|

市場調査レポート

商品コード

1797701

ケイ素ベースバイオスティミュラント市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Silicon Based Biostimulants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ケイ素ベースバイオスティミュラント市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年07月30日

発行: Global Market Insights Inc.

ページ情報: 英文 192 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

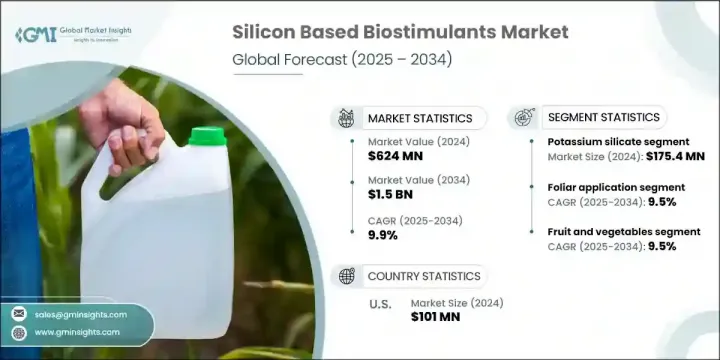

世界のケイ素ベースバイオスティミュラント市場は、2024年には6億2,400万米ドルと評価され、CAGR 9.9%で成長し、2034年には15億米ドルに達すると予測されています。

この市場は、農業が持続可能で弾力性のある農法を優先し続ける中で牽引力を増しています。環境に配慮した効率的な栽培方法へのシフトが進んでいるため、さまざまな農業システムでシリコンベースの投入物に対する需要が高まっています。農業が生物学的および生物学的ストレスの影響を緩和することにますます重点を置くようになる中、これらの生物刺激剤は、植物の健康、収量の安定性、環境圧力への耐性をサポートする能力を理由に採用されています。

この業界の拡大は、研究の活発化、製品の革新、スマート農業技術への関心の高まりに支えられています。農場が化学薬品への依存を減らし、作物の成果を向上させる方法に移行するにつれ、ケイ素を強化した製剤が世界の生産者の間で支持されるようになっています。市場のダイナミックな性質は、特に作物の回復力の向上やストレス下での植物代謝の最適化といった強力な製品性能によってさらに後押しされています。世界のいくつかの地域では、洗練された農業慣行が、再生可能で持続可能な農業への幅広いコミットメントを反映し、このカテゴリーに特化した製品の台頭に有利な条件を作り出しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 6億2,400万米ドル |

| 予測金額 | 15億米ドル |

| CAGR | 9.9% |

市場開拓で注目すべきは、ナノシリコン生物刺激剤の出現です。これらの高度な製剤は、ケイ素ナノ粒子を使用して生物学的利用能(バイオアベイラビリティ)を高め、植物への取り込みの改善やストレスに対する抵抗性の向上など、目標とする利益をもたらします。このような技術革新は、高価値作物や精密農業にとってますます魅力的になっています。研究が深まり商業化が加速するにつれ、複雑な農業システム全体におけるナノシリコンの利点を裏付ける科学的知見の増加によって、新たな機会が表面化しています。この動向は、技術的に先進的な農業地域に新たな成長の道を開くと予想されます。

気候の変動や土壌の健康状態の悪化が世界的に懸念される中、農家と農業関連企業の双方がよりスマートな解決策を模索しています。ケイ素ベースバイオスティミュラントは、重金属曝露、干ばつ、土壌塩分などの環境課題に対する農業の回復力を高めるのに役立っています。こうしたソリューションは、持続可能な農業投入物を求める世界の機運に沿ったものであり、気候変動に配慮した食糧生産システムにとって不可欠な要素になりつつあります。生産者が生態系のバランスを損なうことなく植物の健全性を高める効果的な方法を求めているため、こうした製品の採用は農業のあらゆる分野で増加しています。

製品タイプ別では、ケイ酸カリウム・セグメントは1億7,540万米ドルを生み出し、2024年には28.1%のシェアを占めました。多様な農業環境において安定した性能を発揮することから、信頼性の高いバイオスティミュラントの選択肢を求める生産者の間で最有力な選択肢であり続けています。

