結核診断検査市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Tuberculosis Diagnostics Test Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 145 Pages

- 納期

- 2~3営業日

- 商品コード

- 1782157

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

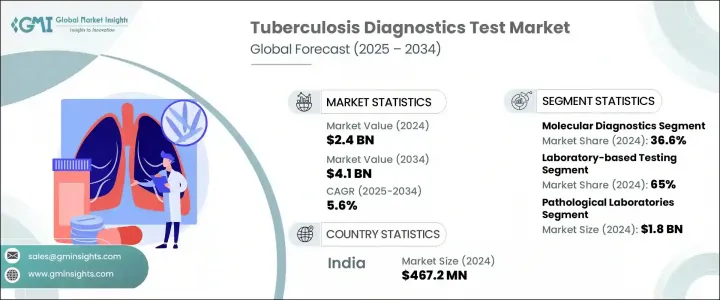

世界の結核診断検査市場は、2024年に24億米ドルと評価され、CAGR 5.6%で成長し、2034年には41億米ドルに達すると推定されています。

世界の結核蔓延率の増加は、診断技術の進歩や公衆衛生意識の急上昇と相まって、信頼性の高い検査ツールへの需要を煽っています。ポイント・オブ・ケア検査の導入が進み、計画的なスクリーニング・プログラムの実施が早期発見率の向上に役立っています。官民両部門が支援するこれらの取り組みは、結核の蔓延を抑制する上で極めて重要なステップであるタイムリーな診断と治療を合理化することを目的としています。

市場拡大の主な要因は、早期スクリーニングの取り組みを強化する世界の取り組みです。政府が支援するヘルスケアプログラムでは、高リスク集団を支援するための体系的な戦略を展開し、診断へのアクセスを向上させています。こうした取り組みにより、地域密着型の検査やアウトリーチによる早期発見が加速しています。結核診断検査は、結核菌の存在を検出し、個人が活動性結核か潜在性結核感染かを判定するために使用されます。正確な同定がより重視される中、同市場では引き続き、診断プラットフォーム全体の技術革新とインフラへの投資が拡大しています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 24億米ドル |

| 予測金額 | 41億米ドル |

| CAGR | 5.6% |

2024年には、分子診断薬が主要セグメントとして浮上し、シェア36.6%を占め、2034年までのCAGRは5.9%と予測されます。これらの診断薬は、結核菌とその薬剤耐性形質を迅速、高感度、高精度に検出することで、これまでの常識を覆しました。この分野の中心的技術であるポリメラーゼ連鎖反応(PCR)の使用により、ヘルスケアプロバイダーは臨床検体から結核菌を正確に検出できるようになり、早期の治療決定をより効果的に行えるようになりました。

ラボベースの検査カテゴリーは、2024年に65%の最大シェアを占めました。その優位性は主に、複雑な薬剤耐性結核症例の診断に不可欠な、正確で集中的な検査方法の使用に起因します。これらの検査は通常、病院、公衆衛生機関、民間の認定検査機関で実施されます。一般的な検査技術には、塗抹顕微鏡検査、培養ベースの診断、インターフェロン-ガンマ放出アッセイ(IGRA)などがあり、いずれも疾患の重症度や潜在的な耐性について詳細な洞察を提供し、臨床医がオーダーメイドの治療計画を立てる際の指針となります。

アジア太平洋地域の結核診断検査市場は、2025年から2034年にかけてCAGR 5.6%で成長すると予測されています。この成長の要因としては、結核患者数の増加、公衆衛生教育の拡大、診断ラボへのアクセスの拡大、診断インフラの強化を目的とした政府の支援政策などが挙げられます。同地域ではヘルスケアへの投資が続いているため、先進的な結核検査ソリューションへの需要が高まると予測されます。

