ワイヤレスEV充電の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Wireless EV Charging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 121 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773460

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

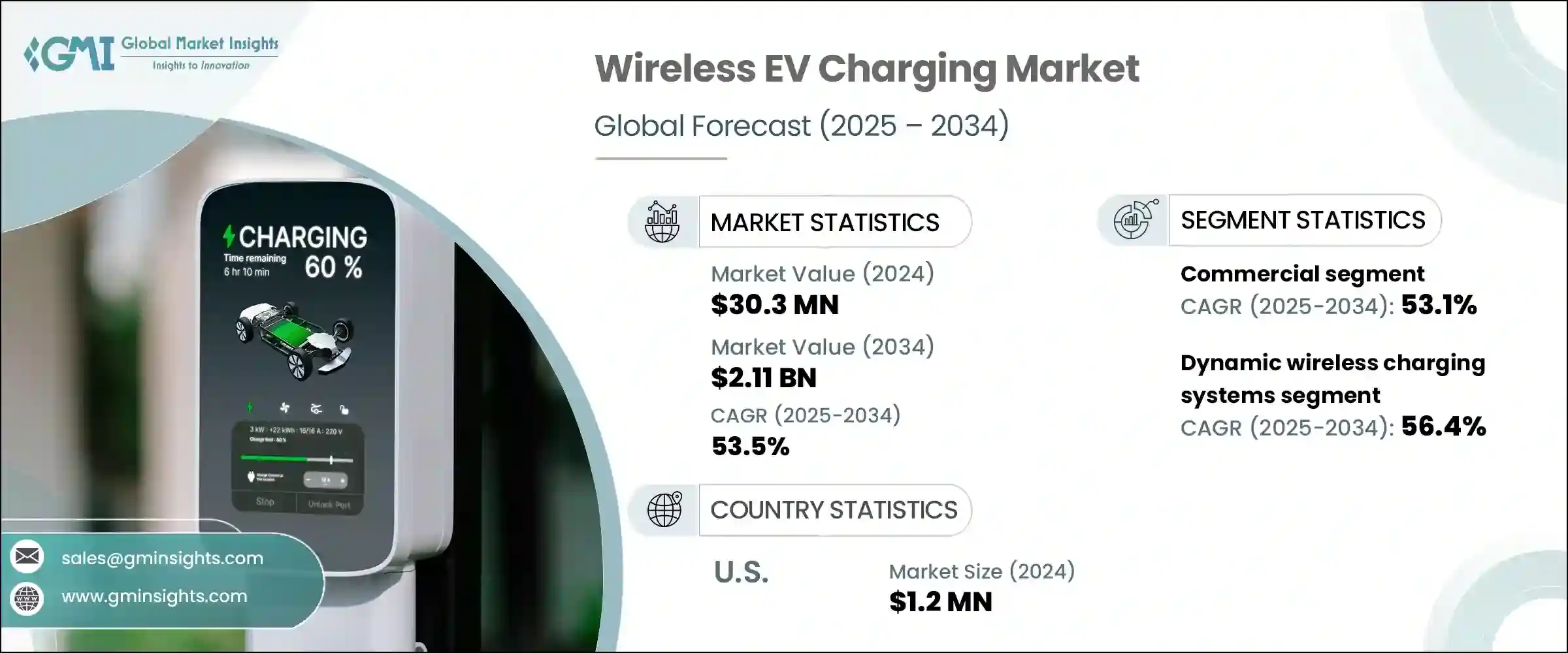

ワイヤレスEV充電の世界市場は、2024年に3,030万米ドルと評価され、CAGR 53.5%で成長し、2034年には21億1,000万米ドルに達すると推定されています。

この急成長の主な要因は、より便利でメンテナンスの少ない充電ソリューションに対する需要の高まりと相まって、輸送車両の電動化が進んでいることです。持続可能な交通機関への世界のシフトが勢いを増すにつれ、シームレスでハンズフリーの充電システムの必要性がより明白になってきています。特に都市インフラは、こうしたイノベーションをサポートするために進化しており、都市計画担当者やモビリティ利害関係者は、従来のプラグイン・ステーションへの依存を減らすために、ワイヤレス技術をますます好むようになっています。