葉面散布分野は2024年に34.1%のシェアを占め、2034年までCAGR 9.5%で成長します。この技術は、植物の葉を通してケイ素を迅速に吸収でき、すぐに効果が得られるため人気があります。植物の状態、ストレス耐性、収量品質が目に見えて改善されることが、迅速で測定可能な成果を目指す生産者や園芸家の間で広く採用されている主な理由です。

2024年の米国のケイ素ベースバイオスティミュラント市場規模は1億100万米ドルで、シェアは80.1%。この分野における同国のリーダーシップは、強力な規制の枠組み、アグリ・テクノロジーの急速な進歩、環境スチュワードシップの広範な重視によって支えられています。ケイ素ベースバイオスティミュラントは、作物生産戦略、特に収量とストレス耐性の強化が最優先課題である穀物・農産物栽培において不可欠なものとなっています。農家がますます予測不可能になる気候条件に対応するにつれ、こうした製品の作物管理プログラムへの統合は着実に拡大しています。

ケイ素ベースバイオスティミュラント市場を形成する主要企業には、Syngenta AG、UPL Limited、Corteva Inc.、Bayer AG、BASF SEなどがあります。シリコン系バイオスティミュラント分野の主要企業は、技術革新、提携、世界展開の組み合わせを通じて市場での地位を強化しています。各社は、高度な製剤、特に高精度の送達と効能の向上を提供するナノシリコン技術を開発するため、研究開発に多額の投資を行っています。農業研究機関や技術プロバイダーとの戦略的提携により、製品開発と商業化が加速しています。また、多くの企業が、地理的な足跡を拡大するために、買収や合弁事業を通じて新興市場に参入しています。地域の作物要件や規制基準に合わせて製品をカスタマイズすることが、重要な焦点となっています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 持続可能な農業への需要の高まり

- 作物のストレス耐性と収量の向上

- バイオ刺激剤の使用に対する規制支援

- 製品配合とナノテクノロジーの進歩

- 業界の潜在的リスク&課題

- 農家の意識と教育の不足

- 従来の投入物に比べてコストが高め

- 市場機会

- 新興市場への拡大

- 精密農業とデジタル農業との統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品タイプ別

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ケイ酸カリウム

- ケイ酸ナトリウム

- 安定化ケイ酸

- シリコンナノ粒子

- その他のシリコン化合物

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 葉面散布

- 土壌への施用

- 種子処理

- 灌水施肥と水耕栽培

第7章 市場推計・予測:作物別、2021年~2034年

- 主要動向

- 穀物

- 果物と野菜

- 産業用作物

- 芝生と観賞用植物

- その他の特殊作物

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東およびアフリカ

第9章 企業プロファイル

- BASF SE

- Eutrema

- Haifa Group

- Intermag

- Nuvia Technologies

- Orion Future Technology Ltd

- Plant Food Company Inc

- PlantoSys Nederland B.V.

- Roam Technology

- Shield Lifesciences and Resins Pvt Ltd

- Sustainable Agro Solutions S.A

- Syngenta AG

The Global Silicon Based Biostimulants Market was valued at USD 624 million in 2024 and is estimated to grow at a CAGR of 9.9% to reach USD 1.5 billion by 2034. This market is gaining traction as agriculture continues to prioritize sustainable and resilient farming methods. The ongoing shift toward eco-conscious and efficient cultivation practices is driving the demand for silicon-based inputs across various farming systems. With agriculture's increasing focus on mitigating the effects of biotic and abiotic stress, these biostimulants are being adopted for their ability to support plant health, yield stability, and resistance to environmental pressures.

The expansion of the industry is backed by rising research, product innovation, and growing interest in smart agriculture technologies. As farms transition to methods that reduce chemical reliance and improve crop outcomes, silicon-enhanced formulations are finding favor among producers globally. The dynamic nature of the market is further propelled by strong product performance, particularly in improving crop resilience and optimizing plant metabolism under stress. Sophisticated agricultural practices in several parts of the world are creating favorable conditions for the rise of specialized products in this category, reflecting a wider commitment to regenerative and sustainable farming.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $624 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 9.9% |

A notable development in the market is the emergence of nano-silicon biostimulants. These advanced formulations use silicon nanoparticles to enhance bioavailability and deliver targeted benefits, such as improved plant uptake and increased resistance to stress. Such innovations are becoming increasingly attractive for high-value crops and precision agriculture. As research deepens and commercialization gains speed, new opportunities are surfacing, driven by a rise in scientific findings that support the advantages of nano-silicon across complex farming systems. This trend is expected to open fresh pathways for growth in technologically advanced agricultural regions.

