電池バインダー材料の市場機会と促進要因、産業動向分析、2025年~2034年予測

Battery Binder Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797749

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

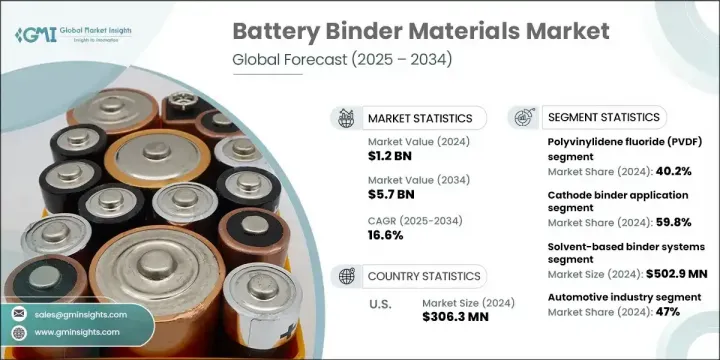

世界の電池バインダー材料市場は2024年に12億米ドルと評価され、CAGR 16.6%で成長し、2034年には57億米ドルに達すると推定されています。

この増加動向は、電気自動車、モバイルエレクトロニクス、再生可能エネルギー貯蔵システムなど、様々な高成長セグメントにおけるリチウムイオン電池の需要増による影響が大きいです。電池バインダーは、活性粒子を電極集電体に固定するために使用される特殊なポリマーであり、高効率、高容量、長寿命の電池を設計する上でますます重要になってきています。構造的な「接着剤」としての役割は、凝集結合と耐久性を保証し、バッテリーの機械的完全性とサイクル性能に直接影響します。

ウェアラブルやスマートフォンのような最新の消費者向け機器のためのエネルギー密度の高いコンパクトなバッテリー設計の拡大は、バインダー材料の配合における技術革新を加速させています。再生可能エネルギーのインフラに大規模なバッテリー貯蔵システムが統合されたことで、長寿命で熱的に安定したバインダーの必要性が急激に高まっています。メーカーは、電極の凝集力を高め、機械的強度を高め、柔軟性を向上させる次世代のアクリル系バインダーの製造に注力しています。軽量部品と環境適合性を重視する開発の高まりが製品開発の舵取りを続けており、サステイナブル材料の採用が進むにつれ、先端製造セグメントでの需要がさらに高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 12億米ドル |

| 予測金額 | 57億米ドル |

| CAGR | 16.6% |

カソードバインダーセグメントは2024年に59.8%のシェアを占め、2034年のCAGRは16.5%と予測されます。これらのバインダーは、厳しい充放電サイクル下でカソードの耐久性と性能を維持するために不可欠です。なかでもPVDF(ポリフッ化ビニリデン)は、堅牢な耐薬品性と耐熱性、信頼性の高い接着性、幅広いカソード材料との適合性で知られています。カソードバインダーは、活物質が集電体表面に効果的に接続された状態を維持し、電池の安定性と出力効率に貢献する上で重要な役割を果たします。

2024年の溶剤系バインダーシステムセグメントの市場規模は5億290万米ドルで、2034年のCAGRは16.8%と予測されています。歴史的に、NMPを使用したPVDFベース溶剤バインダーは、優れた接着性、化学的耐性、性能を提供できるため、電池製造に好んで使用されてきました。しかし、こうした材料は現在、欧州のや北米のなどの主要地域で環境・安全規制が強化され、規制強化に直面しています。溶剤系が依然として主流である一方、水性やよりエコフレンドリーバインダー技術へのシフトが状況を変えつつあり、メーカーは性能を犠牲にすることなく、よりクリーンでコンプライアンスに適合した代替品への移行を進めています。

米国電池バインダー材料2024年の市場規模は3億630万米ドルで、2034年のCAGRは13.7%の成長が見込まれます。米国は、堅調な電気自動車の展開、エネルギー貯蔵への多額の投資、根強い製造エコシステムに後押しされ、バッテリー・バインダー技術革新の中心拠点として繁栄を続けています。国内のバッテリー・サプライチェーンに対する連邦政府の広範な支援は、先進的な接着剤生産に対する財政的インセンティブと相まって、この急速に発展する市場における米国の骨格を固めています。また、戦略的な資本注入により、SBRやPVDFのような次世代バインダー材料の生産能力も向上しており、地域開発をさらに促進しています。

