|

市場調査レポート

商品コード

1797886

分子診断市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Molecular Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 分子診断市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年07月18日

発行: Global Market Insights Inc.

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

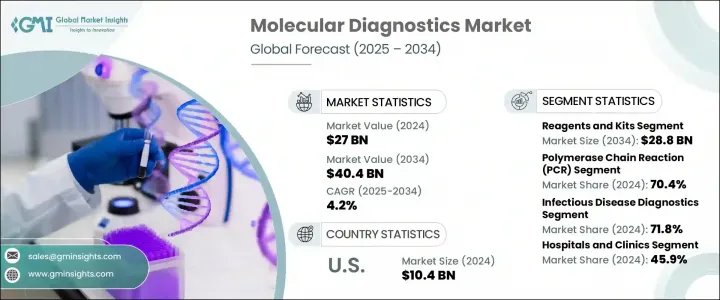

分子診断の世界市場規模は2024年に270億米ドルとなり、CAGR 4.2%で成長し、2034年には404億米ドルに達すると推定されます。

この着実な成長の背景には、感染症患者の増加、分子診断技術の継続的な革新、疾病の早期発見に対する意識の高まり、ポイントオブケア(POC)診断に対するニーズの急増、世界の高齢者人口の急速な拡大など、複数の要因が集約されています。

分子診断は、DNA、RNA、タンパク質を含むゲノムやプロテオーム中の生物学的マーカーを分析することにより、疾患の特定やモニタリングに不可欠な技術です。より迅速で正確な診断ソリューションの提供を迫られるヘルスケアシステムにおいて、この技術は現代臨床においてますます中心的な役割を果たしています。Thermo Fisher Scientific社、Hologic社、Sysmex Corporation社、Danaher Corporation社、Qiagen社など、この市場の主要企業は、進化する世界の医療ニーズに対応するため、製品ラインナップの拡充を続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 270億米ドル |

| 予測金額 | 404億米ドル |

| CAGR | 4.2% |

分子診断は、遺伝子疾患、がん、感染症など幅広い疾患の特定に不可欠な、高感度で正確な検査を含みます。この精度の高さが、先進国市場と新興国市場の双方で採用の原動力となっています。使用されている技術の中では、ポリメラーゼ連鎖反応(PCR)が2024年のシェア70.4%で市場をリードしています。RNAやDNAを正確に増幅し、微量の遺伝物質も検出できるPCRは、特に感染症スクリーニングや遺伝子検査において、早期発見に不可欠なツールとなっています。

腫瘍検査分野は2024年に21億米ドルと評価され、2034年には32億米ドルに達すると予測されています。世界中でがん罹患率が増加していることに加え、早期診断に対する需要が高まっていることが、腫瘍学における高度な分子検査ツールの導入を促進しています。ヘルスケアシステムは、高い感度と特異性を可能にする分子ベースの機器、キット、試薬に投資し、患者の転帰を改善し、がん管理プロトコルを進めています。

米国の分子診断2024年の市場規模は104億米ドル。米国とカナダの市場は、感染症の継続的な増加と次世代診断技術の開発と商業化への強力な支援により、大きな勢いを見せています。厳しい規制基準が設けられているにもかかわらず、革新的な診断機器やキットの展開が顕著に奨励されています。技術の進歩と洗練された分子検査プラットフォームの広範な採用が、北米市場のさらなる牽引役となっています。

世界の分子診断市場で事業を展開する主要企業には、F. Hoffmann-La Roche、Qiagen、Agilent Technologies、Biocartis、Thermo Fisher Scientific、Siemens Healthineers、Abbott Laboratories、QuidelOrtho Corporation、Bio-Rad Laboratories、Illumina、Becton、Dickinson and Company、Sysmex Corporation、Huwel Lifesciences、Biomerieux、Danaher Corporation、Hologicなどがあります。競争の激しい分子診断領域での地位を固めるため、各社は戦略的提携、合併、買収を積極的に進めています。また、ハイスループット、自動化、マルチプレックス検査プラットフォームを革新するための研究開発投資にも注力しています。製品ポートフォリオの拡大、規制当局の承認取得、新たな地域市場への参入は、プレーヤーが世界の足跡を拡大するのに役立っています。さらに、AIとデジタルプラットフォームの統合により、診断精度とスピードが向上し、技術的な優位性がもたらされています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 技術の進歩と世界における病気の早期診断への意識の高まり

- POC診断の需要の高まり

- 高齢人口の増加

- 研究開発イニシアチブの増加

- 感染症の発生率の上昇

- 業界の潜在的リスク&課題

- 分子診断検査の高コスト

- 熟練した人材の不足

- 市場機会

- 新興市場への拡大

- 人工知能(AI)との統合

- 促進要因

- 成長可能性分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 規制情勢

- 将来の市場動向

- 価格分析

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 機器

- 試薬とキット

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- ポリメラーゼ連鎖反応(PCR)

- 交配

- シーケンシング

- 等温核酸増幅技術(INAAT)

- マイクロアレイ

- その他の技術

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 感染症診断

- COVID-19

- インフルエンザ

- 呼吸器合胞体ウイルス(RSV)

- 結核

- CT/NG

- HIV

- C型肝炎

- B型肝炎

- その他の感染症診断

- 遺伝性疾患検査

- 腫瘍学検査

- その他の用途

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院と診療所

- 診断検査室

- その他の用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott Laboratories

- Agilent Technologies

- Becton, Dickinson, and Company

- Biocartis

- Biomerieux

- Bio-Rad Laboratories

- Danaher Corporation

- F. Hoffmann-La Roche

- Hologic

- Huwel Lifesciences

- Illumina

- Qiagen

- QuidelOrtho Corporation

- Siemens Healthineers

- Sysmex Corporation

- Thermo Fisher Scientific

The Global Molecular Diagnostics Market was valued at USD 27 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 40.4 billion by 2034. This steady growth is being fueled by multiple converging factors such as rising cases of infectious diseases, continuous innovation in molecular diagnostic technologies, growing awareness of early disease detection, the surging need for point-of-care (POC) diagnostics, and the rapid expansion of the global elderly population.

