アセトアミノフェン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Acetaminophen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797865

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

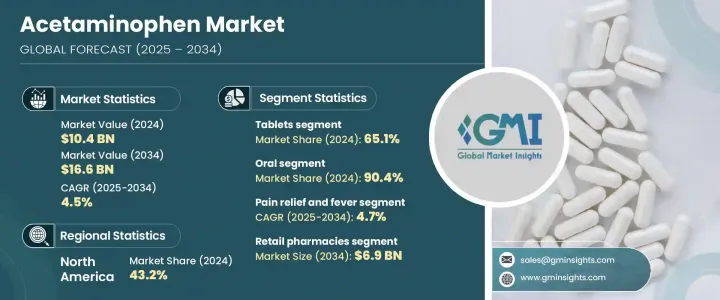

アセトアミノフェンの世界市場規模は、2024年には104億米ドルとなり、CAGR 4.5%で成長し、2034年には166億米ドルに達すると予測されています。

様々な年齢層で慢性的な疼痛状態や繰り返し起こる発熱の有病率が上昇していることが、アセトアミノフェンの世界の需要を促進しています。アセトアミノフェンは、広く入手可能で信頼性の高い市販薬として、軽度から中等度の疼痛や発熱管理に一般的に使用されています。世界の感染症や頭痛関連疾患の増加により、需要はさらに加速しています。非オピオイド鎮痛解熱薬として、アセトアミノフェンは、特に胃腸や循環器系の問題でNSAIDsに不耐性の患者にとって、第一選択の治療薬であり続けています。また、多くの地域でセルフケアや非処方薬への依存が高まっていることも、市場の成長を後押ししています。

サン・ファーマシューティカル・インダストリーズ、アボット、テバ・ファーマシューティカルズ、サノフィ、オーロビンド・ファーマなどの開発大手企業は、多様な製剤を提供し、広範なサプライチェーンを活用し、先進経済諸国と新興経済諸国の両方で強力なブランド認知度を維持することで、重要な役割を果たしています。これらの企業は生産拡張性に継続的に投資しており、様々な治療分野においてアセトアミノフェンの安定した供給を確保しています。薬事規制に関する深い専門知識により、製品承認がスムーズに行われる一方、世界な製造拠点により、供給の途絶が緩和されます。ジェネリック医薬品に注力するだけでなく、徐放性製剤、小児に適した剤形、患者のコンプライアンスを向上させる併用療法を導入することで差別化を図っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 104億米ドル |

| 予測金額 | 166億米ドル |

| CAGR | 4.5% |

2024年には、錠剤ベースの製剤セグメントが65.1%のシェアを占める。この優位性は、費用対効果、製造の容易さ、一貫した投与形式に対する消費者の嗜好によるものです。錠剤は、保存期間が長く、携帯性に優れ、特に一般用医薬品では大量生産に適しているため、広く好まれています。小売薬局やスーパーマーケットでの入手が容易な経口錠剤は、成人・小児を問わず、多くの利用者にとって依然として一般的な剤形です。都市部と農村部の両方のヘルスケア環境からの旺盛な需要は、強固な医薬品製造能力と相まって、このセグメントのリーダーシップを維持し続けています。

経口剤セグメントは2024年に90.4%のシェアを占める。カプセル剤、シロップ剤、錠剤などの経口剤は、投与が容易で体内で速やかに利用でき、自宅での治療に適しているため、依然として好まれています。これらの剤形はセルフメディケーションの動向をサポートし、専門家の監督を必要としない軽度から中等度の疼痛や発熱の治療に特に効果的です。さらに、チュアブル、徐放性製剤、小児用シロップなどの経口製剤の改良により、患者の使用感が向上し、年齢を問わず服薬アドヒアランスが向上しています。

北米のアセトアミノフェンのシェアは2024年に43.2%となりました。同地域の消費量の多さは、関節炎や慢性腰痛などの筋骨格系の疾患が広く蔓延していることと、日常的な疾患に対する非処方薬への依存度が高まっていることに関連しています。さらに、オピオイドに代わる選択肢を推進する啓蒙キャンペーンやヘルスケア政策により、アセトアミノフェンはさらに好ましい選択肢として定着しています。強固な公衆衛生インフラ、高い消費者意識、強力な医薬品プレゼンスにより、北米は引き続きこの分野の大幅な収益成長とイノベーションを牽引しています。

