|

市場調査レポート

商品コード

1797764

軌道上輸送機の市場機会、成長促進要因、産業動向分析、2025~2034年予測Orbital Transfer Vehicle (OTV) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 軌道上輸送機の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年07月28日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

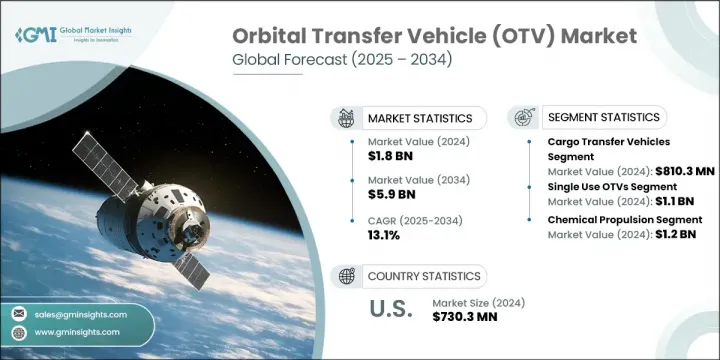

軌道上輸送機の世界市場は、2024年には18億米ドルと評価され、CAGR13.1%で成長し、2034年には59億米ドルに達すると予測されています。

市場成長の原動力となっているのは、適応性の高い衛星展開方法に対するニーズの高まり、小型衛星やキューブサットの打ち上げ頻度の上昇、推進システムの急速な進歩、軌道インフラへの資本流入の急増、商業宇宙構想の着実な増加などです。産業が従来型打ち上げシステムから移行するにつれて、OTVは、地球低軌道(LEO)、地球中軌道(MEO)、静止軌道(GEO)、さらにその先の太陽系宇宙空間など、さまざまな軌道上の目的地にペイロードを運ぶことができる、不可欠な宇宙送達ソリューションとして台頭しつつあります。官民ともに、衛星コンステレーション、宇宙サービスモジュール、軌道ハビタット、月面支援構造物の開発に多額の投資を行っており、市場の長期的成長をさらに後押ししています。

柔軟な衛星輸送に対する需要の高まりは、OTVセグメントの拡大を後押しする重要な要因です。事業者は現在、硬直した事前定義された打ち上げプロファイルに縛られるのではなく、より高い応答性とミッションに応じた軌道配置を提供する展開システムを求めています。軌道上輸送機は、宇宙ロジスティクスソリューションとして、多様な軌道環境でのオンデマンド衛星輸送を可能にすることで、旧来のシステムに取って代わりつつあります。これと並行して、国防部門から民間航空宇宙新興企業まで、宇宙を専門とするさまざまな事業体が、より強固な軌道生態系を構築するための取り組みを強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 18億米ドル |

| 予測金額 | 59億米ドル |

| CAGR | 13.1% |

貨物輸送機セグメントは、2024年に8億1,030万米ドルを生み出しました。このセグメントは、軌道ステーションを維持し、新たな商業プラットフォームへの道を開くために設計されたペイロード再供給ミッションの頻度の増加から引き続き利益を得ています。衛星の整備や軌道上の資産保守が重視されるようになったことで、ミッションクリティカルなハードウェアのタイムリーで安全な輸送を保証する専用の貨物輸送機に対する需要も加速しています。自律型ドッキングシステムの開発と航空宇宙組織間の世界の協力関係の拡大が、再利用型貨物輸送技術の採用を促進しています。

シングルユース軌道輸送機セグメントは、2024年に11億米ドルを生み出しました。これらの輸送機は、構造が単純化され、製造コストが削減され、1回限りのペイロード配備を伴うミッションに適しているため、ますます好まれています。複雑な回収システムや再利用システムを必要としないため、車両回収が現実的でない高リスクまたは長距離のミッションに理想的なソリューションを記載しています。その利用は、戦略的デリバリーの信頼性が最重要視される政府機関や防衛関連のミッションで特に広まっています。さらに、新興企業や航空宇宙産業への新規参入企業は、検査、プロトタイプの検証、経済的に実行可能な軌道実証実験の初期段階において、シングルユースプラットフォームを選択することが多いです。

