衛星ベース地球観測市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)

Satellite-Based Earth Observation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797753

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

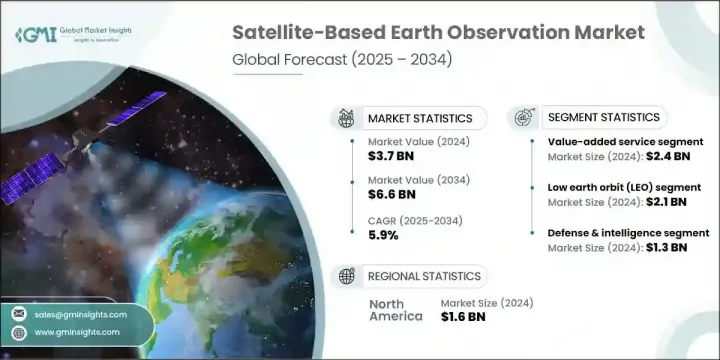

世界の衛星ベース地球観測市場は、2024年には37億米ドルと評価され、CAGR 5.9%で成長し、2034年には66億米ドルに達すると予測されています。

気候監視、国家安全保障、環境用途における地理空間情報への依存の高まりが、一貫した需要を牽引しています。衛星の小型化と配備コストの低減の進歩は、小型衛星の配備を大幅に後押ししています。こうした小型プラットフォームは、農業、防衛、災害対応など、さまざまな分野にコスト効率の高い高解像度データを提供します。人工知能とクラウド・コンピューティングは、生の衛星画像を実用的なデータに変換する上で極めて重要な役割を果たし、それによって産業界や政府機関の意思決定を強化しています。また、気候パターンの監視、都市成長の最適化、自然災害への耐性の向上を目指した世界の取り組みにより、需要も高まっています。

精度の向上、データ配信サイクルの短縮、洗練された分析プラットフォームへの容易なアクセスが市場を後押しし続け、地表の状況をほぼリアルタイムで把握できるようになっています。こうした改善により、データ収集から実用的な意思決定までの時間が大幅に短縮され、農業、環境保全、都市計画、緊急管理などの分野の利害関係者がより効果的に対応できるようになっています。衛星データをAIや機械学習と統合することで、微妙な環境変化を検知し、インフラを監視し、作物の健康状態を評価し、森林伐採や汚染をかつてない精度で追跡する能力がさらに高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 37億米ドル |

| 市場規模予測 | 66億米ドル |

| CAGR | 5.9% |

付加価値サービス分野は、2024年に24億米ドルを生み出しました。この成長は、衛星データから得られるカスタマイズされた分析に対する要求の高まりと結びついています。これらの洞察は、インフラ、エネルギー、スマートシティ、農業などの主要部門で、よりスマートな計画と運用をサポートします。AIを搭載したプラットフォームの開発と分析プロバイダーとの提携により、環境追跡や都市開発などの分野でより具体的なソリューションが可能になります。統一されたプラットフォームを通じてアナリティクスへのアクセスが簡素化されることで、特に高速で直感的、かつ信頼性の高い情報提供システムを求めるユーザーの間で導入が進みます。

低軌道(LEO)セグメントは2024年に21億米ドルと評価されました。小型衛星やコンパクトなCubeSatsの台頭は、これらのプラットフォームが高解像度のビジュアルと迅速な再訪問間隔を提供することから、この成長に寄与しています。頻繁な撮像は、土地利用マッピング、農作物の健康追跡、緊急対応などのアプリケーションをサポートします。打ち上げプロバイダーと衛星会社の協力により、アクセスが改善され、運用コストが削減されました。このような利点により、特に防衛、持続可能性、環境モニタリングの各分野において、詳細で常時観測可能な地球観測に対する商業的・社会的関心の拡大が加速しています。

米国の衛星ベース地球観測2024年の市場規模は13億8,000万米ドル。このリーダーシップは、衛星技術革新と国家安全保障技術への大規模投資に起因します。企業は、災害への備え、気候データの収集、戦略的監視など、進化するニーズに合わせて製品を提供する必要があります。AIを活用したデータ分析、クラウドベースの提供モデル、安全な通信システムの統合を重視することで、将来の政府契約や競合との契約において競争力を維持しようとするベンダーのポジショニングはさらに強化されます。