アセトアミノフェン市場に参入しているトップ企業には、ハイロリス・ファーマシューティカルズ、グラニュールズ・インディア・リミテッド、B.ブラウン・メルサンゲン、バイエルAG、ドクター・レディーズ・ラボラトリーズ、マリンクロット・ファーマシューティカルズ、ノバルティス、グラクソ・スミスクライン・ファーマシューティカルズ、ルパン、アルケム・ラボラトリーズ、ケンビュー(ジョンソン・エンド・ジョンソン)などがあり、サノフィやコンバージェント・テクノロジーズもその一社です。アセトアミノフェン市場における地位を強化するため、大手企業はいくつかの重要な戦略を採用しています。多くの企業は、小児用点眼薬、発泡性錠剤、配合剤など、特定の患者のニーズに合わせた幅広い製剤を導入することで、ポートフォリオの多様化に注力しています。開発途上地域での利用しやすさを向上させるため、製造の拡張性とコストの最適化が重視されています。サプライチェーンの効率化と小売販売業者との戦略的パートナーシップへの投資により、製品の入手性をさらに確実なものにしています。さらに、各社はブランド・リコールを高め、アセトアミノフェン製品を差別化するためのマーケティング・イニシアティブに継続的に取り組んでいます。進化する規制の枠組みを遵守し、製品の品質、安全性、臨床効果に投資することは、長期的な市場戦略にとって不可欠な要素です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 風邪、発熱、インフルエンザの症例が増加

- 慢性疾患と疼痛管理疾患の増加

- NSAIDsおよび麻薬と併用した静脈内パラセタモールの使用増加

- 業界の潜在的リスク&課題

- 血圧の上昇や肝毒性などのパラセタモールの副作用

- より効果的な鎮痛剤の利用可能性

- 市場機会

- 新興市場への進出

- 革新的でより安全な製剤の開発

- 促進要因

- 成長可能性分析

- 規制情勢

- 償還シナリオ

- 将来の市場動向

- ギャップ分析

- パイプライン分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:剤形別、2021年~2034年

- 主要動向

- 錠剤

- 液体懸濁液

- 輸液

- その他の剤形

第6章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 経口

- 非経口

- その他の投与経路

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 痛みの緩和と発熱

- 風邪

- 頭痛

- 腹部のけいれん

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott

- Alkem Laboratories

- Aurobindo Pharma

- B. Braun Melsungen

- Bayer AG

- Dr. Reddy's Laboratories

- GlaxoSmithKline Pharmaceuticals

- Granules India Limited

- Hyloris Pharmaceuticals

- Kenvue(Johnson &Johnson)

- Lupin

- Mallinckrodt Pharmaceuticals

- Novartis

- Sanofi

- Sun Pharmaceutical Industries

- Teva Pharmaceuticals

目次

The Global Acetaminophen Market was valued at USD 10.4 billion in 2024 and is estimated to grow at a CAGR of 4.5% to reach USD 16.6 billion by 2034. The rising prevalence of chronic pain conditions and recurring fever across various age groups continues to propel the demand for acetaminophen worldwide. As a widely accessible and trusted over-the-counter drug, acetaminophen is commonly used for mild to moderate pain and fever management. The global uptick in cases of infectious illnesses and headache-related disorders is further accelerating demand. As a non-opioid analgesic and antipyretic, acetaminophen remains a first-line treatment option, especially for patients intolerant to NSAIDs due to gastrointestinal or cardiovascular issues. The market growth is also reinforced by an increasing reliance on self-care and non-prescription medications across many regions.