米国の軌道上輸送機(OTV)市場は、2024年に7億3,030万米ドルを創出しました。この強力な地位は、衛星打上げ能力の強化、軌道上保守システムの開発、軌道上デブリ軽減戦略の実施など、政府機関と民間事業者の双方による持続的な努力に支えられています。こうした共同投資は、軌道運用の効率を高め、ペイロードの操作性を向上させ、宇宙資産の耐用年数を延ばすことを目的としています。軌道の持続可能性とミッションの柔軟性がますます重視されるようになり、このセグメントでの日本のリーダーシップは強化され続けています。

世界の軌道上輸送機(OTV)市場を積極的に形成している著名な企業には、Astroscale Holdings Inc.、Virgin Galactic、D-Orbit S.p.A.、Relativity Space、OHB SE、Quantum Space LLC、Northrop Grumman Corporation、ArianeGroup SAS、Space Machines Company Pty Ltd、Sierra Space、Moog Inc.、ISRO/Antrix Corporation、China Academy of Launch Vehicle Technology(CALT)、SpaceX、MaiaSpace SAS、Mitsubishi Heavy Industries、Altius Space Machines Inc、Impulse Space Inc.、Roscosmos / Energia、Firefly Aerospace、Atomos Space LLC、Gama Space SAS、Rocket Lab USA Inc.、Blue Origin LLC、Epic Aerospace LLC、Thales Alenia Space S.A.、United Launch Alliance LLC (ULA)、Orbital Operations Ltd、CASIC / ExPace、Momentus Inc.、Starfish Space Inc.があります。軌道上輸送機市場の主要企業は、競合を強化するために技術革新とパートナーシップを優先しています。その多くは、柔軟なミッション構成をサポートするため、独自の推進システムとモジュール型ビークル設計に投資しています。越境戦略的協力関係や組織間の協力関係は、企業がより広範な打ち上げプラットフォームにアクセスし、自社のロケットを多様なミッション・アーキテクチャに統合するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- エコシステム分析

- 産業への影響要因

- 促進要因

- 衛星展開の柔軟性に対する需要の高まり

- 小型衛星とキューブサットの打ち上げ増加

- 推進技術の進歩

- 宇宙インフラへの投資増加

- 商業宇宙活動の拡大

- 落とし穴と課題

- 技術的信頼性とミッション保証

- 規制の複雑さと宇宙交通管理

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 新たなビジネスモデル

- コンプライアンス要件

- 国防予算分析

- 世界の防衛費の動向

- 地域防衛予算配分

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

- 主要な防衛近代化プログラム

- 予算予測(2025~2034)

- 産業の成長への影響

- 国別防衛予算

- 持続可能性への取り組み

- サプライチェーンのレジリエンス

- 地政学的分析

- 人材分析

- デジタル変革

- 合併、買収、戦略的提携の情勢

- リスク評価と管理

- 主要契約の締結(2021~2024年)

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 市場集中分析

- 地域別

- 主要参入企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- 技術

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域による市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- 課題者

- フォロワー

- ニッチ参入企業

- 戦略的展望マトリックス

- 財務実績の比較

- 主要開発、2021~2024年

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推定・予測:タイプ別、2021~2034年

- 主要動向

- 貨物輸送機

- 乗組員輸送機

- 燃料補給機

- 衛星整備・デブリ除去機

- その他

第6章 市場推定・予測:車種別、2021~2034年

- 主要動向

- 使い捨てOTV

- 再利用型OTV

第7章 市場推定・予測:推進システム別、2021~2034年

- 主要動向

- 化学推進

- 電気推進

- 核熱推進

- その他

第8章 市場推定・予測:積載量別、2021~2034年

- 主要動向

- 小型(最大200kg)

- 中型(200kg~1,000kg)

- 大型(1,000kg以上)

第9章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 衛星展開

- 宇宙探査

- 軌道上サービス

- 宇宙旅行

- 宇宙ステーションの補給と乗組員の交代

- その他

第10章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 政府の宇宙機関

- 商業宇宙企業

- 官民パートナーシップ

第11章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第12章 企業プロファイル

- 世界的主要企業

- 地域主要企業

- 破壊的イノベーション/ニッチ参入企業

- Starfish Space Inc.

- Atomos Space LLC

- Astroscale Holdings Inc.

