免疫グロブリンの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Immunoglobulin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1782149

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

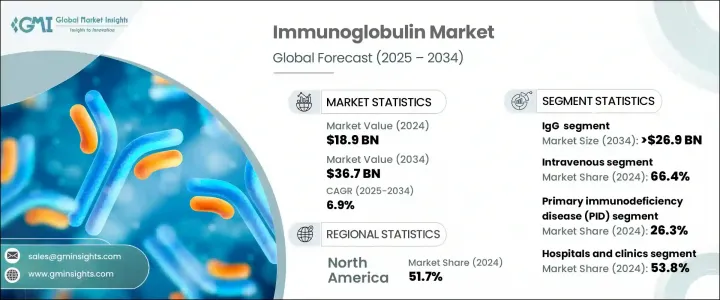

世界の免疫グロブリン市場は、2024年には189億米ドルと評価され、CAGR 6.9%で成長し、2034年には367億米ドルに達すると推定されています。

この市場拡大の主な要因は、様々な年齢層で一次性・二次性ともに免疫不全症が増加していることです。診断法の継続的な進歩とヘルスケア提供者の意識の高まりにより、慢性炎症性脱髄性多発神経炎や多巣性運動ニューロパチーのような複雑な疾患の発見率は着実に増加しています。

これらの疾患は、症状のコントロールや感染症の予防に重要な役割を果たす免疫グロブリン療法を含む生涯にわたる治療を必要とすることが多く、一貫した製品需要に拍車をかけています。免疫グロブリンは免疫系に不可欠な成分であり、ウイルス、細菌、毒素などの有害な病原体を認識し中和する抗体として機能します。B細胞によって自然に産生されるこれらの糖タンパク質は、免疫系にさらなるサポートや調節が必要な患者に静脈内または皮下投与されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 189億米ドル |

| 予測金額 | 367億米ドル |

| CAGR | 6.9% |

自己免疫疾患や免疫不全症例における免疫グロブリンに基づく治療への信頼の高まりが、引き続き市場の見通しを強めています。これらの療法は、抗体欠損を修正し、免疫活性を調整するために使用され、患者に実行可能な長期的解決策を提供します。世界の慢性疾患罹患率の上昇と相まって平均寿命が延び、免疫サポートを必要とする患者層が拡大しているため、需要も拡大しています。免疫学の研究が進み、製品へのアクセスが向上するにつれて、神経学、血液学、内科学など多くの医療分野で免疫療法の利用が広まっています。継続的な技術革新、新興国市場における有利な償還シナリオ、血漿採取ネットワークへの戦略的投資により、市場の成長はさらに加速すると予想されます。

異なる免疫グロブリンクラスの中では、IgGが引き続き支配的な地位を占めています。2024年、IgGセグメントは74.1%の市場シェアを獲得し、2034年にはCAGR 6.8%で269億米ドルを超えると予測されています。IgGの優位性は、広範な臨床使用と幅広い疾患に対する有効性の確立に起因しています。IgGは循環抗体の中で最も高い割合を占めており、病原体の中和、受動免疫の提供、免疫関連疾患の管理に不可欠です。IgGは、その安定した治療性能と幅広い適用範囲から、ヘルスケアのあらゆる場面で好んで使用されています。一方、IgAセグメントは最も急成長しているセグメントの一つとして浮上しており、2034年までのCAGRは7.7%と予測されています。粘膜免疫におけるIgAの役割とその潜在的な治療用途に対する認識の高まりが、この勢いの増加に寄与しています。

用途の観点から、市場は慢性炎症性脱髄性多発神経炎、多巣性運動ニューロパチー、原発性および二次性免疫不全症、ギランバレー症候群、免疫性血小板減少性紫斑病、その他のニッチ疾患など、さまざまな疾患に区分されます。原発性免疫不全症(PID)分野は、2024年には26.3%のシェアで市場をリードし、CAGR 7.1%で拡大すると予測されています。同分野の需要を牽引しているのは、免疫機能を十分に維持するために一貫した治療が必要とされる、生涯にわたる疾患であることです。PID患者は機能的な抗体を産生する能力がなく、頻繁な感染症に非常に脆弱であるため、免疫グロブリンの投与は疾患管理の重要な要素となっています。感染症のリスクを軽減し、入院を制限し、全体的な患者の転帰を向上させる上で重要な役割を担っています。

