 5.2.1 Probiotic dairy products

- 5.2.2 Protein-enriched dairy

- 5.2.3 Functional dairy products

- 5.3 Soy-based food products

- 5.3.1 Traditional soy foods

- 5.3.2 Soy milk and beverages

- 5.3.3 Soy protein products

- 5.4 Combination and hybrid products

- 5.4.1 Dairy-soy blend products

- 5.4.2 Multi-protein formulations

- 5.4.3 Functional food combinations

- 5.4.4 Specialty nutritional products

Chapter 6 Market Estimates and Forecast, By Health Benefit, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Digestive health products

- 6.2.1 Probiotic and prebiotic foods

- 6.2.2 Digestive enzyme enhanced

- 6.2.3 Gut health support products

- 6.3 Bone and joint health

- 6.3.1 Calcium-enriched products

- 6.3.2 Vitamin D fortified foods

- 6.3.3 Bone health support formulations

- 6.4 Heart health products

- 6.4.1 Cholesterol management foods

- 6.4.2 Omega-3 enhanced products

- 6.4.3 Heart-healthy formulations

- 6.5 Protein and muscle health

- 6.5.1 High-protein products

- 6.5.2 Muscle recovery formulations

- 6.5.3 Sports nutrition integration

- 6.6 Weight management

- 6.6.1 Low-calorie and reduced-fat

- 6.6.2 Satiety-enhancing products

- 6.6.3 Metabolic support formulations

Chapter 7 Market Estimates and Forecast, By Consumer Segment, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Health-conscious consumers

- 7.3 Dietary restriction segments

- 7.4 Age-based segments

- 7.4.1 Children and adolescent nutrition

- 7.4.2 Adult health and wellness

- 7.4.3 Senior nutrition and care

- 7.5 Lifestyle-based segments

- 7.5.1 Busy professional

- 7.5.2 Organic and natural preference

- 7.5.3 Premium and artisanal consumers

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Arla Foods amba

- 9.2 Danone S.A.

- 9.3 Dean Foods Company

- 9.4 Fonterra Co-operative Group

- 9.5 FrieslandCampina

- 9.6 General Mills, Inc.

- 9.7 Hain Celestial Group, Inc.

- 9.8 Kellogg Company

- 9.9 Lactalis Group

- 9.10 Nestle S.A.

- 9.11 Silk (Danone)

- 9.12 The Kraft Heinz Company

- 9.13 Unilever PLC

- 9.14 WhiteWave Foods (Danone)

- 9.15 Yakult Honsha Co., Ltd.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日