|

市場調査レポート

商品コード

1773413

自動車用ISG(インテグレーテッドスタータージェネレーター)ユニット市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Integrated Starter-Generator Units Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用ISG(インテグレーテッドスタータージェネレーター)ユニット市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月16日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

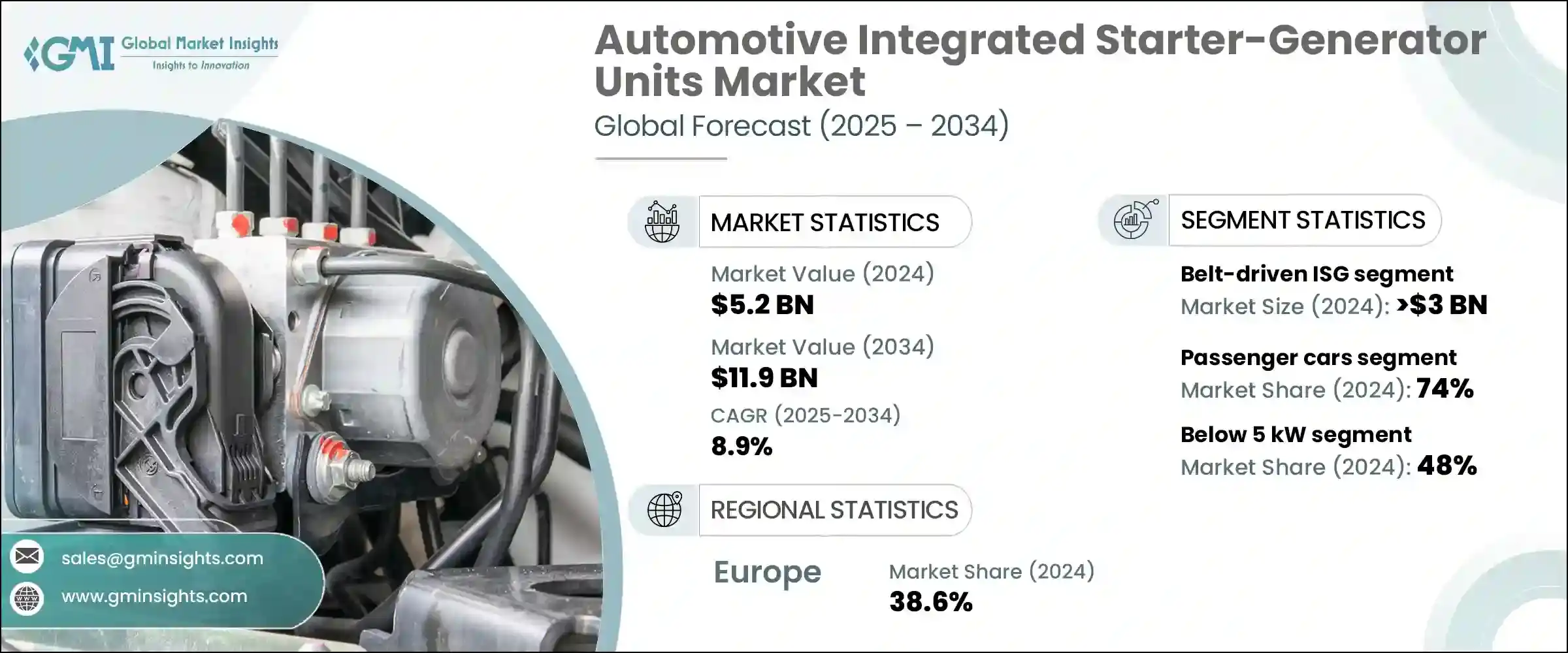

自動車用ISG(インテグレーテッドスタータージェネレーター)ユニットの世界市場規模は、2024年に52億米ドルとなり、CAGR 8.9%で成長し、2034年には119億米ドルに達すると予測されています。

この成長の主な要因は、効率性の向上と環境負荷の低減を両立させた自動車に対する需要の高まりです。排出ガスをめぐる世界の規制が厳しくなるにつれ、自動車メーカーはISG技術を組み込んだマイルド・ハイブリッド・モデルの展開を加速させています。これらのシステムは、フル・ハイブリッドやプラグイン・ハイブリッドに関連した高価格タグを付けずに、より優れた燃費を求める消費者にとって魅力的です。ISGを搭載したパワートレインは、従来の車両設計への影響を最小限に抑えながら、顕著な燃費節約を実現する中間的な存在です。

