改質アスファルトの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Modified Bitumen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773462

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

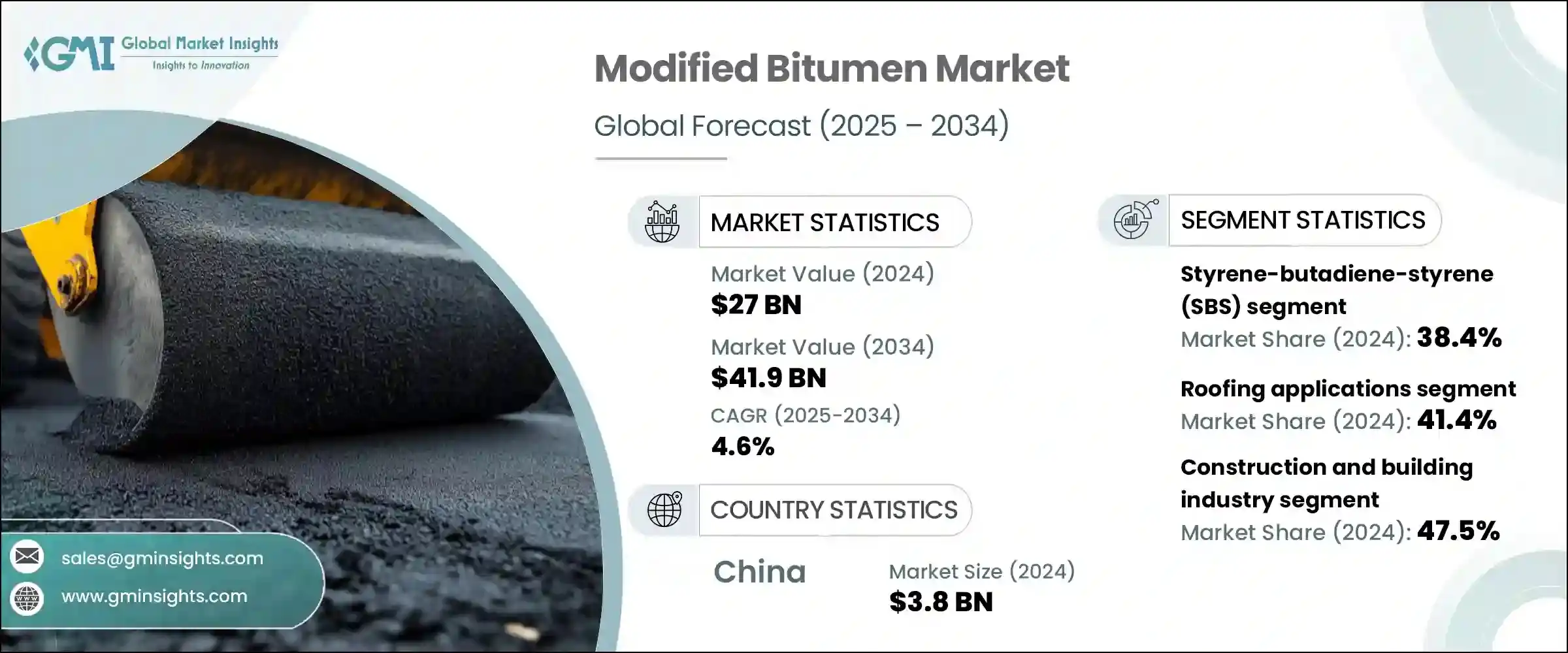

世界の改質アスファルト市場は2024年に270億米ドルと評価され、CAGR 4.6%で成長し、2034年には419億米ドルに達すると推定されています。

世界の建設セクターが屋根と舗装の両方で高性能で長持ちする材料に重点を移しているため、強化アスファルト配合の需要は着実に増加しています。過酷な環境条件に耐えられる道路やインフラの必要性が高まっていることが、弾力性と耐久性を向上させた改質バインダーの採用に拍車をかけています。また、気候への適応性が重視されるようになったことで、熱変動、ひび割れ、酸化に対する耐性に優れたアスファルトの使用も促されています。業界の事業者は、交通量の多い場所や厳しい気象条件下での性能要件を満たすため、ポリマー改質剤を選択するようになっています。さらに、持続可能なインフラ開発に対する意識の高まりは、環境基準に適合し、建設活動による二酸化炭素排出量を削減する材料を製造するよう、メーカーを駆り立てています。