この分野をリードする主要企業には、Danaher Corporation, Abbott Laboratories, bioMerieux, Qiagen N.V., Becton, Dickinson and Company, and F. Hoffmann-La Rocheなどがあります。市場での存在感を高めるため、トップ企業は分子診断・迅速診断技術を進歩させる研究開発に多額の投資を行っています。ヘルスケアプロバイダーや研究機関との戦略的合併や共同研究は、各社の診断ポートフォリオや世界な事業展開の拡大に役立っています。いくつかの企業は、特に高負荷地域における低資源環境向けに、低コストで携帯可能な結核検査ソリューションの開発に注力しています。さらに、メーカーは検査感度を最適化し、納期を短縮し、自社のプラットフォームが国際的な規制基準を満たしていることを保証しています。このような戦略により、アクセシビリティ、正確性、効率性が強化され、各社は長期的な市場リーダーとしての地位を確立しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界的に結核の負担が増加

- 結核診断技術の進歩

- 結核に関する意識向上とスクリーニングプログラムの実施

- ポイントオブケア検査(POCT)の急増

- 業界の潜在的リスク&課題

- 感度と特異度の限界

- 厳しい規制シナリオ

- 促進要因

- 成長可能性分析

- 技術的情勢

- 規制情勢

- 北米

- 欧州

- 将来の市場動向

- 価格分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:検査の種類別、2021年~2034年

- 主要動向

- 放射線学的方法

- 診断実験方法

- 顕微鏡検査

- 培養に基づく技術

- 血清学的検査

- 分子診断

- ポリメラーゼ連鎖反応(PCR)

- 核酸増幅検査(NAAT)

- GeneXpert MTB/RIF

- 潜在感染の検出

- ツベルクリン皮膚テスト(TST)/精製タンパク質誘導体(PPD)

- 第一世代のPPDベースのTST

- 組み換え抗原を用いた新世代の皮膚検査

- ツベルクリン皮膚テスト(TST)/精製タンパク質誘導体(PPD)

- インターフェロンガンマ遊離試験(IGRA)

- ELISAベースのIGRA

- ELISPOTベースのIGRA

- ポイントオブケアIGRA

- サイトカイン検出アッセイ

- 薬剤耐性の検出(DST)

- ファージアッセイ

- その他の検査の種類

第6章 市場推計・予測:モダリティ別、2021年~2034年

- 主要動向

- ポイントオブケア検査(POCT)

- 臨床検査(非POCT)

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病理学検査室

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- Anhui Zhifei Longcom Biopharmaceutical Co.

- Becton, Dickinson and Company

- bioMerieux

- Danaher Corporation(Cepheid)

- F. Hoffmann-La Roche

- Generium Pharmaceuticals

- Hain Lifescience

- Hologic

- Japan BCG Laboratory

- NIPRO

- Oxford Immunotec

- Qiagen N.V.

- Sanofi

- Siemens Healthineers

- Thermo Fisher Scientific

目次

The Global Tuberculosis Diagnostics Test Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 4.1 billion by 2034. Increasing TB prevalence worldwide, coupled with advancements in diagnostic technologies and a sharp rise in public health awareness, are fueling demand for reliable testing tools. The rising adoption of point-of-care testing and the implementation of structured screening programs are helping improve early detection rates. These efforts, supported by both public and private sectors, aim to streamline timely diagnosis and treatment, crucial steps in controlling the spread of tuberculosis.

A major driver behind the market's expansion is the global effort to strengthen early screening initiatives. Government-backed healthcare programs are rolling out structured strategies to support high-risk populations with better diagnostic access. These initiatives are accelerating early identification through community-based testing and outreach. Tuberculosis diagnostic tests are used to detect the presence of the mycobacterium tuberculosis bacteria and to determine if an individual has active TB or a latent TB infection, which is essential for guiding treatment decisions. With more emphasis on accurate identification, the market continues to witness greater investment in innovation and infrastructure across diagnostic platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 5.6% |

In 2024, molecular diagnostics emerged as the leading segment, contributing 36.6% share and projected to grow at a CAGR of 5.9% through 2034. These diagnostics have changed the game by offering fast, sensitive, and accurate detection of Mycobacterium tuberculosis and its drug resistance traits. The use of polymerase chain reaction (PCR) as a central technique in this space enables healthcare providers to detect TB bacteria from clinical samples with precision, making early treatment decisions more effective.