Molecular diagnostics serves as a vital technique in identifying and monitoring diseases by analyzing biological markers in the genome and proteome, including DNA, RNA, and proteins. With healthcare systems under pressure to deliver faster and more accurate diagnostic solutions, this technique is playing an increasingly central role in modern clinical practice. Major players in the market-such as Thermo Fisher Scientific, Hologic, Sysmex Corporation, Danaher Corporation, and Qiagen-continue to expand their offerings to meet evolving global health needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27 Billion |

| Forecast Value | $40.4 Billion |

| CAGR | 4.2% |

Molecular diagnostics involves highly sensitive and accurate tests that are critical for identifying a wide array of conditions, including genetic disorders, cancers, and infectious diseases. This accuracy is driving its adoption across both developed and emerging markets. Among the technologies used, polymerase chain reaction (PCR) led the market in 2024 with a 70.4% share. Its precise amplification of RNA and DNA and ability to detect even the smallest quantities of genetic material make PCR an essential tool for early detection, especially for infectious disease screening and genetic testing.

The oncology testing segment was valued at USD 2.1 billion in 2024 and is projected to reach USD 3.2 billion by 2034. Increasing cancer incidence across the globe, along with a rising demand for early diagnosis, is driving the uptake of advanced molecular testing tools in oncology. Healthcare systems are investing in molecular-based instruments, kits, and reagents that enable high sensitivity and specificity, improving patient outcomes and advancing cancer management protocols.

United States Molecular Diagnostics Market generated 10.4 billion in 2024. The U.S. and Canadian markets are witnessing significant momentum due to the continued rise of infectious diseases and strong support for the development and commercialization of next-generation diagnostic technologies. Even with strict regulatory standards in place, there is notable encouragement for the rollout of innovative diagnostic instruments and kits. Technological advancement and widespread adoption of sophisticated molecular testing platforms are helping to drive the market further in North America.

Leading companies operating in the Global Molecular Diagnostics Market include F. Hoffmann-La Roche, Qiagen, Agilent Technologies, Biocartis, Thermo Fisher Scientific, Siemens Healthineers, Abbott Laboratories, QuidelOrtho Corporation, Bio-Rad Laboratories, Illumina, Becton, Dickinson and Company, Sysmex Corporation, Huwel Lifesciences, Biomerieux, Danaher Corporation, and Hologic. To solidify their positions in the competitive molecular diagnostics space, companies are actively pursuing strategic alliances, mergers, and acquisitions. They are also focused on investing in R&D to innovate high-throughput, automated, and multiplex testing platforms. Expanding product portfolios, obtaining regulatory approvals, and entering new regional markets are helping players scale their global footprint. Additionally, integration of AI and digital platforms is enhancing diagnostic accuracy and speed, providing a technological edge.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Technology

- 2.2.3 Application

- 2.2.4 End use

- 2.2.5 Regional

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advances and increasing awareness towards early disease diagnosis globally

- 3.2.1.2 Escalating demand for POC diagnostics

- 3.2.1.3 Increasing geriatric population base

- 3.2.1.4 Increasing number of R&D initiatives

- 3.2.1.5 Rising incidences of infectious diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of molecular diagnostic tests

- 3.2.2.2 Lack of skilled personnel

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Integration with artificial intelligence (AI)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East and Africa

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.3 Reagents and kits

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Polymerase chain reaction (PCR)

- 6.3 Hybridization

- 6.4 Sequencing

- 6.5 Isothermal nucleic acid amplification technology (INAAT)

- 6.6 Microarrays

- 6.7 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Infectious disease diagnostics

- 7.2.1 COVID-19

- 7.2.2 Flu

- 7.2.3 Respiratory syncytial virus (RSV)

- 7.2.4 Tuberculosis

- 7.2.5 CT/NG

- 7.2.6 HIV

- 7.2.7 Hepatitis C

- 7.2.8 Hepatitis B

- 7.2.9 Other infectious disease diagnostics

- 7.3 Genetic disease testing

- 7.4 Oncology testing

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Diagnostic laboratories

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Agilent Technologies

- 10.3 Becton, Dickinson, and Company

- 10.4 Biocartis

- 10.5 Biomerieux

- 10.6 Bio-Rad Laboratories

- 10.7 Danaher Corporation

- 10.8 F. Hoffmann-La Roche

- 10.9 Hologic

- 10.10 Huwel Lifesciences

- 10.11 Illumina

- 10.12 Qiagen

- 10.13 QuidelOrtho Corporation

- 10.14 Siemens Healthineers

- 10.15 Sysmex Corporation

- 10.16 Thermo Fisher Scientific