世界各地の政府が意欲的なインフラ整備目標を掲げているため、精製業者やアスファルトメーカーは高性能グレードの生産能力を拡大する必要に迫られています。公共部門や民間部門のプロジェクトにおける材料の選択は、気候変動に配慮したエンジニアリング基準やライフサイクルコスト評価によってますます導かれるようになっています。改質アスファルトは、過酷な条件下でも性能を維持できることから、長期的な価値とメンテナンスの低減を求めるプロジェクトに好まれる選択肢となっています。バインダー化学の革新は、弾性の向上、優れた温度安定性、高い耐紫外線性を示すポリマー配合の開発に貢献しています。これらの特性は舗装や屋根の寿命を延ばし、インフラ投資の全体的なコスト効率に貢献します。その結果、この材料は、近代的で持続可能な建設手法への投資の高まりに支えられ、長期的な交通・都市開発計画に不可欠なものとなりつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 270億米ドル |

| 予測金額 | 419億米ドル |

| CAGR | 4.6% |

同市場の成長を支えているのは、排出量削減と建設投入資材の循環性促進を目的とした厳しい規制シフトでもあります。改質アスファルト再生ゴムや低排出ポリマーのような環境に配慮した材料を配合したブレンドは、政府がグリーンビルディング認証を施行し、気候変動に強い都市化を奨励する中で、支持を集めています。特に、ポリマーを改質したものは顕著で、性能と持続可能性の目標とのバランスが取れた選択肢に対する需要が急増しています。混合適合性、低温舗装ソリューション、炭素削減添加剤に焦点を当てた調査努力が続けられており、これらはすべて、材料選択における環境配慮の影響力の高まりを反映しています。このように進化する状況の中で、メーカーは高性能で環境に優しい配合を再構築することで対応し、持続可能性の枠組みに準拠しながら、より幅広いインフラのニーズに応えることを可能にしています。

市場で使用されている様々な改質剤の中で、スチレン-ブタジエン-スチレン(SBS)は、弾性、耐疲労性、温度耐性を向上させる能力があるため、引き続き優位を占めています。これらの特性により、SBS改質バインダーは、頻繁な温度変化や車両負荷の大きい過酷な環境に特に適しています。SBS改質バインダーは、変形やひび割れを抑えることで表面の耐久性を大幅に向上させ、最終的に道路や屋根システムの耐用年数を延ばします。SBSの機械的性能は、新築プロジェクトでも改修プロジェクトでも好まれる選択肢となっており、多様な地域市場においてSBSの存在感を高めています。

改質アスファルトは用途別に道路建設・舗装、ルーフィング、防水・シーリング、工業・特殊用途に区分されます。屋根材用途は、耐候性とエネルギー効率に優れた建材の需要増加に牽引され、2024年の世界市場シェアの41.4%を占めました。屋根膜にSBSとアタクチック・ポリプロピレン(APP)を使用することで、柔軟性と紫外線劣化への耐性が強化され、近代的な都市建築に理想的なものとなっています。特に急速な都市化が進む地域では、商業および住宅建設が着実に増加しており、屋根材がこうした先端素材へとシフトしています。断熱特性の向上と、より厳しい建築基準法への適合により、改質屋根膜は先進経済諸国でも新興経済諸国でも人気が高まっています。

製造技術も製品の品質と適応性に影響します。特に、粘度や弾力性といった特定の性能基準を満たす必要がある、カスタマイズされた量や配合の場合には、バッチプロセスが依然としてポリマー-改質アスファルトの製造に広く使用されています。この方法によって、生産者は様々な地域の要求や特殊なプロジェクトの要求に、より柔軟に対応することができます。特に研究開発用途や、配合調整が必要な少量生産プロジェクトに有益です。

