産業用トラクションバッテリー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Industrial Traction Battery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797830

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

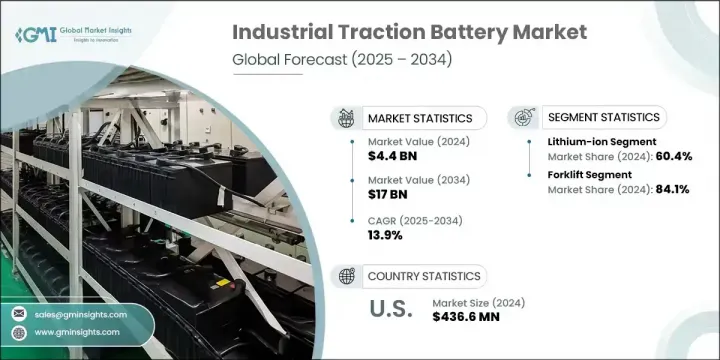

世界の産業用トラクションバッテリー市場は、2024年には44億米ドルと評価され、CAGR 13.9%で成長し、2034年には170億米ドルに達すると推定されています。

この急成長の主な要因は、近代的な産業施設内での電動マテリアルハンドリング機器、ユーティリティカート、オートメーションシステムに対する需要の高まりです。バッテリー駆動のシステムは、運用コストの低さ、排出量の削減、メンテナンスの必要性の最小化により、燃料駆動の機械に急速に取って代わりつつあります。倉庫管理、ロジスティクス、製造業務がより高い効率性と持続可能性を追求する中、トラクション・バッテリーはこのシフトを可能にする重要な役割を果たしています。自動化とロボット工学への投資の拡大は、ワークフローと安全性を向上させるバッテリー駆動の産業用資産の広範な使用を支えています。

同時に、バッテリー化学、特にリチウムイオンとキャパシタ技術の急速な進歩は、より高いエネルギー効率とより速い充電サイクルを実現しています。これらの利点により、メーカーは環境ガイドラインを遵守しながら、ダウンタイムを削減し、処理能力を向上させることができます。電気自動車への転換に財政的インセンティブと補助金を提供する政府のイニシアチブは、業界全体でクリーンエネルギー技術の採用を強化しています。トラクションバッテリー・システムは現在、稼働時間と運転回復力を最大化しながら二酸化炭素排出量の削減を目指す次世代産業エコシステムに不可欠なものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 44億米ドル |

| 予測金額 | 170億米ドル |

| CAGR | 13.9% |

リチウムイオン部門は60.4%のシェアを占め、2034年までのCAGRは15%と予測されます。この成長を後押ししているのは、倉庫業、建設業、生産業において、長期的な効率向上と排出ガス規制への準拠を求めるあまり、バッテリー駆動機器への嗜好が高まっていることです。リチウムイオンユニットは、他のバッテリータイプに比べてエネルギー密度に優れ、寿命が長く、メンテナンスが最小限であることから支持されています。急速充電技術との互換性と高負荷用途への対応能力により、連続運転に最適な選択肢となっています。

鉄道分野の2024年の市場規模は5億8,640万米ドルでした。国や地域の当局は、脱炭素化戦略の一環として、ハイブリッド鉄道や電気鉄道インフラへの投資を増やしています。都市部がよりクリーンで効率的な公共交通網を優先しているため、バッテリー駆動の地下鉄や軽便鉄道車両が目立つようになっています。鉄道のトラクション・バッテリーは、推進力をサポートするだけでなく、補助システムにも電力を供給するため、都市回廊でより静かで排出ガスのない輸送手段を可能にします。

北米の産業用トラクションバッテリーは2034年までのCAGRが10%と予想されます。スマート製造、eコマース、産業オートメーションの台頭が、電動産業車両とそれを支えるインフラの需要を押し上げています。バッテリー技術の進歩、特に充電時間の短縮とサービス間隔の延長がこの勢いを支えています。米国とカナダの企業は、規制要件と社内の持続可能性目標の両方を満たすため、低排出ガス機器への切り替えを加速させています。産業ハブは、環境に配慮した義務に沿い、エネルギー関連コストを長期的に最小化するために、バッテリー駆動の車両を統合しています。

この産業用トラクションバッテリー市場でイノベーションを推進している主要企業には、ENERSYS、BYD、Flux Power、Sunlight Group、EXIDE INDUSTRIESなどがあり、いずれも世界の競争情勢を積極的に形成しています。産業用トラクションバッテリー市場の主要企業は、先進電池技術、特にリチウムイオンと固体化学への長期的戦略投資を優先しています。これらの企業は、地域の需要に対応し、サプライチェーンの制約を軽減するために、世界な製造拠点を拡大しています。製品の多様化は彼らのアプローチの中心であり、幅広い電気産業車両に適合するモジュラー・バッテリー・システムに強く焦点を当てています。各社はまた、OEMやロジスティクス・オペレーターと協力して、性能と信頼性を向上させる統合バッテリーソリューションを共同開発しています。市場のリーダー企業数社は、リアルタイムのモニタリング、予測分析、性能最適化のためにテレマティクスとバッテリー管理システムを組み込んで、デジタルサービスを強化しています。さらに、循環型経済モデルやセカンドライフバッテリープログラムを推進することで、持続可能性目標との整合性を図っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンマッピング

- ステークホルダー分析

- 産業構造の進化

- 規制情勢

- 世界の安全基準

- 環境規制と持続可能性要件

- 地域による規制の違い

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

- 技術の進化とイノベーションの動向

- バッテリーの化学と進歩のタイムライン

- エネルギー密度向上の軌跡

- バッテリー管理システムの進化

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 戦略的ダッシュボード

- 戦略的取り組み

- 主要なパートナーシップとコラボレーション

- 主要なM&A活動

- 製品の革新と発売

- 市場拡大戦略

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:化学別、2021年~2034年

- 主要動向

- 鉛蓄電池

- リチウムイオン

- ニッケルベース

- その他

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- フォークリフト

- 鉄道

- その他

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- 韓国

- オーストラリア

- インド

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- Amara Raja Batteries

- Aliant Battery

- BYD

- Camel Group

- East Penn

- EXIDE INDUSTRIES

- ecovolta

- ENERSYS

- Farasis Energy

- Flux Power

- Guoxuan High-tech Power Energy

- HOPPECKE Batteries

- Hitachi Energy

- Mutlu Corporation

- MIDAC

- Sunlight Group

- Sunwoda Electronic

- Toshiba Corporation

目次

The Global Industrial Traction Battery Market was valued at USD 4.4 billion in 2024 and is estimated to grow at a CAGR of 13.9% to reach USD 17 billion by 2034. This surge is largely fueled by the rising demand for electric material handling equipment, utility carts, and automation systems within modern industrial facilities. Battery-powered systems are rapidly replacing fuel-driven machinery due to their lower operational costs, reduced emissions, and minimal maintenance needs. As warehousing, logistics, and manufacturing operations push for greater efficiency and sustainability, traction batteries are playing a crucial role in enabling the shift. Growing investment in automation and robotics is supporting widespread use of battery-powered industrial assets that improve workflow and safety.

At the same time, rapid progress in battery chemistry, particularly in lithium-ion and ultracapacitor technologies, is delivering greater energy efficiency and faster charge cycles. These benefits are allowing manufacturers to cut downtime and increase throughput, while still adhering to environmental guidelines. Government initiatives offering financial incentives and subsidies for electric fleet conversions are reinforcing the adoption of clean-energy technologies across industries. Traction battery systems are now integral to next-gen industrial ecosystems aiming to reduce carbon output while maximizing uptime and operational resilience.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 Billion |

| Forecast Value | $17 Billion |

| CAGR | 13.9% |

The lithium-ion segment held a 60.4% share and is projected to grow at a CAGR of 15% through 2034. This growth is being propelled by a growing preference for battery-powered equipment in warehousing, construction, and production, as organizations seek long-term efficiency gains and compliance with emissions regulations. Lithium-ion units are favored for their superior energy density, longer life span, and minimal maintenance compared to other battery types. Their compatibility with fast-charging technologies and ability to support high-duty applications make them a prime choice for continuous operation.

The rail segment was valued at USD 586.4 million in 2024. National and regional authorities are increasing investments in hybrid and electric rail infrastructure as part of decarbonization strategies. Battery-powered metro and light rail vehicles are becoming more prominent as urban areas prioritize cleaner, more efficient public transport networks. Traction batteries in rail not only support propulsion but also power auxiliary systems, enabling quieter, emission-free transit options in urban corridors.

North America Industrial Traction Battery Market is expected to register a CAGR of 10% through 2034. The rise of smart manufacturing, e-commerce, and industrial automation is pushing demand for electric industrial vehicles and supporting infrastructure. Advancements in battery technologies, particularly those that reduce charging time and extend service intervals, are supporting this momentum. Businesses across the U.S. and Canada are increasingly switching to low-emission equipment to meet both regulatory requirements and internal sustainability goals. Industrial hubs are integrating battery-powered fleets to align with green mandates and minimize energy-related costs over time.

Top players driving innovation in this Industrial Traction Battery Market include ENERSYS, BYD, Flux Power, Sunlight Group, and EXIDE INDUSTRIES, all of which are actively shaping the global competitive landscape. Leading companies in the industrial traction battery market are prioritizing long-term strategic investments in advanced battery technologies, particularly lithium-ion and solid-state chemistries. These players are expanding their global manufacturing footprints to address regional demand and reduce supply chain constraints. Product diversification is central to their approach, with a strong focus on modular battery systems compatible with a wide range of electric industrial vehicles. Companies are also collaborating with OEMs and logistics operators to co-develop integrated battery solutions that enhance performance and reliability. Several market leaders are enhancing their digital offerings by embedding telematics and battery management systems for real-time monitoring, predictive analytics, and performance optimization. Additionally, they are aligning with sustainability targets by promoting circular economy models and second-life battery programs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1.1 Value chain mapping

- 3.1.1.2 Stakeholder analysis

- 3.1.1.3 Industry structure evolution

- 3.2 Regulatory landscape

- 3.2.1.1 Global safety standards

- 3.2.1.2 Environmental regulations and sustainability requirements

- 3.2.1.3 Regional regulatory variations

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Technology evolution and innovation trends

- 3.7.1 Battery chemistry and advancement timeline

- 3.7.2 Energy density improvement trajectory

- 3.7.3 Battery management system evolution

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Chemistry, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Lead acid

- 5.3 Lithium-ion

- 5.4 Nickel-based

- 5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Forklift

- 6.3 Railroads

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 Australia

- 7.4.5 India

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Amara Raja Batteries

- 8.2 Aliant Battery

- 8.3 BYD

- 8.4 Camel Group

- 8.5 East Penn

- 8.6 EXIDE INDUSTRIES

- 8.7 ecovolta

- 8.8 ENERSYS

- 8.9 Farasis Energy

- 8.10 Flux Power

- 8.11 Guoxuan High-tech Power Energy

- 8.12 HOPPECKE Batteries

- 8.13 Hitachi Energy

- 8.14 Mutlu Corporation

- 8.15 MIDAC

- 8.16 Sunlight Group

- 8.17 Sunwoda Electronic

- 8.18 Toshiba Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日