- Virgin Galactic

The Global Orbital Transfer Vehicle Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 13.1% to reach USD 5.9 billion by 2034. The market growth is driven by an increasing need for adaptable satellite deployment methods, the rising frequency of small satellite and CubeSat launches, rapid progress in propulsion systems, surging capital flow into orbital infrastructure, and a steady uptick in commercial space initiatives. As the industry shifts away from traditional launch systems, OTVs are emerging as indispensable in-space delivery solutions capable of maneuvering payloads to various orbital destinations-including low Earth orbit (LEO), medium Earth orbit (MEO), geostationary orbit (GEO), and beyond to cislunar space. Both public and private sectors are channeling considerable investments into developing satellite constellations, in-space service modules, orbital habitats, and lunar support structures-further fueling long-term growth in the market.

Heightened demand for flexible satellite transportation is a critical factor powering the expansion of the OTV space. Operators now seek deployment systems that offer greater responsiveness and mission-specific orbital placement, rather than being tied to rigid, predefined launch profiles. Orbital transfer vehicles, acting as in-space logistics solutions, are replacing older systems by enabling on-demand satellite delivery across a diverse range of orbital environments. In tandem, various space-focused entities-from national defense divisions to commercial aerospace startups-are ramping up efforts to construct more robust orbital ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 13.1% |

The cargo transfer vehicles segment generated USD 810.3 million in 2024. This segment continues to benefit from the growing frequency of payload resupply missions designed to sustain orbital stations and pave the way for emerging commercial platforms. The growing emphasis on satellite servicing and orbital asset maintenance is also accelerating demand for dedicated cargo vehicles that ensure the timely, secure transport of mission-critical hardware. Developments in autonomous docking systems and expanding global cooperation between aerospace organizations are driving the adoption of reusable cargo transport technologies.

The single-use orbital transfer vehicles segment generated USD 1.1 billion in 2024. These vehicles are increasingly favored due to their simplified structure, reduced manufacturing costs, and suitability for missions involving one-time payload deployments. By eliminating the need for complex retrieval or reuse systems, they provide an ideal solution for high-risk or long-distance missions where vehicle recovery is impractical. Their utilization is particularly prevalent among government bodies and defense-related missions, where strategic delivery reliability is paramount. Additionally, startups and newer entrants to the aerospace industry often opt for single-use platforms during initial stages of testing, prototype validation, or conducting economically viable orbital demonstrations.

United States Orbital Transfer Vehicle (OTV) Market generated USD 730.3 million in 2024. This strong position is underpinned by sustained efforts from both governmental institutions and commercial operators to enhance satellite launch capabilities, develop in-orbit maintenance systems, and implement orbital debris mitigation strategies. These collaborative investments aim to enhance the efficiency of orbital operations, increase payload maneuverability, and extend the useful life of space assets. The growing emphasis on orbital sustainability and mission flexibility continues to strengthen the country's leadership in the sector.

Prominent players actively shaping the Global Orbital Transfer Vehicle (OTV) Market include Astroscale Holdings Inc., Virgin Galactic, D-Orbit S.p.A., Relativity Space, OHB SE, Quantum Space LLC, Northrop Grumman Corporation, ArianeGroup SAS, Space Machines Company Pty Ltd, Sierra Space, Moog Inc., ISRO / Antrix Corporation, China Academy of Launch Vehicle Technology (CALT), SpaceX, MaiaSpace SAS, Mitsubishi Heavy Industries, Altius Space Machines Inc., Impulse Space Inc., Roscosmos / Energia, Firefly Aerospace, Atomos Space LLC, Gama Space SAS, Rocket Lab USA Inc., Blue Origin LLC, Epic Aerospace LLC, Thales Alenia Space S.A., United Launch Alliance LLC (ULA), Orbital Operations Ltd, CASIC / ExPace, Momentus Inc., and Starfish Space Inc. Leading companies in the orbital transfer vehicle market are prioritizing innovation and partnerships to solidify their competitive edge. Many are investing in proprietary propulsion systems and modular vehicle designs to support flexible mission configurations. Strategic collaborations-both cross-border and inter-organizational-are helping firms access broader launch platforms and integrate their vehicles into diverse mission architectures.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Vehicle type trends

- 2.2.3 Propulsion system trends

- 2.2.4 Payload capacity trends

- 2.2.5 Application trends

- 2.2.6 End use trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry ecosystem analysis

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing demand for satellite deployment flexibility