世界の電池バインダー材料市場をリードする主要企業には、Zeon Corporation、Solvay S.A.、Chemours Company、Sinochem Lantian、Dongyue Group、Arkema S.A.、Kureha Corporation、Shanghai 3F New Materials、JSR Corporation、Shandong Huaxia Shenzhou New Materialなどがあります。これらの企業は、世界の持続可能性目標を満たす、環境に優しく高性能なバインダー配合を開発するため、研究開発に多額の投資を行っています。電池セルメーカーやOEMとの提携により、次世代電池システムへの新材料の迅速な統合が可能になっています。各社はまた、生産能力を拡大し、合弁事業に参入して地域的なリーチを強化しています。規制状況の変化に対応するため、市場情勢をリードする各社は、製造時の拡大性とエネルギー効率に重点を置きながら、従来型溶剤系システムから水性代替システムへの移行を進めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 電気自動車市場の拡大

- エネルギー貯蔵システムの導入

- 民生用電子機器製品の需要増加

- バッテリー性能向上要件

- 産業の潜在的リスク・課題

- 高い材料費と価格変動

- 環境と安全規制

- 技術的なパフォーマンスの制限

- サプライチェーンの集中リスク

- 市場機会

- 次世代バッテリー技術

- サステイナブルバイオベースバインダーの開発

- シリコンアノード技術の採用

- 新興市場への浸透

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品タイプ別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)

- (注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- ポリフッ化ビニリデン(PVDF)

- カルボキシメチルセルロース(CMC)

- スチレンブタジエンゴム(SBR)

- ポリアクリル酸(PAA)

- その他の特殊バインダー

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- カソードバインダーの用途

- NCMカソードシステム

- NCAカソードシステム

- LFPカソードシステム

- 高電圧カソード材料

- アノードバインダーの用途

- 黒鉛アノードシステム

- シリコンベースアノードシステム

- チタン酸リチウム(LTO)システム

- 次世代アノード材料

第7章 市場推定・予測:技術別、2021~2034年

- 主要動向

- 溶剤系バインダーシステム

- 従来型PVDFシステム

- 水性バインダーシステム

- CMC/SBRの組み合わせ

- ハイブリッドバインダーシステム

- 多成分配合

- 次世代技術

- 固体電池バインダー

- 導電性バインダーネットワーク

- 自己修復材料

第8章 市場推定・予測:最終用途産業別、2021~2034年

- 主要動向

- 自動車産業

- 電気乗用車

- 電気商用車

- ハイブリッド電気自動車

- 民生用電子機器

- スマートフォンとタブレット

- ノートパソコンとポータブルデバイス

- ウェアラブル電子機器

- ゲームとエンターテイメント機器

- エネルギー貯蔵システム

- グリッドスケールのエネルギー貯蔵

- 住宅エネルギー貯蔵

- 商業と産業用貯蔵

- 再生可能エネルギーの統合

- 産業用途

- マテリアルハンドリング機器

- バックアップ電源システム

- 通信インフラ

- 医療とヘルスケア機器

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第10章 企業プロファイル

- Arkema S.A.

- Chemours Company

- Dongyue Group

- JSR Corporation

- Kureha Corporation

- Shandong Huaxia Shenzhou New Material

- Shanghai 3F New Materials

- Sinochem Lantian

- Solvay S.A.

- Zeon Corporation

目次

The Global Battery Binder Materials Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 16.6% to reach USD 5.7 billion by 2034. This upward trend is largely influenced by the escalating demand for lithium-ion batteries across a variety of high-growth sectors such as electric vehicles, mobile electronics, and renewable energy storage systems. Battery binders-specialized polymers used to secure active particles to electrode current collectors-are becoming increasingly vital in designing batteries with greater efficiency, higher capacity, and extended lifespans. Their role as structural "adhesives" ensures cohesive binding and durability, directly impacting the battery's mechanical integrity and cycle performance.

The expansion of energy-dense, compact battery designs for modern consumer devices like wearables and smartphones is accelerating innovation in binder material formulations. With the integration of large-scale battery storage systems into renewable energy infrastructure, the need for long-lasting and thermally stable binders has grown sharply. Manufacturers are focusing on producing next-generation acrylic-based binders to boost electrode cohesion, enhance mechanical strength, and improve flexibility. Rising emphasis on lightweight components and environmental compatibility continues to steer product development, while growing adoption of sustainable materials further elevates demand in advanced manufacturing sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 16.6% |

The cathode binders segment held 59.8% share in 2024, with projected growth at a CAGR of 16.5% through 2034. These binders are essential in maintaining cathode durability and performance under rigorous charge-discharge cycles. Among the most used materials is PVDF (polyvinylidene fluoride), known for its robust chemical and thermal resistance, reliable adhesion, and compatibility with a wide range of cathode materials. Cathode binders play a critical role in ensuring that the active materials remain effectively connected to the collector surface, thereby contributing to battery stability and output efficiency.