世界の衛星ベース地球観測市場の主要参入企業には、Planet Labs PBC、MinoSpace、GeoOptics Inc.、ICEYE Oy、Capella Space Inc.、OroraTech GmbH、Airbus Defence and Space、Spire Global, Inc.、ImageSat International N.V.、Maxar Technologies Inc.、BlackSky Technology Inc.、LiveEO GmbH、L3Harris Technologies Inc.、China Siwei Surveying and Mapping Technology Co.衛星ベース地球観測市場におけるプレゼンスを強化するため、各社はよりインテリジェントなデータ解釈のためのAIや機械学習アルゴリズムの統合に注力しています。多くの企業が分析会社とパートナーシップを結び、防衛、農業、環境モニタリングなど特定の業界に合わせたカスタマイズサービスを共同開発しています。小型衛星のコンステレーションを拡大することで、より広いカバー範囲とより頻繁なデータ収集が可能になります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- エコシステム分析

- 業界への影響要因

- 促進要因

- 地理空間データに対する需要の増加

- 気候変動監視

- 政府および防衛アプリケーション

- クラウドコンピューティングとAI分析の普及

- 衛星の小型化の進歩

- 落とし穴と課題

- 高額な初期投資と立ち上げコスト

- 軌道上のデブリと宇宙の混雑

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 新たなビジネスモデル

- コンプライアンス要件

- 国防予算分析

- 世界の防衛費の動向

- 地域防衛予算配分

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

- 主要な防衛近代化プログラム

- 予算予測(2025-2034)

- 業界の成長への影響

- 国別防衛予算

- サプライチェーンのレジリエンス

- 地政学的分析

- 人材分析

- デジタル変革

- 合併、買収、戦略的提携の情勢

- リスク評価と管理

- 主要契約の締結(2021~2024年)

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 市場集中分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な動向(2021~2024年)

- 企業合併・買収 (M&A)

- 事業提携・協力

- 技術進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:製品種類別(2021~2034年)

- 主要動向

- EOデータ

- 光学画像データ

- レーダー画像データ

- ハイパースペクトル画像データ

- 熱赤外線画像データ

- その他

- 付加価値サービス

- 分析および洞察サービス

- 地理空間インテリジェンスプラットフォーム

- その他

第6章 市場推計・予測:衛星軌道別(2021~2034年)

- 主要動向

- 低軌道(LEO)

- 中軌道(MEO)

- 静止軌道(GEO)

第7章 市場推計・予測:技術別(2021~2034年)

- 主要動向

- 光学式(電気光学式)

- 合成開口レーダー(SAR)

- ハイパースペクトル・マルチスペクトル

- 熱赤外線センサー

- LiDARシステム

- その他

第8章 市場推計・予測:用途別(2021~2034年)

- 主要動向

- 農業・林業

- 防衛・諜報

- 環境・気候監視

- 都市・インフラ計画

- エネルギー・鉱業・天然資源

- 海運・輸送

- その他

第9章 市場推計・予測:最終用途別(2021~2034年)

- 主要動向

- 政府・防衛

- 軍隊・諜報機関

- 民間政府・公安部門

- 商業用

- 農業・林業企業

- 環境サービスプロバイダー

- 建設・都市計画会社

- エネルギー・鉱業会社

- 海運事業者

- その他

- 研究・学術

- その他

第10章 市場推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- 世界の主要企業

- Maxar Technologies Inc.

- Airbus Defence and Space

- Planet Labs PBC

- ImageSat International N.V.

- Spire Global Inc

- 各地域の主要企業

- 北米

- BlackSky Technology Inc.

- L3Harris Technologies Inc

- MDA Space Ltd.

- 欧州

- LiveEO GmbH

- Satellite Vu Ltd.

- ICEYE Oy

- アジア太平洋地域

- SpaceWill Information Co., Ltd.