アジア太平洋地域は、引き続き世界の改質アスファルト市場において主導的地位を占めており、その原動力となっているのは、堅調な建設活動、交通機関への投資拡大、都市拡大の進展です。同地域の国々は、インフラの改修や新規開発に多額の投資を行っており、性能改質表面処理材の安定した需要を牽引しています。同地域における市場の上昇の勢いは、政府の支援による取り組みや、大規模な輸送・住宅プロジェクトの増加によって強化されており、これらすべてが高品質で弾力性のある投入物に依存しています。

世界市場の主要プレーヤーには、シェル・世界、トタルエナジーズSE、エクソンモービル・コーポレーション、ナイナスAB、クレイトン・コーポレーションが含まれます。これらの企業は、さまざまな環境や交通条件に合わせて設計されたSBS、APP、およびハイブリッド変性製品の幅広いポートフォリオを通じて強い存在感を維持しています。製品の配合、技術サポート、供給の信頼性における専門知識により、これらの企業は大規模なインフラストラクチャーや産業プロジェクトで好まれるサプライヤーとなっています。これらの企業はまた、環境への影響を低減することを目的としたバイオベースの改質剤、再生材適合性、次世代バインダーの開発により、持続可能性へのシフトをリードしています。継続的な研究開発と低炭素イノベーションへの注力を通じて、これらの企業は、耐久性に優れ、気候変動に強い材料に対する世界の需要を満たしながら、改質アスファルト技術の未来を形成し続けています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- インフラ開発と都市化の進展

- 気候レジリエンスと異常気象への適応

- 持続可能性義務と環境規制

- パフォーマンスの向上とライフサイクルコストの最適化

- 業界の潜在的リスク&課題

- 初期費用が高く、経済的障壁が高い(60~70%のプレミアム)

