|

市場調査レポート

商品コード

1637749

ビチューメン-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Bitumen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ビチューメン-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

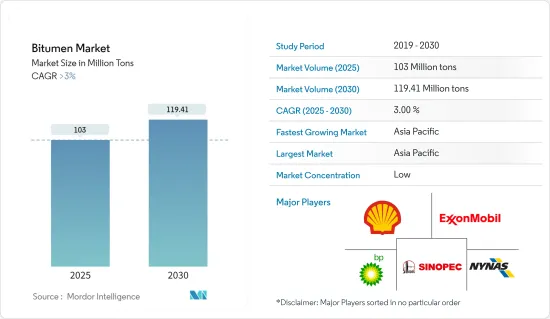

ビチューメン市場規模は2025年に1億300万トンと推定され、予測期間(2025~2030年)のCAGRは3%を超え、2030年には1億1,941万トンに達すると予測されます。

COVID-19は世界市場のビチューメン需要に悪影響を与えました。COVID-19の間、多くの建設プロジェクトが中断され、世界中でビチューメンの使用が減少しました。しかし、操業停止や規制が緩和されると、主要地域では建設活動が継続されました。それ以来、市場は順調に成長しています。

主要ハイライト

- ビチューメン市場の成長を牽引しているのは、道路建設と補修活動の増加、充填材、接着剤、シーリング材としてのビチューメンに対する商業と国内建築部門からの需要の増大です。

- その反面、有害な大気排出物を発生させるビチューメンの利用など、環境に対する懸念の高まりが市場の成長を妨げています。

- 高性能ビチューメン製品や道路インフラの開発を改善するためのビチューメン加工に関する研究開発は、今後数年間、ビチューメン市場にさまざまな機会を生み出すと予想されます。

- アジア太平洋はビチューメン市場で大きなシェアを占め、予測期間中に最も高いCAGRで推移すると予想されます。

ビチューメン市場の動向

市場を独占する道路建設セグメント

- 道路建設産業は、世界的にビチューメンの最大消費者の一つであり、ビチューメンの総消費量のかなりの部分を占めています。道路、高速道路、その他の交通インフラの舗装に必要なビチューメンの量が多いことが、同市場における優位性の一因となっています。

- ビチューメンをベースとしたビチューメン舗装は、耐久性、柔軟性、耐候性に優れており、道路建設プロジェクトに適しています。ビチューメン道路は、重い交通荷重、さまざまな気象条件、その他の環境要因に耐えることができ、長期的な性能と費用対効果を保証します。

- FMI Corporation(コンサルティングと投資銀行)によると、北米のエンジニアリングと建設支出は、2024年末までに2%増加すると予想されています。

- さらに、米国国勢調査局が発表したデータによると、米国における輸送のための民間建設額は2020年に163億1,000万米ドル増加し、2023年には193億9,000万米ドルに達します。

- 新興経済諸国であるアジア太平洋では、都市化の進展や、伝統的セグメントから新興の第二次産業へのシフトにより、インフラプロジェクト、特に運輸部門が大幅に増加すると予想されます。加えて、経済繁栄の拡大が、輸送や製造といった、原料を供給し消費者に販売する消費セクターへのインフラ融資を促進しています。

- 中国国家建設プロセス総公司(CSCEC)は、2020年の4,186kmから、2022年には合計4,623kmの新規道路建設に調印しました。この動向もビチューメン市場を支えています。

- NIPの下、インドはインフラ整備に1億米ドルの投資予算を割り当てた。インドは、デリー・ムンバイ間産業回廊、アムリトサル・コルカタ間産業回廊、バイザッグ・チェンナイ間産業回廊、ベンガルール・チェンナイ間産業回廊、ベンガルール・ムンバイ間産業回廊など、複数の産業回廊を開発するための予算を可決しました。これらのプロジェクトは2025年3月までに完成する予定であり、今後数年間でビチューメンの需要が増加すると予想されます。

- これらすべての要因により、ビチューメン市場は予測期間中に世界的に成長する可能性が高いです。

アジア太平洋が市場を独占する

- インド、中国、その他の東南アジア諸国などの様々な国々における急速な工業化と都市化は、道路、高速道路、空港、港湾などのインフラプロジェクトへの大規模な投資につながり、ビチューメンの需要を促進しています。

- アジア太平洋の建設セクターはビチューメンの最大消費者のひとつであり、進行中の住宅、商業、工業建設プロジェクトが、道路舗装、屋根、防水用のビチューメンなどのビチューメン系材料の需要を煽っています。