また、プレミアムカーやパフォーマンスカーへの意欲の高まりも、ISGユニットの採用を加速させています。ISGユニットは、エンジンのスタート・ストップ操作をよりスムーズにし、低速トルクを向上させてドライビング・フィールを高めることに貢献するからです。これは、パワーや高級感を犠牲にすることなく効率化を実現するという、ハイエンドバイヤーが求めるものと完全に一致します。都市部における渋滞の増加に伴い、アイドリングストップや頻繁な停車時の燃料消費を抑えるシステムの需要が急増しています。ISGユニットは、排出ガスを削減しながらこれらの課題を管理するのに役立ち、よりスマートで環境に優しい都市交通を推進する上で好ましい選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 52億米ドル |

| 予測金額 | 119億米ドル |

| CAGR | 8.9% |

2024年、ベルト駆動ISGシステム・セグメントは30億米ドルを生み出し、自動車メーカーに実用的でコスト効率の高い電動化ルートを提供することで市場を独占しました。これらのユニットはエンジンの前部に取り付けられ、ベルトを介してクランクシャフトに接続されるため、メーカーは主要部品を再設計することなく統合することができます。この合理的な統合は、既存の車両プラットフォームを迅速に電動化したいブランドにとって大きな利点であり、時間と資本の両方を節約することができます。

マイルド・ハイブリッド電気自動車は2024年に最大の市場シェアを占め、今後も主要な成長分野であり続けると予測されます。これらの車両はコンパクトなバッテリーを搭載しており、惰性走行時の静かな動作からシームレスなエンジン再始動まで、ドライバーがすぐに気づく性能上の利点を提供します。低速トルクのブーストは、特にストップ・アンド・ゴーの交通におけるドライバビリティを向上させる。さらに、マイルド・ハイブリッドは外部充電に依存しないため、運転習慣を変えることなく環境に優しい選択肢を求める消費者にとって理想的です。その結果、これらのシステムは商用車と自家用車の両方で一般的になりつつあります。

ドイツ自動車用ISG(インテグレーテッドスタータージェネレーター)ユニット2024年の市場規模は4億9,670万米ドル。同国の圧倒的な地位は、成熟した自動車製造基盤と、さまざまな車両クラスでの48ボルトシステムの早期採用によって支えられています。大手メーカーは、規制上の要求と消費者の期待の両方を満たすために、ラインアップ全体にベルト駆動ISG技術を積極的に導入しています。ボッシュ、コンチネンタル、ゼット・エフ・フリードリヒスハーフェン(ZF Friedrichshafen)などの主要メーカーを擁するドイツの強固なサプライチェーンは、現地生産と技術革新をさらにサポートし、世界のISG市場で競争力を維持するのに役立っています。

世界の自動車用ISG(インテグレーテッドスタータージェネレーター)ユニット市場で活躍する主要企業には、ボッシュ、三菱電機、デンソー、ボルグワーナー、マグナ・インターナショナル、ZFフリードリヒスハーフェン、SEGオートモーティブ、コンチネンタル、日立アステモ、ヴァレオなどがあります。自動車用ISG市場で主要な地位を確保するため、各企業はいくつかの戦略分野に注力しています。中核戦略のひとつは、ISGシステムの性能向上、軽量化、エネルギー効率改善のための研究開発への投資です。メーカー各社はまた、さまざまな車両カテゴリーにISGを統合できるよう、プラットフォームの拡張性を目標としています。OEMとのコラボレーションは、特定のドライブトレイン向けのソリューションをカスタマイズする上で重要な役割を果たします。さらに、企業はリードタイムを短縮し、地域の調達政策に準拠するため、現地生産を通じて生産能力を強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 燃費効率への需要の急増

- 世界中で厳しい排出規制

- 費用対効果の高い電化ソリューション

- 高級品および中高級品セグメントにおける需要の増加

- 業界の潜在的リスク&課題

- エントリーレベルの車両の初期統合コストが高め

- 消費者の認知度と価値の認識が限られている

- 市場機会

- 新興市場における48Vマイルドハイブリッドの拡大

- 商用車の電動化

- プレミアム/高級車向け高性能ISG

- 旧型車両のアフターマーケットと改造

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ベルト駆動ISG(B-ISG)

- クランクシャフトマウントISG

- デュアルクラッチトランスミッションISG

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- SUV

- ハッチバック

- 商用車

- LCV(小型商用車)

- MCV(中型商用車)

- HCV(大型商用車)

第7章 市場推計・予測:出力別、2021年~2034年

- 主要動向

- 5kW未満

- 5~10kW

- 10kW以上

第8章 市場推計・予測:推進タイプ別、2021年~2034年

- 主要動向

- マイルドハイブリッド電気自動車(MHEV)

- 内燃機関(ICE)車

第9章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- マレーシア

- シンガポール

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Aisin Corporation

- BorgWarner

- Bosch

- Continental

- Denso Corporation

- Hitachi Astemo

- Hyundai Mobis Co

- Johnson Electric Holdings

- Magna International

- MAHLE Group

- Mando Corporation

- Mitsubishi Electric Corporation

- Nidec Corporation

- Prestolite Electric Incorporated

- Schaeffler AG

- SEG Automotive

- Toyota Industries

- Woory Industrial Co

- Valeo

- ZF Friedrichshafen

The Global Automotive Integrated Starter-Generator Units Market was valued at USD 5.2 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 11.9 billion by 2034. This growth is largely fueled by rising demand for vehicles that offer both improved efficiency and reduced environmental impact. As global regulations surrounding emissions become stricter, automakers are ramping up the rollout of mild hybrid models that incorporate ISG technology. These systems are attractive to consumers seeking better fuel economy without the steep price tag associated with full or plug-in hybrids. ISG-equipped powertrains provide a middle ground-delivering noticeable fuel savings with minimal disruption to conventional vehicle designs.