- 保管安定性と取り扱いの複雑さ

- 熟練した設置作業員が限られている

- 原材料価格の変動とサプライチェーンの依存性

- 市場機会

- 新興市場とインフラ投資プログラム

- バイオベースとリサイクルポリマーの統合

- スマートインフラストラクチャとIoT統合

- 災害に強い建設要件

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:ポリマー改質剤の種類別、2021-2034

- 主要動向

- スチレン-ブタジエン-スチレン(SBS)改質アスファルト

- SBSポリマーのグレードと仕様

- アタクチックポリプロピレン(APP)改質アスファルト

- エチレン酢酸ビニル(EVA)改質アスファルト

- 熱可塑性エラストマー(TPE)およびその他の改質剤

- バイオベースおよびリサイクルポリマー改質剤

- ハイブリッドおよびマルチポリマーシステム

- SBS-APP複合製品

- ポリマーゴムハイブリッド改質

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 屋根材用途

- 低勾配および平らな屋根システム

- 商業および産業用建物への応用

- 多層システムの構成とパフォーマンス

- 急勾配屋根への適用

- 住宅屋根

- 下地材とICEのダム保護

- シングルとタイルの統合システム

- 低勾配および平らな屋根システム

- 道路建設と舗装

- 高速道路および州間高速道路のアプリケーション

- 都市および地方自治体の道路システム

- 市街地道路および幹線道路への応用

- 交差点および高応力ゾーンのソリューション

- メンテナンスおよびリハビリテーションプロジェクト

- 空港および産業用舗装

- 防水およびシーリング用途

- 地下防水システム

- ファンデーションおよび地下室のアプリケーション

- トンネルおよび地下構造物の保護

- 橋梁床版およびインフラの防水

- 地上防水ソリューション

- プラザデッキとバルコニーシステム

- 緑の屋根と庭園のアプリケーション

- 駐車場構造とポディウムデッキの保護

- 地下防水システム

- 産業および特殊用途

- 接着剤とシーラント

- コーティングと保護システム

- パイプコーティングと腐食防止

第7章 市場推計・予測:最終用途産業別、2021-2034

- 主要動向

- 建設・建築業界

- 住宅建設市場

- 一戸建て住宅と集合住宅

- 改修・改築プロジェクト

- エネルギー効率とグリーンビルディングの要件

- 商業建設セクター

- オフィスビルと小売センター

- ヘルスケア・教育施設

- ホスピタリティとエンターテイメント会場

- 産業建設アプリケーション

- 製造および加工施設

- 倉庫および配送センター

- データセンターとテクノロジーインフラストラクチャ

- 住宅建設市場

- 交通インフラ

- 高速道路と道路インフラ

- 州間高速道路システムの保守

- 州および地方の道路網

- 橋梁・高架建設

- 空港インフラ開発

- 滑走路およびターミナル拡張プロジェクト

- 貨物施設開発

- 港湾・海洋インフラ

- コンテナターミナルおよび埠頭建設

- 沿岸保護および防波堤プロジェクト

- 高速道路と道路インフラ

- エネルギーおよび公益事業セクター

- 発電施設

- 太陽光発電所と風力エネルギーインフラ

- 従来の発電所メンテナンス

- 石油・ガスインフラ

- 精製および処理施設アプリケーション

- パイプラインと貯蔵タンクの保護

- 水と廃水処理

- 治療施設インフラ

- 貯水池および貯蔵施設の防水

- 発電施設

- 政府と公共インフラ

- 連邦政府および州政府のプロジェクト

- 市町村および地方自治体向けアプリケーション

- 軍事および防衛インフラ

- プライベート市場と専門市場

- スポーツ・レクリエーション施設

- 農業および農村インフラ

- 鉱業および採掘産業

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- CertainTeed Corporation

- Colas Group

- Dynasol Group

- Ergon Inc.

- ExxonMobil Corporation

- Johns Manville

- Kraton Corporation

- LG Chem Ltd

- MBTechnology

- Nynas AB

- Polyglass U.S.A., Inc

- Shell Global

- Siplast(Icopal Group)

- TotalEnergies SE

- Versalis S.p.A

目次

The Global Modified Bitumen Market was valued at USD 27 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 41.9 billion by 2034. The demand for enhanced bitumen formulations is steadily rising as the construction sector worldwide shifts focus toward high-performance, long-lasting materials for both roofing and paving. The increasing necessity for roads and infrastructure that can withstand harsh environmental conditions has fueled the adoption of modified binders with improved resilience and durability. A growing emphasis on climate adaptability has also prompted the use of bitumen variants that offer better resistance to thermal fluctuations, cracking, and oxidation. Industry operators are increasingly selecting polymer-modified alternatives to meet the performance requirements of high-traffic areas and challenging weather zones. In addition, growing awareness around sustainable infrastructure development is motivating manufacturers to produce materials that align with environmental standards and reduce the carbon impact of construction activities.

Governments in many parts of the world are pursuing ambitious infrastructure goals, prompting refiners and bitumen producers to expand their capacity for high-performance grades. Material choices in public and private sector projects are increasingly guided by climate-conscious engineering standards and lifecycle cost assessments. Modified bitumen's capacity to retain performance under extreme conditions has made it a preferred option for projects demanding long-term value and lower maintenance. Innovations in binder chemistry have contributed to the development of polymer formulations that exhibit improved elasticity, superior temperature stability, and higher UV resistance. These characteristics extend the life of pavements and roofing systems and contribute to the overall cost-efficiency of infrastructure investments. As a result, the material is becoming integral to long-term transportation and urban development plans, supported by rising investment in modern, sustainable construction practices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27 Billion |

| Forecast Value | $41.9 Billion |

| CAGR | 4.6% |

The market's growth is also supported by stringent regulatory shifts aimed at reducing emissions and promoting circularity in construction inputs. Modified bitumen blends incorporating eco-conscious materials-such as recycled rubber or low-emission polymers-are gaining traction as governments enforce green building certifications and encourage climate-resilient urbanization. Polymer-modified variants are especially prominent, with demand surging for options that balance performance with sustainability goals. Research efforts continue to focus on blending compatibility, low-temperature paving solutions, and carbon-reducing additives, all of which reflect the growing influence of environmental considerations on material selection. In this evolving landscape, manufacturers are responding by reengineering formulations that are both high performing and eco-friendly, allowing them to cater to a broader range of infrastructure needs while complying with sustainability frameworks.