In 2024, the solvent-based binder systems segment was valued at USD 502.9 million and is projected to grow at a CAGR of 16.8% through 2034. Historically, PVDF-based solvent binders using NMP were favored in battery manufacturing due to their ability to offer superior adhesion, chemical resilience, and performance. However, these materials are now facing tighter restrictions due to increasing environmental and safety regulations in key regions like Europe and North America. While solvent-based systems still dominate, the shift toward water-based and more eco-friendly binder technologies is reshaping the landscape, pushing manufacturers toward cleaner and more compliant alternatives without compromising performance.

United States Battery Binder Materials Market generated USD 306.3 million in 2024, with expected growth at a CAGR of 13.7% through 2034. The nation continues to thrive as a central hub for battery binder innovation, propelled by its robust electric vehicle rollout, significant investments in energy storage, and deep-rooted manufacturing ecosystem. Extensive federal support for domestic battery supply chains, combined with financial incentives for advanced adhesive production, has strengthened the U.S. foothold in this fast-evolving market. Strategic capital infusion is also advancing production capabilities for next-gen binder materials like SBR and PVDF, further driving local development.

Key companies leading the Global Battery Binder Materials Market include Zeon Corporation, Solvay S.A., Chemours Company, Sinochem Lantian, Dongyue Group, Arkema S.A., Kureha Corporation, Shanghai 3F New Materials, JSR Corporation, and Shandong Huaxia Shenzhou New Material. They are investing significantly in R&D to develop environmentally friendly and high-performance binder formulations that meet global sustainability goals. Collaborations with battery cell manufacturers and OEMs are enabling faster integration of new materials into next-generation battery systems. Companies are also expanding production capacity and entering joint ventures to strengthen their regional reach. To comply with shifting regulatory landscapes, market leaders are transitioning from traditional solvent-based systems to water-based alternatives while focusing on scalability and energy efficiency during manufacturing.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 Technology

- 2.2.5 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electric vehicle market expansion

- 3.2.1.2 Energy storage system deployment

- 3.2.1.3 Consumer electronics demand growth

- 3.2.1.4 Battery performance enhancement requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High material costs and price volatility

- 3.2.2.2 Environmental and safety regulations

- 3.2.2.3 Technical performance limitations

- 3.2.2.4 Supply chain concentration risks

- 3.2.3 Market opportunities

- 3.2.3.1 Next-generation battery technologies

- 3.2.3.2 Sustainable and bio-based binder development

- 3.2.3.3 Silicon anode technology adoption

- 3.2.3.4 Emerging market penetration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyvinylidene Fluoride (PVDF)

- 5.3 Carboxymethyl Cellulose (CMC)

- 5.4 Styrene-Butadiene Rubber (SBR)

- 5.5 Polyacrylic Acid (PAA)

- 5.6 Other Specialty Binders

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cathode binder applications

- 6.2.1 NCM cathode systems

- 6.2.2 NCA cathode systems

- 6.2.3 LFP cathode systems

- 6.2.4 High-voltage Cathode Materials

- 6.3 Anode binder applications

- 6.3.1 Graphite anode systems

- 6.3.2 Silicon-based anode systems

- 6.3.3 Lithium titanate oxide (LTO) systems

- 6.3.4 Next-generation anode materials

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Solvent-based binder systems

- 7.2.1 Traditional PVDF systems

- 7.3 Water-based binder systems

- 7.3.1 CMC/SBR combinations

- 7.4 Hybrid binder systems

- 7.4.1 Multi-component formulations

- 7.5 Next-generation technologies

- 7.5.1 Solid-state battery binders

- 7.5.2 Conductive binder networks

- 7.5.3 Self-healing materials

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Automotive industry

- 8.2.1 Electric passenger vehicles

- 8.2.2 Electric commercial vehicles

- 8.2.3 Hybrid electric vehicles

- 8.3 Consumer electronics

- 8.3.1 Smartphones and tablets

- 8.3.2 Laptops and portable devices

- 8.3.3 Wearable electronics

- 8.3.4 Gaming and entertainment devices

- 8.4 Energy storage systems

- 8.4.1 Grid-scale energy storage

- 8.4.2 Residential energy storage

- 8.4.3 Commercial and industrial storage

- 8.4.4 Renewable energy integration

- 8.5 Industrial applications

- 8.5.1 Material handling equipment

- 8.5.2 Backup power systems

- 8.5.3 Telecommunications infrastructure

- 8.5.4 Medical and healthcare devices

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arkema S.A.

- 10.2 Chemours Company

- 10.3 Dongyue Group

- 10.4 JSR Corporation

- 10.5 Kureha Corporation

- 10.6 Shandong Huaxia Shenzhou New Material

- 10.7 Shanghai 3F New Materials

- 10.8 Sinochem Lantian

- 10.9 Solvay S.A.

- 10.10 Zeon Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日