Leading players such as Sun Pharmaceutical Industries, Abbott, Teva Pharmaceuticals, Sanofi, and Aurobindo Pharma play a critical role by offering a diverse range of formulations, leveraging extensive supply chains, and maintaining strong brand recognition in both developed and emerging economies. These companies continuously invest in production scalability, ensuring consistent availability of acetaminophen across various therapeutic segments. Their deep regulatory expertise allows for smoother product approvals, while global manufacturing footprints help mitigate supply disruptions. In addition to focusing on generics, they also differentiate themselves by introducing extended-release versions, pediatric-friendly formats, and combination therapies that improve patient compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.4 Billion |

| Forecast Value | $16.6 Billion |

| CAGR | 4.5% |

In 2024, the tablet-based formulations segment held a 65.1% share. This dominance is attributed to their cost-effectiveness, ease of manufacturing, and consumer preference for consistent dosage formats. Tablets are widely preferred for their longer shelf life, portability, and compatibility with large-scale production, especially for over-the-counter products. With broad accessibility in retail pharmacies and supermarkets, the oral tablet remains the go-to form for most users across adult and pediatric populations. Strong demand from both urban and rural healthcare settings, combined with robust pharmaceutical manufacturing capacities, continues to sustain the segment's leadership.

The oral route segment held a 90.4% share in 2024. Oral formulations-including capsules, syrups, and tablets-remain the preferred choice due to their ease of administration, rapid availability in the body, and suitability for at-home treatment. These formats support self-medication trends and are especially effective for treating low to moderate pain or fever without the need for professional supervision. Additionally, enhanced oral formulations such as chewables, extended-release variants, and child-friendly syrups are improving patient experience and ensuring better adherence across age groups.

North America Acetaminophen Market with a 43.2% share in 2024. The region's high consumption is linked to the widespread prevalence of musculoskeletal conditions such as arthritis and chronic back pain, coupled with an increased reliance on non-prescription medications for everyday ailments. Moreover, awareness campaigns and healthcare policies promoting alternatives to opioids have further established acetaminophen as a preferred option. With robust public health infrastructure, high consumer awareness, and strong pharmaceutical presence, North America continues to drive significant revenue growth and innovation in the sector.

Some of the top companies operating in the Acetaminophen Market include Hyloris Pharmaceuticals, Granules India Limited, B. Braun Melsungen, Bayer AG, Dr. Reddy's Laboratories, Mallinckrodt Pharmaceuticals, Novartis, GlaxoSmithKline Pharmaceuticals, Lupin, Alkem Laboratories, and Kenvue (Johnson & Johnson), alongside others like Sanofi and Convergent Technologies. To strengthen their position in the acetaminophen market, leading players are adopting several key strategies. Many companies focus on portfolio diversification by introducing a broad range of formulations tailored to specific patient needs, such as pediatric drops, effervescent tablets, and combination products. Strong emphasis is placed on manufacturing scalability and cost optimization to improve accessibility in developing regions. Investments in supply chain efficiency and strategic partnerships with retail distributors further ensure product availability. In addition, companies continue to engage in marketing initiatives to enhance brand recall and differentiate their acetaminophen products. Compliance with evolving regulatory frameworks and investment in product quality, safety, and clinical efficacy remain essential elements of their long-term market strategy.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Dosage form trends

- 2.2.3 Route of administration trends

- 2.2.4 Application trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising cases of common cold, fever, and influenza

- 3.2.1.2 Rising number of chronic diseases and pain management conditions

- 3.2.1.3 Increasing use of intravenous paracetamol in combination with NSAIDs and narcotics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects of paracetamol, such as a rise in blood pressure and hepatotoxicity

- 3.2.2.2 Availability of more effective painkillers

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets

- 3.2.3.2 Development of innovative and safer formulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Reimbursement scenario

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Pipeline analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Dosage Form, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Tablet

- 5.3 Liquid suspension

- 5.4 Infusion solution

- 5.5 Other dosage forms

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Parenteral

- 6.4 Other routes of administration

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pain relief and fever

- 7.3 Common cold

- 7.4 Headache

- 7.5 Abdominal cramps

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott

- 10.2 Alkem Laboratories

- 10.3 Aurobindo Pharma

- 10.4 B. Braun Melsungen

- 10.5 Bayer AG

- 10.6 Dr. Reddy's Laboratories

- 10.7 GlaxoSmithKline Pharmaceuticals

- 10.8 Granules India Limited

- 10.9 Hyloris Pharmaceuticals

- 10.10 Kenvue (Johnson & Johnson)

- 10.11 Lupin

- 10.12 Mallinckrodt Pharmaceuticals

- 10.13 Novartis

- 10.14 Sanofi

- 10.15 Sun Pharmaceutical Industries

- 10.16 Teva Pharmaceuticals

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日