- 中国の次期第15次5ヵ年計画では、交通、エネルギー、水システム、都市開発における新しいインフラプロジェクトに重点が置かれています。第1弾には、中国東北部や北京・天津・河北地域における高規格農地の建設を含む、約2,900のプロジェクトが含まれています。

- インドでは、India Brand Equity Foundation(IBEF)が発表したデータによると、2,000年4月から2023年3月までの間に、住宅、インフラ、建設開発プロジェクトなど建設開発への外国直接投資(FDI)は263億5,000万米ドルに上った。

- インドで今後予定されているプロジェクトで、ビチューメンの需要を増やすと想定されるものには、デリー・ムンバイ間産業回廊、バラットマラプロジェクト、グジャラート国際金融技術都市(GIFT)、スマートシティ高知、ナビ・ムンバイ国際空港などがあります。

- 国家投資促進・円滑化庁(National Investment Promotion and Facilitation Agency)が発表したデータによると、インドは2024年度のインフラ整備に1兆4,000億米ドルの予算を割り当てています。このうち再生可能エネルギーが24%、道路・高速道路が18%、都市インフラが17%、鉄道が12%となっています。

- 上記の要因により、予測期間中、アジア太平洋におけるビチューメンの需要は増加すると予想されます。

ビチューメン産業概要

ビチューメン市場はセグメント化されており、圧倒的なシェアを持つ大手企業は存在しないです。主要参入企業(順不同)には、ExxonMobil、Shell、BP PLC、NYNAS AB、China Petroleum & Chemical Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 道路建設と補修活動の増加

- 商業ビルと国内ビル建設による需要

- 抑制要因

- 環境への懸念

- その他の抑制要因

- 産業のバリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 原料分析

第5章 市場セグメンテーション(市場規模(数量))

- 製品タイプ別

- 舗装グレード

- 硬質グレード

- 酸化グレード

- ビチューメンエマルジョン

- ポリマー改質ビチューメン

- その他の製品タイプ(乳化タイプ)

- 用途別

- 道路建設

- 防水

- 接着剤

- その他の用途(工業用塗料)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- インドネシア

- タイ

- マレーシア

- ベトナム

- ASEAN諸国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- ロシア

- スペイン

- トルコ

- ノルディック

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BMI Group(Icopal Enterprise ApS)

- Bouygues Group

- BP PLC

- China Petroleum & Chemical Corporation

- ENEOS Corporation(JXTG Nippon Oil & Energy Corporation)

- Exxon Mobil Corporation

- Indian Oil Corporation Ltd

- Kraton Corporation

- Marathon Oil Company(Marathon Petroleum LP)

- NYNAS AB

- Shell

- Suncor Energy Inc.

第7章 市場機会と今後の動向

- 道路インフラ改善のためのビチューメン加工に関する研究開発

- 高性能ビチューメン製品の開発

The Bitumen Market size is estimated at 103 million tons in 2025, and is expected to reach 119.41 million tons by 2030, at a CAGR of greater than 3% during the forecast period (2025-2030).

COVID-19 adversely influenced the demand for bitumen on the global market. During COVID-19, a large number of construction projects were on hold, reducing the use of bitumen throughout the world. However, as lockdowns and restrictions eased, there was continued construction activity in major regions. Since then, the market has been growing steadily.

Key Highlights

- The growth of the bitumen market is driven by increased road construction and repair activities, as well as a growing demand from both commercial and domestic building sectors for bitumen as fillers, adhesives, or sealants.

- On the flip side, increasing environmental concerns, such as the utilization of bitumen, which generates several harmful atmospheric emissions, have been hindering the market's growth.

- Research and development on bitumen processing to improve the development of high-performance bitumen products and road infrastructure are expected to create various opportunities for the bitumen market in the upcoming years.

- Asia-Pacific is expected to hold a significant share of the bitumen market and witness the highest CAGR during the forecast period.

Bitumen Market Trends

Road Construction Segment to Dominate the Market

- The road construction industry is one of the largest consumers of bitumen globally, accounting for a significant portion of total bitumen consumption. The sheer volume of bitumen required for paving roads, highways, and other transportation infrastructure contributes to its dominance in the market.

- Bitumen-based asphalt pavements offer excellent durability, flexibility, and resistance to weathering, making them well-suited for road construction projects. Asphalt roads can withstand heavy traffic loads, varying weather conditions, and other environmental factors, ensuring long-term performance and cost-effectiveness.

- According to the FMI Corporation (a consulting and investment bank), engineering and construction spending in North America is expected to increase by 2% by the end of 2024.