電気自動車の普及は先進経済諸国と新興経済諸国の双方で加速しており、ケーブルレスで手間のかからない充電によってユーザー体験を向上させることに、より大きな注目が集まっています。この動向は、ワイヤレスEV充電システムへの関心の高まりに大きく寄与しています。自動車メーカー、インフラ公開会社、公益事業者が戦略を調整し続ける中、公共空間と非公開空間の両方にワイヤレス技術を統合することが現実味を帯びてきています。このような協力関係により、相互運用可能な充電ソリューションの開発も急ピッチで進められており、これは統一的で拡張性のあるEVエコシステムの構築に不可欠です。その結果、ワイヤレス充電システムは、その利便性だけでなく、充電時間を短縮し、電気自動車の運行効率を高める可能性からも支持を集めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 3,030万米ドル |

| 予測金額 | 21億1,000万米ドル |

| CAGR | 53.5% |

ワイヤレスEV充電市場は、最終用途に基づいて商業用セグメントと住宅用セグメントに分類されます。商業セグメントは、2025年から2034年にかけてCAGR 53.1%で成長すると予測されます。この成長の主な要因は、交通通路、物流ハブ、公共交通ルートにおけるワイヤレス充電技術の導入が増加していることです。電気自動車を採用する企業や自治体が増えるにつれ、効率的で手間のかからない充電システムの必要性が不可欠になっています。ワイヤレス・インフラは、ダウンタイムを削減し、手動による介入を必要とせずに車両を確実に稼働させることで、効果的なソリューションを提供します。これは、時間にシビアな配送や輸送サービスにおいて、車両を中断することなく利用することが求められる商業用途において特に有益です。

充電タイプの観点から、市場は据置型とダイナミック・ワイヤレス充電システムに区分されます。ダイナミック・ワイヤレス充電分野は、2025年から2034年にかけてCAGR 56.4%で成長すると予測されています。この急成長を支えているのは、走行中の車両向けに継続的な電力供給ソリューションを開発する取り組みが増加していることです。ダイナミック・システムは、高速道路や貨物用途に大きな利点を提供し、車両が専用の充電ステーションに停車することなく、移動中に電力を受け取ることを可能にします。このリアルタイム充電機能は、電気トラック、バス、配送車の航続距離と運行効率を向上させることができ、車両運行会社や交通計画者にとって魅力的な選択肢となります。

米国では、ワイヤレスEV充電市場は着実な成長を示しており、評価額は2022年の50万米ドルから2023年には80万米ドル、さらに2024年には120万米ドルまで上昇しています。同地域は、2024年の世界市場で4%のシェアを占めています。電力網の近代化と車両統合機能の強化を目的とした政府の取り組みが、この拡大を促進する上で重要な役割を果たしています。連邦政府の投資は、ワイヤレス充電技術の研究開発を支援し、車両電化のための大規模なパイロットプログラムを奨励しています。米国は、エネルギー効率を改善し、二酸化炭素排出量を削減し、送電網の回復力を強化することを目標とした戦略により、ワイヤレス充電技術革新のリーダーとしての地位を確立しつつあります。

ワイヤレスEV充電業界の主要企業は、事業を拡大するための戦略的措置を講じています。これには、複数の車種に適応可能なモジュール式充電プラットフォームに注力することや、標準化された交換可能な部品を利用することで生産コストを最適化することなどが含まれます。相互運用性を重視することで、ワイヤレス・システムがさまざまな電気自動車とシームレスに動作することが保証され、これは商業的な実行可能性にとって不可欠です。

さらに、各社は自動車メーカーとの共同開発プロジェクトに取り組み、新車と既存車の両方との互換性を確保しながら、後付け可能なソリューションを開発しています。公共機関やスマートシティ開発業者との長期的な協力関係も、ワイヤレス充電ネットワークの普及に重要な役割を果たしています。知的財産ポートフォリオを強化することで、これらのプレーヤーは市場での地位を守り、今後数年間の持続的なイノベーションと成長の舞台を整えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:最終用途別、2021-2034

- 主要動向

- 商業用

- 住宅用

第6章 市場規模・予測:充電タイプ別、2021-2034

- 主要動向

- ダイナミックワイヤレス充電システム

- 据置型ワイヤレス充電システム

第7章 市場規模・予測:推進方式別、2021-2034

- バッテリーEV

- プラグインハイブリッドEV

第8章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ノルウェー

- ドイツ

- フランス

- 英国

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- 世界のその他の地域

第9章 企業プロファイル

- Continental

- Electreon

- Elix Wireless

- ENRX

- Evatran Group

- HEVO

- InductEV

- Lumen Australia

- Momentum Dynamics

- Plugless Power

- Qualcomm

- Siemens

- Toshiba Corporation

- Wave Charging

- Wiferion

- WiTricity Corporation

- ZTE Corporation

目次

The Global Wireless EV Charging Market was valued at USD 30.3 million in 2024 and is estimated to grow at a CAGR of 53.5% to reach USD 2.11 billion by 2034. This rapid growth is primarily fueled by the increasing electrification of transportation fleets, coupled with rising demand for more convenient and low-maintenance charging solutions. As the global shift toward sustainable transportation gains momentum, the need for seamless, hands-free charging systems is becoming more evident. Urban infrastructure, in particular, is evolving to support these innovations, with city planners and mobility stakeholders increasingly favoring wireless technologies to reduce reliance on conventional plug-in stations.