- MinoSpace

- XRTech Group

- China Siwei Surveying and Mapping Technology Co., Ltd.

- 北米

- ディスラプター/ニッチプレーヤー

- Capella Space Inc.

- Pixxel Inc

- OroraTech GmbH

- UrtheCast Corp.

- GeoOptics Inc.

目次

The Global Satellite-Based Earth Observation Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 6.6 billion by 2034. Increasing reliance on geospatial intelligence for climate surveillance, national security, and environmental applications is driving consistent demand. Advancements in satellite miniaturization and lower deployment costs have significantly boosted the deployment of smaller satellites. These compact platforms deliver cost-effective, high-resolution data across several sectors, including agriculture, defense, and disaster response. Artificial intelligence and cloud computing play a pivotal role in transforming raw satellite imagery into actionable data, thereby enhancing decision-making for industries and governments alike. Demand is also rising due to global efforts aimed at monitoring climate patterns, optimizing urban growth, and improving resilience to natural disasters.

Enhanced accuracy, shorter data delivery cycles, and easy access to sophisticated analytics platforms continue to push the market forward, enabling near real-time insights into Earth's surface conditions. These improvements are drastically reducing the time between data collection and actionable decision-making, allowing stakeholders in sectors such as agriculture, environmental conservation, urban planning, and emergency management to respond more effectively. The integration of satellite data with AI and machine learning has further amplified the ability to detect subtle environmental changes, monitor infrastructure, assess crop health, and track deforestation or pollution with unprecedented precision.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 billion |

| Forecast Value | $6.6 billion |

| CAGR | 5.9% |

The value-added services segment generated USD 2.4 billion in 2024. This growth is tied to the increasing requirement for customized analysis derived from satellite data. These insights support smarter planning and operations in key sectors such as infrastructure, energy, smart cities, and agriculture. Integration of AI-powered platforms and partnerships with analytics providers allows for more specific solutions in areas like environmental tracking and city development. Simplified access to analytics through unified platforms increases adoption, especially among users seeking fast, intuitive, and reliable information delivery systems.

The low Earth orbit (LEO) segment was valued at USD 2.1 billion in 2024. The rise of small satellites and compact CubeSats contributes to this growth, as these platforms deliver high-resolution visuals and rapid revisit intervals. Frequent imaging supports applications such as land use mapping, crop health tracking, and emergency response. Collaboration between launch providers and satellite firms has improved access and reduced operational costs. These advantages have accelerated the expansion of commercial and public interest in detailed, constant Earth observation, especially across defense, sustainability, and environmental monitoring initiatives.

United States Satellite-Based Earth Observation Market generated USD 1.38 billion in 2024. This leadership stems from large-scale investment in satellite innovation and national security technologies. Companies must align their product offerings with evolving needs in disaster readiness, climate data gathering, and strategic surveillance. Emphasis on integrating AI-driven data analysis, cloud-based delivery models, and secure communications systems will further enhance the positioning of vendors seeking to remain competitive in future government contracts and commercial engagements.

Key participants in the Global Satellite-Based Earth Observation Market include Planet Labs PBC, MinoSpace, GeoOptics Inc., ICEYE Oy, Capella Space Inc., OroraTech GmbH, Airbus Defence and Space, Spire Global, Inc., ImageSat International N.V., Maxar Technologies Inc., BlackSky Technology Inc., LiveEO GmbH, L3Harris Technologies Inc., China Siwei Surveying and Mapping Technology Co., Ltd., and MDA Space Ltd. To strengthen their presence in the satellite-based Earth observation market, companies are focusing on integrating AI and machine learning algorithms for more intelligent data interpretation. Many are forming partnerships with analytics firms to co-develop customized services tailored to specific industries like defense, agriculture, and environmental monitoring. Expanding constellations of smaller satellites enables broader coverage and more frequent data collection.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Satellite orbit trends

- 2.2.3 Technology trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry ecosystem analysis

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing demand for geospatial data

