|

市場調査レポート

商品コード

1773457

太陽光発電封止材市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Solar Encapsulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 太陽光発電封止材市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月27日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

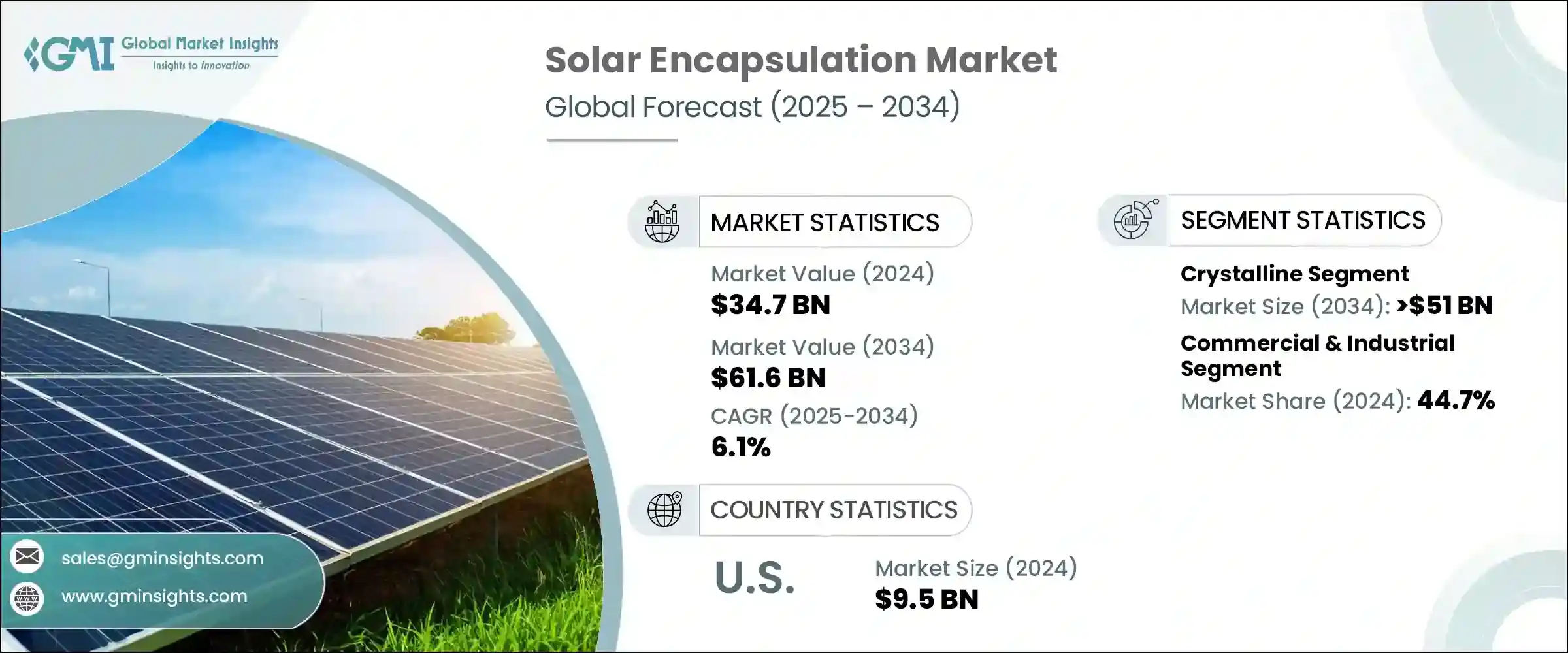

世界の太陽光発電封止材市場は、2024年に347億米ドルと評価され、CAGR 6.1%で成長し、2034年には616億米ドルに達すると推定されています。

この上昇傾向は、政府の好意的な政策に支えられた、国内でのソーラー製造への世界の軸足によるところが大きいです。世界各国は、輸入太陽光発電部品への依存を減らすために奨励金ベースの枠組みを導入しており、それによって封止材などの重要材料の国内生産を強化しています。これらの材料は、太陽電池を環境暴露から守り、パネルの寿命を延ばし、全体的な性能を高める上で重要な役割を果たしています。住宅、商業施設、公共施設規模のプロジェクトで太陽光発電の導入が進むにつれ、信頼性が高く高品質な封止材の必要性は、既存の太陽光発電経済圏でも新興経済圏でもますます高まっています。