Among the various modifiers used in the market, Styrene-Butadiene-Styrene (SBS) continues to dominate due to its ability to enhance elasticity, fatigue resistance, and temperature tolerance. These properties make SBS-modified binders particularly suitable for demanding environments with frequent temperature changes or heavy vehicular load. SBS modifications significantly improve surface durability by reducing deformation and cracking, ultimately extending the service life of roads and roofing systems. Its mechanical performance makes it a preferred choice in both new construction and rehabilitation projects, which helps explain its strong presence across diverse regional markets.

Modified bitumen is segmented by application into road construction and paving, roofing, waterproofing and sealing, and industrial and specialty uses. Roofing applications accounted for 41.4% of the global market share in 2024, driven by increasing demand for weather-resistant and energy-efficient building materials. The use of SBS and Atactic Polypropylene (APP) in roofing membranes enhances flexibility and resistance to UV degradation, making them ideal for modern urban buildings. The steady rise in commercial and residential construction, especially in regions undergoing rapid urbanization, has supported the shift toward these advanced materials in roofing systems. Enhanced insulation properties and compliance with stricter building codes have made modified roofing membranes increasingly popular in both developed and developing economies.

Manufacturing techniques also influence product quality and adaptability. The batch process remains widely used for producing polymer-modified bitumen, particularly for customized volumes or formulations where specific performance criteria-such as viscosity or elasticity-must be met. This method allows producers to respond to varying regional requirements and specialty project demands with more flexibility. It is especially beneficial for R&D applications or lower-volume projects where formulation adjustments are necessary.

Asia Pacific continues to hold a leading position in the global modified bitumen market, driven by robust construction activity, growing investments in transportation, and rising urban expansion. Countries across the region are investing heavily in infrastructure upgrades and new development, driving consistent demand for performance-modified surfacing materials. The market's upward momentum in the region is reinforced by government-backed initiatives and a growing number of large-scale transport and housing projects, all of which rely on high-quality, resilient inputs.

Key players in the global market include Shell Global, TotalEnergies SE, ExxonMobil Corporation, Nynas AB, and Kraton Corporation. These companies maintain a strong presence through a wide-ranging portfolio of SBS, APP, and hybrid-modified products designed for varying environmental and traffic conditions. Their expertise in product formulation, technical support, and supply reliability positions them as preferred suppliers for large infrastructure and industrial projects. These firms are also leading the shift toward sustainability by developing bio-based modifiers, recycled content compatibility, and next-generation binders aimed at reducing environmental impact. Through ongoing R&D and a focus on low-carbon innovations, these companies continue to shape the future of modified bitumen technologies while meeting global demand for durable, climate-resilient materials.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Polymer modified type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Infrastructure development and urbanization growth

- 3.2.1.2 Climate resilience and extreme weather adaptation

- 3.2.1.3 Sustainability mandates and environmental regulations

- 3.2.1.4 Performance enhancement and lifecycle cost optimization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial costs and economic barriers (60-70% premium)

- 3.2.2.2 Storage stability and handling complexities

- 3.2.2.3 Limited skilled installation workforce

- 3.2.2.4 Raw material price volatility and supply chain dependencies

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets and infrastructure investment programs

- 3.2.3.2 Bio-based and recycled polymer integration

- 3.2.3.3 Smart infrastructure and IoT integration

- 3.2.3.4 Disaster-resilient construction requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Polymer Modifier Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Styrene-butadiene-styrene (SBS) modified bitumen