- 3.3.1.2 Climate change monitoring

- 3.3.1.3 Government and defense applications

- 3.3.1.4 Proliferation of cloud computing and AI analytics

- 3.3.1.5 Advancements in satellite miniaturization

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 High Initial Investment and Launch Costs

- 3.3.2.2 Orbital Debris and Space Congestion

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Emerging business models

- 3.10 Compliance requirements

- 3.11 Defense budget analysis

- 3.12 Global defense spending trends

- 3.13 Regional defense budget allocation

- 3.13.1 North America

- 3.13.2 Europe

- 3.13.3 Asia Pacific

- 3.13.4 Middle East and Africa

- 3.13.5 Latin America

- 3.14 Key defense modernization programs

- 3.15 Budget forecast (2025-2034)

- 3.15.1 Impact on industry growth

- 3.15.2 Defense budgets by country

- 3.16 Supply chain resilience

- 3.17 Geopolitical analysis

- 3.18 Workforce analysis

- 3.19 Digital transformation

- 3.20 Mergers, acquisitions, and strategic partnerships landscape

- 3.21 Risk assessment and management

- 3.22 Major contract awards (2021-2024)

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market estimates and forecast, By Product Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 EO Data

- 5.2.1 Optical imaging data

- 5.2.2 Radar imaging data

- 5.2.3 Hyperspectral imaging data

- 5.2.4 Thermal infrared imaging data

- 5.2.5 Others

- 5.3 Value-added services

- 5.3.1 Analytics & Insight Services

- 5.3.2 Geospatial Intelligence Platforms

- 5.3.3 Others

Chapter 6 Market estimates and forecast, By Satellite Orbit, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Low earth orbit (LEO)

- 6.3 Medium earth orbit (MEO)

- 6.4 Geostationary orbit (GEO)

Chapter 7 Market estimates and forecast, By Technology, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Optical (electro-optical)

- 7.3 Synthetic aperture radar (SAR)

- 7.4 Hyperspectral & multispectral

- 7.5 Thermal infrared sensors

- 7.6 LiDAR systems

- 7.7 Others

Chapter 8 Market estimates and forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Agriculture & forestry

- 8.3 Defense & intelligence

- 8.4 Environmental & climate monitoring

- 8.5 Urban & infrastructure planning

- 8.6 Energy, mining & natural resources

- 8.7 Maritime & transportation

- 8.8 Others

Chapter 9 Market estimates and forecast, By End Use, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 Government & defense

- 9.2.1 Military & intelligence agencies

- 9.2.2 Civil government & public safety departments

- 9.3 Commercial

- 9.3.1 Agribusiness & forestry companies

- 9.3.2 Environmental service providers

- 9.3.3 Construction & urban planning firms

- 9.3.4 Energy & mining companies

- 9.3.5 Maritime logistics operators

- 9.3.6 Others

- 9.4 Research & academia

- 9.5 Others

Chapter 10 Market estimates and forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company profiles

- 11.1 Global Key Players

- 11.1.1 Maxar Technologies Inc.

- 11.1.2 Airbus Defence and Space

- 11.1.3 Planet Labs PBC

- 11.1.4 ImageSat International N.V.

- 11.1.5 Spire Global Inc

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 BlackSky Technology Inc.

- 11.2.1.2 L3Harris Technologies Inc

- 11.2.1.3 MDA Space Ltd.

- 11.2.2 Europe

- 11.2.2.1 LiveEO GmbH

- 11.2.2.2 Satellite Vu Ltd.

- 11.2.2.3 ICEYE Oy

- 11.2.3 Asia-Pacific

- 11.2.3.1 SpaceWill Information Co., Ltd.

- 11.2.3.2 MinoSpace

- 11.2.3.3 XRTech Group

- 11.2.3.4 China Siwei Surveying and Mapping Technology Co., Ltd.

- 11.2.1 North America

- 11.3 Disruptors / Niche Players

- 11.3.1 Capella Space Inc.

- 11.3.2 Pixxel Inc

- 11.3.3 OroraTech GmbH

- 11.3.4 UrtheCast Corp.

- 11.3.5 GeoOptics Inc.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日