- 3.3.1.2 Rising small satellite and cubesat launches

- 3.3.1.3 Advancements in propulsion technologies

- 3.3.1.4 Increased investments in space infrastructure

- 3.3.1.5 The growing commercial space activities

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 Technical Reliability and Mission Assurance

- 3.3.2.2 Regulatory Complexity and Space Traffic Management

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Emerging business models

- 3.10 Compliance requirements

- 3.11 Defense budget analysis

- 3.12 Global defense spending trends

- 3.13 Regional defense budget allocation

- 3.13.1 North America

- 3.13.2 Europe

- 3.13.3 Asia Pacific

- 3.13.4 Middle East and Africa

- 3.13.5 Latin America

- 3.14 Key defense modernization programs

- 3.15 Budget forecast (2025-2034)

- 3.15.1 Impact on industry growth

- 3.15.2 Defense budgets by country

- 3.16 Sustainability initiatives

- 3.17 Supply chain resilience

- 3.18 Geopolitical analysis

- 3.19 Workforce analysis

- 3.20 Digital transformation

- 3.21 Mergers, acquisitions, and strategic partnerships landscape

- 3.22 Risk assessment and management

- 3.23 Major contract awards (2021-2024)

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market estimates and forecast, By Type, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Cargo transfer vehicles

- 5.3 Crew transfer vehicles

- 5.4 Refueling vehicles

- 5.5 Satellite servicing & debris removal vehicles

- 5.6 Others

Chapter 6 Market estimates and forecast, By Vehicle Type, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Single Use OTVs

- 6.3 Reusable OTVs

Chapter 7 Market estimates and forecast, By Propulsion System, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Chemical propulsion

- 7.3 Electric propulsion

- 7.4 Nuclear thermal propulsion

- 7.5 Others

Chapter 8 Market estimates and forecast, By Payload Capacity, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Small payload (up to 200 kg)

- 8.3 Medium payload (200 kg to 1,000 kg)

- 8.4 Large payload (1,000 kg and above)

Chapter 9 Market estimates and forecast, By Application, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 Satellite deployment

- 9.3 Space exploration

- 9.4 Inorbit servicing

- 9.5 Space tourism

- 9.6 Space station resupply & crew rotation

- 9.7 Others

Chapter 10 Market estimates and forecast, By End Use, 2021 - 2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 Government space agencies

- 10.3 Commercial space companies

- 10.4 Public-private partnerships

Chapter 11 Market estimates and forecast, By Region, 2021 - 2034 (USD Million & Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company profiles

- 12.1 Global Key Players

- 12.1.1 SpaceX

- 12.1.2 Blue Origin LLC

- 12.1.3 Northrop Grumman Corporation

- 12.1.4 Thales Alenia Space S.A.

- 12.1.5 ArianeGroup SAS

- 12.1.6 United Launch Alliance LLC (ULA)

- 12.1.7 Mitsubishi Heavy Industries

- 12.1.8 China Academy of Launch Vehicle Technology (CALT)

- 12.1.9 Roscosmos / Energia

- 12.1.10 ISRO / Antrix Corporation

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 Rocket Lab USA Inc.

- 12.2.1.2 Momentus Inc.

- 12.2.1.3 Epic Aerospace LLC

- 12.2.1.4 Quantum Space LLC

- 12.2.1.5 Impulse Space Inc.

- 12.2.1.6 Firefly Aerospace

- 12.2.1.7 Relativity Space

- 12.2.1.8 Sierra Space

- 12.2.1.9 Moog Inc.

- 12.2.1.10 Altius Space Machines Inc.

- 12.2.2 Europe

- 12.2.2.1 D-Orbit S.p.A.

- 12.2.2.2 OHB SE

- 12.2.2.3 Orbital Operations Ltd

- 12.2.2.4 Gama Space SAS

- 12.2.2.5 MaiaSpace SAS

- 12.2.3 Asia-Pacific

- 12.2.3.1 CASIC / ExPace

- 12.2.3.2 Space Machines Company Pty Ltd

- 12.2.1 North America

- 12.3 Disruptors / Niche Players

- 12.3.1 Starfish Space Inc.

- 12.3.2 Atomos Space LLC

- 12.3.3 Astroscale Holdings Inc.

- 12.3.4 Virgin Galactic