- 5.2.1 SBS polymer grades and specifications

- 5.3 Atactic polypropylene (APP) modified bitumen

- 5.4 Ethylene vinyl acetate (EVA) modified bitumen

- 5.5 Thermoplastic elastomers (TPE) and other modifiers

- 5.6 Bio-based and recycled polymer Modifiers

- 5.7 Hybrid and multi-polymer systems

- 5.7.1 SBS-APP combination products

- 5.7.2 Polymer-rubber hybrid modifications

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Roofing applications

- 6.2.1 Low-slope and flat roofing systems

- 6.2.1.1 Commercial and industrial building applications

- 6.2.1.2 Multi-ply system configurations and performance

- 6.2.2 Steep-slope roofing applications

- 6.2.2.1 Residential roofing

- 6.2.2.2 Underlayment and ice dam protection

- 6.2.2.3 Shingle and tile integration systems

- 6.2.1 Low-slope and flat roofing systems

- 6.3 Road construction and paving

- 6.3.1 Highway and interstate applications

- 6.3.2 Urban and municipal road systems

- 6.3.2.1 City street and arterial applications

- 6.3.2.2 Intersection and high-stress zone solutions

- 6.3.2.3 Maintenance and rehabilitation projects

- 6.3.3 Airport and industrial paving

- 6.4 Waterproofing and sealing applications

- 6.4.1 Below-grade waterproofing systems

- 6.4.1.1 Foundation and basement applications

- 6.4.1.2 Tunnel and underground structure protection

- 6.4.1.3 Bridge deck and infrastructure waterproofing

- 6.4.2 Above-grade waterproofing solutions

- 6.4.2.1 Plaza deck and balcony systems

- 6.4.2.2 Green roof and garden applications

- 6.4.2.3 Parking structure and podium deck protection

- 6.4.1 Below-grade waterproofing systems

- 6.5 Industrial and specialty applications

- 6.5.1 Adhesives and sealants

- 6.5.2 Coatings and protective systems

- 6.5.3 Pipe coating and corrosion protection

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Construction and Building Industry

- 7.2.1 Residential Construction Market

- 7.2.1.1 Single-Family and Multi-Family Housing

- 7.2.1.2 Renovation and Retrofit Projects

- 7.2.1.3 Energy Efficiency and Green Building Requirements

- 7.2.2 Commercial Construction Sector

- 7.2.2.1 Office Buildings and Retail Centers

- 7.2.2.2 Healthcare and Educational Facilities

- 7.2.2.3 Hospitality and Entertainment Venues

- 7.2.3 Industrial Construction Applications

- 7.2.3.1 Manufacturing and Processing Facilities

- 7.2.3.2 Warehousing and Distribution Centers

- 7.2.3.3 Data Centers and Technology Infrastructure

- 7.2.1 Residential Construction Market

- 7.3 Transportation Infrastructure

- 7.3.1 Highway and Road Infrastructure

- 7.3.1.1 Interstate Highway System Maintenance

- 7.3.1.2 State and Local Road Networks

- 7.3.1.3 Bridge and Overpass Construction

- 7.3.2 Airport Infrastructure Development

- 7.3.2.1 Runway and Terminal Expansion Projects

- 7.3.2.2 Cargo and Freight Facility Development

- 7.3.3 Port and Marine Infrastructure

- 7.3.3.1 Container Terminal and Wharf Construction

- 7.3.3.2 Coastal Protection and Seawall Projects

- 7.3.1 Highway and Road Infrastructure

- 7.4 Energy and Utilities Sector

- 7.4.1 Power Generation Facilities

- 7.4.1.1 Solar Farm and Wind Energy Infrastructure

- 7.4.1.2 Traditional Power Plant Maintenance

- 7.4.2 Oil and Gas Infrastructure

- 7.4.2.1 Refinery and Processing Facility Applications

- 7.4.2.2 Pipeline and Storage Tank Protection

- 7.4.3 Water and Wastewater Treatment

- 7.4.3.1 Treatment Plant Infrastructure

- 7.4.3.2 Reservoir and Storage Facility Waterproofing

- 7.4.1 Power Generation Facilities

- 7.5 Government and Public Infrastructure

- 7.5.1 Federal and State Government Projects

- 7.5.2 Municipal and Local Government Applications

- 7.5.3 Military and Defense Infrastructure

- 7.6 Private and Specialty Markets

- 7.6.1 Sports and Recreation Facilities

- 7.6.2 Agricultural and Rural Infrastructure

- 7.6.3 Mining and Extractive Industries

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 CertainTeed Corporation

- 9.2 Colas Group

- 9.3 Dynasol Group

- 9.4 Ergon Inc.

- 9.5 ExxonMobil Corporation

- 9.6 Johns Manville

- 9.7 Kraton Corporation

- 9.8 LG Chem Ltd

- 9.9 MBTechnology

- 9.10 Nynas AB

- 9.11 Polyglass U.S.A., Inc

- 9.12 Shell Global

- 9.13 Siplast (Icopal Group)

- 9.14 TotalEnergies SE

- 9.15 Versalis S.p.A

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日