最終用途別では、病院・診療所が2024年の市場シェア53.8%で世界市場を独占しています。これらの環境は、免疫グロブリン療法、特に医学的監督と特殊な機器を必要とする点滴療法を受ける患者の主要なケアポイントとして機能しています。病院の管理された環境は、安全な点滴の実施を保証し、副作用が発生した場合には即座に介入することができます。反復投与や長期投与が必要なことから、患者は一貫した安全な投与を病院や診療所に依存することが多いです。

地域別では、北米が2024年に51.7%のシェアを占め、最大市場に浮上しました。同地域は、先進的なヘルスケアシステム、強固な償還政策、血漿採取のための確立されたインフラストラクチャーなどの恩恵を受けています。免疫関連疾患の有病率が高く、臨床技術革新が進んでいることも、この地域をリードする要因となっています。高齢者人口の増加と診断能力の向上も、この地域の市場拡大に大きく寄与しています。

市場参入企業は、強力なサプライチェーン、継続的な製品革新、戦略的パートナーシップを通じてリーダーシップを維持しています。血漿分画の専門知識と治療上の一貫性を重視する姿勢が競争力を高めています。各社はまた、新たな需要を開発し、従来の製造技術への依存を減らすために新興市場に投資しており、より広範な世界市場浸透への道を開いています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 免疫不全疾患の発生率の上昇

- 神経疾患および自己免疫疾患への応用拡大

- 世界の人口高齢化

- 診断認識とスクリーニングプログラムの改善

- 業界の潜在的リスク&課題

- 治療費の高騰

- プラズマ供給の制約

- 市場機会

- 組み換え免疫グロブリンの開発

- 新興国における需要の高まり

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術的進歩

- 現在の技術動向

- 新興技術

- 償還シナリオ

- 将来の市場動向

- ギャップ分析

- パイプライン分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- IgG

- IgA

- IgM

- IgD

- IgE

第6章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 静脈内(IVIg)

- 皮下(SCIg)

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 慢性炎症性脱髄性多発神経炎(CIDP)

- 多巣性運動神経障害(MMN)

- 原発性免疫不全症(PID)

- 二次性免疫不全症(SID)

- ギランバレー症候群

- 免疫血小板減少性紫斑病(ITP)

- その他の用途

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院と診療所

- 外来手術センター

- 在宅ケアの設定

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- ADMA Biologics

- Baxter international

- Bio Products Laboratory

- CSL Behring

- Emergent BioSolutions

- Grifols SA

- Johnson &Johnson(Omrix Biopharmaceuticals)

- Kedrion Biopharma

- LFB Group

- Octapharma AG

- Pfizer

- Shanghai RAAS Blood Products

- Takeda Pharmaceutical Company

目次

The Global Immunoglobulin Market was valued at USD 18.9 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 36.7 billion by 2034. This expansion is largely attributed to the rising occurrence of immunodeficiency disorders, both primary and secondary, across various age groups. With continued advancements in diagnostics and greater awareness among healthcare providers, detection rates of complex conditions like chronic inflammatory demyelinating polyneuropathy and multifocal motor neuropathy are steadily increasing.

These conditions often require lifelong treatment involving immunoglobulin therapies, which play a key role in controlling symptoms and preventing infections, thereby fueling consistent product demand. Immunoglobulins are essential components of the immune system, functioning as antibodies that recognize and neutralize harmful pathogens such as viruses, bacteria, and toxins. Produced naturally by B cells, these glycoproteins are administered either intravenously or subcutaneously to patients whose immune systems require additional support or modulation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.9 Billion |

| Forecast Value | $36.7 Billion |

| CAGR | 6.9% |

The growing reliance on immunoglobulin-based therapies in autoimmune and immune deficiency cases continues to strengthen the market outlook. These therapies are used to correct antibody deficiencies and regulate immune activity, offering patients a viable long-term solution. Increasing life expectancy, coupled with a rise in chronic disease incidence globally, is creating a broader patient base that requires immune support, thereby adding to the demand pool. As immunology research progresses and product accessibility improves, the use of immunoglobulin therapy is gaining traction across numerous medical disciplines, including neurology, hematology, and internal medicine. Continuous innovation, favorable reimbursement scenarios in developed regions, and strategic investments in plasma collection networks are expected to further accelerate market growth.