The laboratory-based testing category held the largest share 65% in 2024. Its dominance is primarily attributed to the use of accurate, centralized testing methods critical for diagnosing complex and drug-resistant TB cases. These tests are typically performed in hospitals, public health institutions, and private certified laboratories. Common testing techniques include smear microscopy, culture-based diagnostics, and interferon-gamma release assays (IGRAs), all of which offer in-depth insight into disease severity and potential resistance, guiding clinicians in creating tailored treatment plans.

Asia Pacific Tuberculosis Diagnostics Test Market is expected to grow at a CAGR of 5.6% from 2025 to 2034. Factors contributing to this growth include the increasing number of TB cases, expanding public health education, greater access to diagnostic labs, and supportive governmental policies aimed at strengthening diagnostic infrastructure. As the region continues to invest in healthcare, the demand for advanced TB testing solutions is forecasted to rise.

Prominent players leading this space include Danaher Corporation, Abbott Laboratories, bioMerieux, Qiagen N.V., Becton, Dickinson and Company, and F. Hoffmann-La Roche. To strengthen their market presence, top firms are heavily investing in R&D to advance molecular and rapid diagnostic technologies. Strategic mergers and collaborations with healthcare providers and research institutions are helping companies expand their diagnostic portfolios and global footprint. Several players are focusing on creating low-cost, portable TB testing solutions tailored for low-resource settings, particularly in high-burden regions. Additionally, manufacturers are optimizing test sensitivity, reducing turnaround time, and ensuring their platforms meet international regulatory standards. These strategies collectively enhance accessibility, accuracy, and efficiency, positioning companies for long-term market leadership.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Test type

- 2.2.3 Modality

- 2.2.4 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising burden of tuberculosis globally

- 3.2.1.2 Advancement in tuberculosis diagnostics techniques

- 3.2.1.3 Increasing awareness and screening programs regarding tuberculosis

- 3.2.1.4 Surge in point-of-care testing (POCT)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited sensitivity and specificity

- 3.2.2.2 Stringent regulatory scenario

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technological landscape

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy outlook matrix

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Radiographic method

- 5.3 Diagnostic laboratory methods

- 5.3.1 Microscopy

- 5.3.2 Culture-based techniques

- 5.3.3 Serological tests

- 5.4 Molecular diagnostics

- 5.4.1 Polymerase chain reaction (PCR)

- 5.4.2 Nucleic acid amplification tests (NAAT)

- 5.4.3 GeneXpert MTB/RIF

- 5.5 Detection of latent infection

- 5.5.1 Tuberculin skin test (TST)/ Purified protein derivative (PPD)

- 5.5.1.1 First-generation PPD-based TSTs

- 5.5.1.2 New-generation skin tests with recombinant antigens

- 5.5.1 Tuberculin skin test (TST)/ Purified protein derivative (PPD)

- 5.6 Interferon-gamma release assays (IGRAs)

- 5.6.1.1 ELISA-based IGRAs

- 5.6.1.2 ELISPOT-based IGRAs

- 5.6.1.3 Point-of-care IGRAs

- 5.7 Cytokine detection assays

- 5.8 Detection of drug resistance (DST)

- 5.9 Phage assay

- 5.10 Other test types

Chapter 6 Market Estimates and Forecast, By Modality, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Point of care testing (POCT)

- 6.3 Laboratory-based testing (Non-POCT)

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pathological laboratories

- 7.3 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Anhui Zhifei Longcom Biopharmaceutical Co.

- 9.3 Becton, Dickinson and Company

- 9.4 bioMerieux

- 9.5 Danaher Corporation (Cepheid)

- 9.6 F. Hoffmann-La Roche

- 9.7 Generium Pharmaceuticals

- 9.8 Hain Lifescience

- 9.9 Hologic

- 9.10 Japan BCG Laboratory

- 9.11 NIPRO

- 9.12 Oxford Immunotec

- 9.13 Qiagen N.V.

- 9.14 Sanofi

- 9.15 Siemens Healthineers

- 9.16 Thermo Fisher Scientific

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 145 Pages

- 納期

- 2~3営業日