The adoption of electric vehicles is accelerating across both developed and emerging economies, leading to a broader focus on enhancing user experience with cable-free, hassle-free charging. This trend is contributing significantly to the growing interest in wireless EV charging systems. As vehicle manufacturers, infrastructure companies, and utilities continue aligning their strategies, the integration of wireless technologies into both public and private spaces is becoming a practical reality. These collaborations are also fast-tracking the development of interoperable charging solutions, which are crucial for creating a unified and scalable EV ecosystem. As a result, wireless charging systems are gaining traction not only for their convenience but also for their potential to reduce charging time and increase operational efficiency for electric fleets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $30.3 Million |

| Forecast Value | $2.11 Billion |

| CAGR | 53.5% |

Based on end use, the wireless EV charging market is categorized into commercial and residential segments. The commercial segment is expected to grow at a CAGR of 53.1% from 2025 to 2034. This growth is largely attributed to the increased deployment of wireless charging technologies in transportation corridors, logistics hubs, and public transit routes. As more businesses and municipalities adopt electric fleets, the need for efficient, low-touch charging systems becomes essential. Wireless infrastructure offers an effective solution by reducing downtime and ensuring that vehicles remain operational without the need for manual intervention. This is particularly beneficial in commercial applications where time-sensitive delivery and transit services demand uninterrupted vehicle availability.

In terms of charging type, the market is segmented into stationary and dynamic wireless charging systems. The dynamic wireless charging segment is forecast to grow at a CAGR of 56.4% between 2025 and 2034. This surge in growth is supported by increasing efforts to develop continuous power delivery solutions for vehicles in motion. Dynamic systems offer significant advantages for highway and freight applications, allowing vehicles to receive power on the go without having to stop at dedicated charging stations. This real-time charging capability can improve the range and operational efficiency of electric trucks, buses, and delivery vehicles, making it an appealing option for fleet operators and transportation planners alike.

In the United States, the wireless EV charging market has shown steady growth, with valuations rising from USD 500 thousand in 2022 to USD 800 thousand in 2023 and further to USD 1.2 million in 2024. The region accounted for a 4% share of the global market in 2024. Government initiatives aimed at modernizing the electric grid and enhancing vehicle integration capabilities are playing a key role in driving this expansion. Federal investments are supporting research and development in wireless charging technologies and encouraging large-scale pilot programs for fleet electrification. The US is positioning itself as a leader in wireless charging innovation, with targeted strategies to improve energy efficiency, reduce carbon emissions, and strengthen grid resilience.

Leading companies in the wireless EV charging industry are taking strategic steps to scale up their operations. These include focusing on modular charging platforms that can be adapted across multiple vehicle types and optimizing production costs by utilizing standardized, interchangeable components. The emphasis on interoperability ensures that wireless systems can work seamlessly with a wide range of electric vehicles, which is vital for commercial viability.

Additionally, companies are engaging in co-development projects with automakers to create retrofit-ready solutions, ensuring compatibility with both new and existing vehicles. Long-term collaborations with public agencies and smart city developers are also playing a critical role in expanding the reach of wireless charging networks. By reinforcing their intellectual property portfolios, these players are safeguarding their market positions and setting the stage for sustained innovation and growth in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Commercial

- 5.3 Residential

Chapter 6 Market Size and Forecast, By Charging Type, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Dynamic wireless charging systems

- 6.3 Stationary wireless charging systems

Chapter 7 Market Size and Forecast, By Propulsion Type, 2021 - 2034 (USD Million)

- 7.1 Battery EV

- 7.2 Plug-in hybrid EV

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & MT)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Norway

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 UK

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.5 Rest of World

Chapter 9 Company Profiles

- 9.1 Continental

- 9.2 Electreon

- 9.3 Elix Wireless

- 9.4 ENRX

- 9.5 Evatran Group

- 9.6 HEVO

- 9.7 InductEV

- 9.8 Lumen Australia

- 9.9 Momentum Dynamics

- 9.10 Plugless Power

- 9.11 Qualcomm

- 9.12 Siemens

- 9.13 Toshiba Corporation

- 9.14 Wave Charging

- 9.15 Wiferion

- 9.16 WiTricity Corporation

- 9.17 ZTE Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 121 Pages

- 納期

- 2~3営業日