Among the different immunoglobulin classes, IgG continues to hold the dominant position. In 2024, the IgG segment captured a market share of 74.1% and is anticipated to surpass USD 26.9 billion by 2034, with a CAGR of 6.8%. Its dominance stems from broad clinical usage and well-established efficacy in a wide range of conditions. IgG represents the highest proportion of circulating antibodies and is essential for neutralizing pathogens, offering passive immunity, and managing immune-related conditions. Its consistent therapeutic performance and wide application range make it the preferred choice across healthcare settings. Meanwhile, the IgA segment is emerging as one of the fastest-growing, projected to grow at a CAGR of 7.7% through 2034. Growing recognition of its role in mucosal immunity and its potential therapeutic applications is contributing to this increased momentum.

From an application perspective, the market is segmented into various conditions such as chronic inflammatory demyelinating polyneuropathy, multifocal motor neuropathy, primary and secondary immunodeficiency diseases, Guillain-Barre syndrome, immune thrombocytopenic purpura, and other niche disorders. The primary immunodeficiency disease (PID) segment led the market in 2024 with a share of 26.3% and is forecasted to expand at a CAGR of 7.1%. The demand in this segment is driven by the lifelong nature of the condition, which requires consistent immunoglobulin therapy to maintain adequate immune function. Patients with PID lack the ability to produce functional antibodies and are highly vulnerable to frequent infections, making immunoglobulin administration a vital component of disease management. It plays a critical role in reducing infection risks, limiting hospital admissions, and enhancing overall patient outcomes.

In terms of end use, the hospital and clinic segment dominated the global market with a market share of 53.8% in 2024. These settings serve as the primary point of care for patients receiving immunoglobulin therapy, particularly intravenous forms that demand medical supervision and specialized equipment. The controlled environment of hospitals ensures safe infusion practices and allows immediate intervention in case of adverse reactions. Given the requirement for repeated and long-term dosing, patients often rely on hospitals and clinics for consistent and secure administration.

Regionally, North America emerged as the largest market, commanding a share of 51.7% in 2024. The region benefits from advanced healthcare systems, robust reimbursement policies, and a well-established infrastructure for plasma collection. The high prevalence of immune-related disorders and ongoing clinical innovation further contribute to its leading position. The expanding elderly population and improved diagnostic capabilities are also key contributors to the region's market strength.

Market players are maintaining their leadership through strong supply chains, continuous product innovation, and strategic partnerships. Their expertise in plasma fractionation and focus on therapeutic consistency give them a competitive edge. Companies are also investing in emerging markets to tap into new demand and reduce dependence on traditional manufacturing techniques, paving the way for broader global market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Route of administration trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of immunodeficiency disorders

- 3.2.1.2 Expanding applications in neurological and autoimmune diseases

- 3.2.1.3 Global aging population

- 3.2.1.4 Improved diagnostic awareness and screening programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of therapy

- 3.2.2.2 Plasma supply constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Development of recombinant immunoglobulins

- 3.2.3.2 Rising demand in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Pipeline analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 IgG

- 5.3 IgA

- 5.4 IgM

- 5.5 IgD

- 5.6 IgE

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Intravenous (IVIg)

- 6.3 Subcutaneous (SCIg)

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Chronic inflammatory demyelinating polyneuropathy (CIDP)

- 7.3 Multifocal motor neuropathy (MMN)

- 7.4 Primary immunodeficiency disease (PID)

- 7.5 Secondary immunodeficiency disease (SID)

- 7.6 Guillain-Barre syndrome

- 7.7 Immune thrombocytopenic purpura (ITP)

- 7.8 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Ambulatory surgical centers

- 8.4 Homecare settings

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ADMA Biologics

- 10.2 Baxter international

- 10.3 Bio Products Laboratory

- 10.4 CSL Behring

- 10.5 Emergent BioSolutions

- 10.6 Grifols SA

- 10.7 Johnson & Johnson (Omrix Biopharmaceuticals)

- 10.8 Kedrion Biopharma

- 10.9 LFB Group

- 10.10 Octapharma AG

- 10.11 Pfizer

- 10.12 Shanghai RAAS Blood Products

- 10.13 Takeda Pharmaceutical Company

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日