特にソーラーモジュールの生産が急拡大している市場では、メーカー各社が急増する需要に対応するために事業を拡大しています。先進国も新興諸国も、サプライチェーンの合理化に重点を置きながら、ソーラーモジュールの現地生産を支援するインフラに多額の投資を行っています。このシフトは、モジュールの長期的な効率と耐久性を確保するための鍵となる封止材料の消費量の大幅な増加を促しています。この動向は、大規模生産のために封止材への確実なアクセスを必要とする垂直統合型ソーラー企業の増加によってさらに強化されています。こうした企業が原材料の調達やモジュールの組み立てを含むバリューチェーンの管理を強化するにつれて、安定した一貫性のある封止材供給に対する需要が高まり、今後数年間の市場力学にプラスの影響を与えると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 347億米ドル |

| 予測金額 | 616億米ドル |

| CAGR | 6.1% |

結晶系パネル・セグメントは、2034年までに510億米ドル以上の売上が見込まれます。これらのパネルは、その費用対効果と標準的な封止技術との互換性により、引き続き市場を独占しています。結晶モジュールは一般的にEVAベースの封止材と組み合わされ、手頃な価格で十分な紫外線保護と耐熱性を提供します。構造が比較的単純で、さまざまな太陽電池用途で主流となっているため、従来のラミネート材料に理想的に適合し、封止材市場の成長をさらに後押ししています。

用途別では、商業・産業分野が2024年の太陽光発電封止材世界市場シェアの44.7%を占めています。この分野が突出しているのは、特に大規模な設置において高性能太陽電池モジュールの導入が増加しているためです。こうしたプロジェクトでは、過酷な使用条件に耐えながら長期にわたって優れた効率を実現できる高度な封止システムが必要とされることが多いです。商業用太陽光発電設備が厳しい性能基準に直面する中、信頼性、熱制御、劣化耐性を強化した革新的な封止材への需要が高まっています。

地域別では、北米市場が2024年に29.8%のシェアを占め、米国が圧倒的な役割を果たしています。米国の太陽光発電封止材市場規模は、2022年に47億米ドル、2023年に76億米ドル、2024年に95億米ドルとなりました。この成長を支える主な要因は、封止剤製造に特に重点を置いた、強固な国内太陽電池サプライチェーンの開発に対する連邦政府のコミットメントです。シリコンベース技術と薄膜技術の両方における太陽電池コンポーネントの生産強化を目指す国家的イニシアティブが、高性能封止材の幅広い採用に寄与しています。こうした市場開拓は、封止材分野の既存企業と新規参入企業の双方に大きな市場機会をもたらすと予想されます。

この分野で事業を展開する大手企業は、市場ポジションを確保するためにさまざまな戦略を駆使しています。生産能力を拡大し、EVAフィルムやPOEフィルムの自社製造に投資し、トップクラスの太陽電池モジュールメーカーと強力なパートナーシップを結んでいます。また、地域市場向けに製品を調整し、ポリマーサプライヤーと後方統合し、材料の耐久性と耐紫外線性を向上させるための研究開発を強化することにも注力しています。これによって、コスト競争力を維持しながら、進化する性能基準を満たす封止材を確保することができます。

大手封止材メーカーはまた、モジュール効率を高めるため、透明性やPID耐性などの材料特性の革新を優先しています。同時に、ロジスティクスを改善しリードタイムを短縮するため、現地に製造拠点を構築しています。垂直統合型モジュールメーカーとの戦略的合意は、これらの企業が市場での存在感を高め、サプライチェーンの安定性を向上させるのに役立っています。彼らの努力は、フィルム押出成形能力の拡大、ラミネーション技術の最適化、IECやBISなどの国際認証規格への準拠にも及んでおり、これらはすべて、世界の競合情勢において長期的な競争力を維持するために不可欠なものです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:パネルタイプ別、2021年~2034年

- 主要動向

- 結晶質

- 薄膜

- その他

第6章 市場規模・予測:材料別、2021年~2034年

- 主要動向

- EVA

- POE

- EPE

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 住宅

- 商業および工業

- ユーティリティ

第8章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 建設

- エレクトロニクス

- その他

第9章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- オーストリア

- デンマーク

- フィンランド

- フランス

- ドイツ

- イタリア

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- シンガポール

- 中東・アフリカ

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- ヨルダン

- オマーン

- ラテンアメリカ

- ブラジル

- チリ

- アルゼンチン

- ペルー

第10章 企業プロファイル

- 3M

- Al Technology

- Celanese

- Dow Corning

- DuPont

- Eastman

- First Solar

- Hangzhou First PV Material

- Momentive

- Mitsubishi Chemicals

- RenewSys India

- STR Holdings

- Trosifol

The Global Solar Encapsulation Market was valued at USD 34.7 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 61.6 billion by 2034. This upward trend is largely driven by the global pivot toward domestic solar manufacturing, supported by favorable government policies. Countries across the globe are introducing incentive-based frameworks to reduce dependency on imported photovoltaic components, thereby bolstering local production of critical materials such as encapsulants. These materials play a vital role in safeguarding solar cells from environmental exposure, prolonging panel life, and enhancing overall performance. As solar adoption continues to gain ground in residential, commercial, and utility-scale projects, the need for reliable, high-quality encapsulation materials is becoming increasingly essential across both established and emerging solar economies.