The growing appetite for premium and performance vehicles is also accelerating the adoption of ISG units, as they contribute to smoother engine start-stop operations and deliver low-end torque improvements that enhance driving feel. This aligns perfectly with what high-end buyers want-efficiency without sacrificing power or luxury. As congestion increases in urban areas, demand for systems that reduce fuel use during idling and frequent stops has surged. ISG units help manage these challenges while also reducing emissions, making them a favored option in the push for smarter, greener urban transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 Billion |

| Forecast Value | $11.9 Billion |

| CAGR | 8.9% |

In 2024, the belt-driven ISG systems segment generated USD 3 billion, dominating the market by offering automakers a practical and cost-effective route to electrification. These units are mounted on the engine's front and connected via a belt to the crankshaft, allowing manufacturers to integrate them without redesigning major components. This streamlined integration is a major advantage for brands looking to electrify existing vehicle platforms quickly, saving both time and capital.

Mild hybrid-electric vehicles represented the largest market share in 2024 and are projected to remain a key growth area. These vehicles incorporate a compact battery and deliver performance benefits that drivers can immediately notice-from quiet operation during coasting to seamless engine restarts. The low-end torque boost improves drivability, particularly in stop-and-go traffic. Additionally, mild hybrids do not rely on external charging, making them ideal for consumers who want eco-friendly options without changing their driving habits. As a result, these systems are becoming more common across both commercial fleets and personal vehicles.

Germany Automotive Integrated Starter-Generator Units Market generated USD 496.7 million in 2024. The country's dominant position is supported by a mature automotive manufacturing base and early adoption of 48-volt systems across various vehicle classes. Leading manufacturers have aggressively implemented belt-driven ISG technology across their lineups to meet both regulatory demands and consumer expectations. Germany's robust supply chain, with major contributors such as Bosch, Continental, and ZF Friedrichshafen, further supports local production and innovation, helping the country maintain a competitive edge in the global ISG market.

Key players active in the Global Automotive Integrated Starter-Generator Units Market include Bosch, Mitsubishi Electric, Denso, BorgWarner, Magna International, ZF Friedrichshafen, SEG Automotive, Continental, Hitachi Astemo, and Valeo. To secure a leading position in the automotive ISG market, companies are focusing on several strategic areas. One core strategy involves investment in R&D to enhance performance, reduce weight, and improve the energy efficiency of ISG systems. Manufacturers are also targeting platform scalability to allow ISG integration across various vehicle categories. Collaborations with OEMs play a key role in customizing solutions for specific drivetrains. In addition, firms are strengthening their production capabilities through localized manufacturing to reduce lead times and comply with regional sourcing policies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Power rating

- 2.2.5 Propulsion type

- 2.2.6 Sales channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in demand for fuel efficiency

- 3.2.1.2 Stricter emission regulations worldwide

- 3.2.1.3 Cost-effective electrification solution

- 3.2.1.4 Growing demand in the luxury and mid-premium segment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial integration cost for entry-level vehicles

- 3.2.2.2 Limited consumer awareness and perceived value

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of 48V mild hybrids in emerging markets

- 3.2.3.2 Commercial vehicle electrification

- 3.2.3.3 High-performance ISGs for premium/luxury vehicles

- 3.2.3.4 Aftermarket & retrofits for legacy fleets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Belt-driven ISG (B-ISG)

- 5.3 Crankshaft-mounted ISG

- 5.4 Dual-clutch transmission ISG

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedan

- 6.2.2 SUV

- 6.2.3 Hatchback

- 6.3 Commercial vehicles

- 6.3.1 LCVs (light commercial vehicles)

- 6.3.2 MCVs (medium commercial vehicles)

- 6.3.3 HCVs (heavy commercial vehicles)

Chapter 7 Market Estimates & Forecast, By Power rating, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Below 5 kW

- 7.3 5–10 kW

- 7.4 Above 10 kW

Chapter 8 Market Estimates & Forecast, By Propulsion type, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Mild hybrid electric vehicles (MHEVs)

- 8.3 Internal combustion engine (ICE) vehicles

Chapter 9 Market Estimates & Forecast, By Sales channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aisin Corporation

- 11.2 BorgWarner

- 11.3 Bosch

- 11.4 Continental

- 11.5 Denso Corporation

- 11.6 Hitachi Astemo

- 11.7 Hyundai Mobis Co

- 11.8 Johnson Electric Holdings

- 11.9 Magna International

- 11.10 MAHLE Group

- 11.11 Mando Corporation

- 11.12 Mitsubishi Electric Corporation

- 11.13 Nidec Corporation

- 11.14 Prestolite Electric Incorporated

- 11.15 Schaeffler AG

- 11.16 SEG Automotive

- 11.17 Toyota Industries

- 11.18 Woory Industrial Co

- 11.19 Valeo

- 11.20 ZF Friedrichshafen