- Moreover, according to the data released by the United States Census Bureau, the value of private construction for transportation in the United States increased by USD 16.31 billion in 2020 to USD 19.39 billion in 2023.

- Infrastructure projects are expected to increase significantly in developing Asia-Pacific economies, particularly the transport sector, due to increased urbanization and shifting focus from traditional sectors toward emerging secondary industries. In addition, the growing economic prosperity is driving infrastructure financing toward consumer sectors such as transport and manufacturing, where raw materials are provided and sold to consumers.

- The China State Construction Engineering Corporation (CSCEC) signed a total of 4,623 kilometers of new road construction in 2022, up from 4,186 kilometers in 2020. This trend also supports the bitumen market.

- Under NIP, India allocated an investment budget of ~USD 1000 million for infrastructure. India passed a budget to develop several industrial corridors, including the Delhi-Mumbai Industrial Corridor, Amritsar-Kolkata Industrial Corridor, Vizag-Chennai Industrial Corridor, Bengaluru-Chennai Industrial Corridor, and the Bengaluru-Mumbai Industrial Corridor. These projects are expected to be completed by March 2025, which is expected to increase the demand for bitumen in the coming years.

- Owing to all these factors, the bitumen market is likely to grow globally during the forecast period.

Asia-Pacific to Dominate the Market

- The rapid industrialization and urbanization in various countries such as India, China, and other Southeast Asian nations have led to significant investments in infrastructure projects, including roads, highways, airports, and ports, driving the demand for bitumen.

- The construction sector in Asia-Pacific is one of the largest consumers of bitumen, with ongoing residential, commercial, and industrial construction projects fueling the demand for bitumen-based materials such as asphalt for road paving, roofing, and waterproofing.

- China's upcoming 15th Five-Year Plan focuses on new infrastructure projects in transport, energy, water systems, and urban development. The first batch includes about 2,900 projects, including the construction of high-standard farmland in northeast China and the Beijing-Tianjin-Hebei region.

- In India, according to the data published by the Indian Brand Equity Foundation (IBEF), foreign direct investment (FDI) in construction development, such as housing, infrastructure, and construction development projects, was valued at USD 26.35 billion between April 2000 and March 2023.

- The upcoming projects in India that are assumable to increase the demand for bitumen include the Delhi-Mumbai Industrial Corridor, Bharatmala Project, Gujarat International Finance Tec-City (GIFT), Smart City Kochi, and Navi Mumbai International Airport.

- According to the data published by the National Investment Promotion and Facilitation Agency, India has allocated a budget of USD 1.4 trillion for infrastructure for FY 2024. Of this, 24% is for renewable energy, 18% is for roads and highways, 17% is for urban infrastructure, and 12% is for railways.

- The factors mentioned above are expected to increase the demand for bitumen in Asia-Pacific during the forecast period.

Bitumen Industry Overview

The bitumen market is fragmented, with no major players having a dominant share. Some of the major players (not in any particular order) include Exxon Mobil Corporation, Shell, BP PLC, NYNAS AB, and China Petroleum & Chemical Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Road Construction and Repair Activities

- 4.1.2 Demand from Commercial and Domestic Building Constructions

- 4.2 Restraints

- 4.2.1 Environmental Concerns

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Feedstock Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Product Type

- 5.1.1 Paving Grade

- 5.1.2 Hard Grade

- 5.1.3 Oxidized Grade

- 5.1.4 Bitumen Emulsions

- 5.1.5 Polymer Modified Bitumen

- 5.1.6 Other Product Types (Emulsified)

- 5.2 By Application

- 5.2.1 Road Construction

- 5.2.2 Waterproofing

- 5.2.3 Adhesives

- 5.2.4 Other Applications (Industrial Coatings)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Thailand

- 5.3.1.7 Malaysia

- 5.3.1.8 Vietnam

- 5.3.1.9 ASEAN Countries

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 Turkey

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombian

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BMI Group (Icopal Enterprise ApS)

- 6.4.2 Bouygues Group

- 6.4.3 BP PLC

- 6.4.4 China Petroleum & Chemical Corporation

- 6.4.5 ENEOS Corporation (JXTG Nippon Oil & Energy Corporation)

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 Indian Oil Corporation Ltd

- 6.4.8 Kraton Corporation

- 6.4.9 Marathon Oil Company (Marathon Petroleum LP)

- 6.4.10 NYNAS AB

- 6.4.11 Shell

- 6.4.12 Suncor Energy Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Research and Development on Bitumen Processing to Improve Road Infrastructure

- 7.2 Development of High-Performance Bitumen Products