Manufacturers are scaling up their operations to meet the surging demand, particularly in markets where solar module production is expanding rapidly. Both developed and developing countries are investing heavily in infrastructure that supports the local manufacturing of solar modules, with a strong focus on streamlining the supply chain. This shift is encouraging significant growth in the consumption of encapsulation materials, which are key to ensuring long-term module efficiency and durability. The trend is further reinforced by the growing number of vertically integrated solar companies that require dependable access to encapsulants for large-scale production. As these companies consolidate control over the value chain, including raw material sourcing and module assembly, their demand for stable and consistent encapsulation supply is expected to grow, positively influencing market dynamics over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.7 Billion |

| Forecast Value | $61.6 Billion |

| CAGR | 6.1% |

The crystalline panel segment is anticipated to generate over USD 51 billion in revenue by 2034. These panels continue to dominate the market due to their cost-effectiveness and compatibility with standard encapsulation techniques. Crystalline modules are commonly paired with EVA-based encapsulants, which offer adequate UV protection and thermal resistance at affordable rates. Their relatively simple structure and mainstream adoption across various solar applications make them an ideal fit for conventional lamination materials, further supporting encapsulant market growth.

Within the application landscape, the commercial and industrial sector accounted for 44.7% of the global solar encapsulation market share in 2024. The segment's prominence is attributed to the rising deployment of high-performance solar modules, particularly in large-scale installations. These projects often require advanced encapsulation systems capable of withstanding harsh operating conditions while delivering superior efficiency over time. As commercial solar installations face rigorous performance standards, demand is growing for innovative encapsulants that offer enhanced reliability, thermal control, and resistance to degradation.

In regional terms, the North American market held a 29.8% share in 2024, with the U.S. playing a dominant role. The solar encapsulation market in the United States was valued at USD 4.7 billion in 2022, USD 7.6 billion in 2023, and USD 9.5 billion in 2024. A key factor supporting this growth is the federal commitment to developing a robust domestic solar supply chain, with specific emphasis on encapsulant manufacturing. National initiatives aimed at strengthening the production of solar components across both silicon-based and thin-film technologies are contributing to the broader adoption of high-performance encapsulation materials. These developments are expected to create strong market opportunities for both established players and new entrants in the encapsulant space.

Major companies operating in this sector are leveraging a combination of strategies to secure their market position. They are expanding their production capacities, investing in in-house manufacturing of EVA and POE films, and forming strong partnerships with top-tier solar module producers. Many are also focusing on tailoring products for regional markets, integrating backward with polymer suppliers, and intensifying their research and development efforts to improve material durability and UV resistance. This helps ensure their encapsulants meet evolving performance standards while remaining cost-competitive.

Leading encapsulant producers are also prioritizing innovation in material properties such as transparency and PID resistance to enhance module efficiency. At the same time, they are building localized manufacturing hubs to improve logistics and reduce lead times. Strategic agreements with vertically integrated module manufacturers are helping these companies boost their market presence and improve supply chain stability. Their efforts also extend to scaling up film extrusion capabilities, optimizing lamination technologies, and ensuring compliance with international certification standards such as IEC and BIS, all of which are instrumental in maintaining long-term competitiveness in the global solar encapsulation landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Panel Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Crystalline

- 5.3 Thin Film

- 5.4 Others

Chapter 6 Market Size and Forecast, By Material Type, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 EVA

- 6.3 POE

- 6.4 EPE

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial & industrial

- 7.4 Utility

Chapter 8 Market Size and Forecast, By End Use, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 Construction

- 8.3 Electronics

- 8.4 Others

Chapter 9 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & MT)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Austria

- 9.3.2 Denmark

- 9.3.3 Finland

- 9.3.4 France

- 9.3.5 Germany

- 9.3.6 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 India

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.5 Middle East and Africa

- 9.5.1 Israel

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

- 9.5.4 Jordan

- 9.5.5 Oman

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Chile

- 9.6.3 Argentina

- 9.6.4 Peru

Chapter 10 Company Profiles

- 10.1 3M

- 10.2 Al Technology

- 10.3 Celanese

- 10.4 Dow Corning

- 10.5 DuPont

- 10.6 Eastman

- 10.7 First Solar

- 10.8 Hangzhou First PV Material

- 10.9 Momentive

- 10.10 Mitsubishi Chemicals

- 10.11 RenewSys India

- 10.12 STR Holdings

- 10.13 Trosifol