Amid global concerns about climate shifts and deteriorating soil health, both farmers and agribusinesses are exploring smarter solutions. Silicon-based biostimulants are proving instrumental in boosting agricultural resilience to environmental challenges, including heavy metal exposure, drought, and soil salinity. These solutions align with the global momentum toward sustainable agricultural inputs, which are becoming an essential part of climate-conscious food production systems. The adoption of these products is increasing across the farming spectrum as growers seek effective ways to enhance plant health without compromising ecological balance.

In terms of product type, the potassium silicate segment generated USD 175.4 million and held 28.1% share in 2024 due to its proven effectiveness in boosting plant strength and stress response across multiple crop types. Its consistent performance in diverse agricultural environments continues to make it a top choice among growers looking for reliable biostimulant options.

The foliar segment held a 34.1% share in 2024 and will grow at a 9.5% CAGR through 2034. This technique is popular because it enables rapid absorption of silicon through plant foliage and delivers immediate benefits. Visible improvements in plant condition, stress resistance, and yield quality are key reasons for its widespread adoption among growers and horticulturists aiming for fast, measurable outcomes.

United States Silicon Based Biostimulants Market generated USD 101 million in 2024 and held an 80.1% share. The country's leadership in the sector is supported by a strong regulatory framework, rapid advancements in agri-tech, and widespread emphasis on environmental stewardship. Silicon-based biostimulants have become integral in crop production strategies, particularly in grain and produce farming, where enhancing yield and stress tolerance are top priorities. The integration of these products into crop management programs is steadily expanding as farmers respond to increasingly unpredictable climate conditions.

Key players shaping the Silicon Based Biostimulants Market include Syngenta AG, UPL Limited, Corteva Inc., Bayer AG, and BASF SE. Leading firms in the silicon-based biostimulants sector are reinforcing their market positions through a combination of innovation, partnerships, and global expansion. Companies are heavily investing in R&D to create advanced formulations, particularly nano-silicon technologies that offer precision delivery and improved efficacy. Strategic collaborations with agricultural research institutions and tech providers are accelerating product development and commercialization. Many players are also entering emerging markets through acquisitions and joint ventures to expand their geographic footprint. Customization of product offerings to meet regional crop requirements and regulatory standards has become a critical focus.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application method

- 2.2.4 Crop type

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sustainable agriculture

- 3.2.1.2 Enhanced crop stress tolerance and yield

- 3.2.1.3 Regulatory support for biostimulants use

- 3.2.1.4 Advancements in product formulations and nanotechnology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited farmer awareness and education

- 3.2.2.2 Higher cost compared to conventional inputs

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Integration with precision and digital agriculture

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Million, Tons)

- 5.1 Key trends

- 5.2 Potassium silicate

- 5.3 Sodium silicate

- 5.4 Stabilized silicic acid

- 5.5 Silicon nanoparticles

- 5.6 Other silicon compounds

Chapter 6 Market Estimates & Forecast, By Application Method, 2021 - 2034 (USD Million, Tons)

- 6.1 Key trends

- 6.2 Foliar application

- 6.3 Soil application

- 6.4 Seed treatment

- 6.5 Fertigation and hydroponic

Chapter 7 Market Estimates & Forecast, By Crop Type, 2021 - 2034 (USD Million, Tons)

- 7.1 Key trends

- 7.2 Cereals and grains

- 7.3 Fruits and vegetables

- 7.4 Industrial crops

- 7.5 Turf and ornamentals

- 7.6 Other specialty crops

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million, Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Italy

- 8.3.4 Spain

- 8.3.5 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Eutrema

- 9.3 Haifa Group

- 9.4 Intermag

- 9.5 Nuvia Technologies

- 9.6 Orion Future Technology Ltd

- 9.7 Plant Food Company Inc

- 9.8 PlantoSys Nederland B.V.

- 9.9 Roam Technology

- 9.10 Shield Lifesciences and Resins Pvt Ltd

- 9.11 Sustainable Agro Solutions S.A

- 9.12 Syngenta AG