|

市場調査レポート

商品コード

1773369

航空宇宙用ファスナーの市場機会と促進要因、産業動向分析、2025~2034年予測Aerospace Fasteners Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 航空宇宙用ファスナーの市場機会と促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年06月17日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

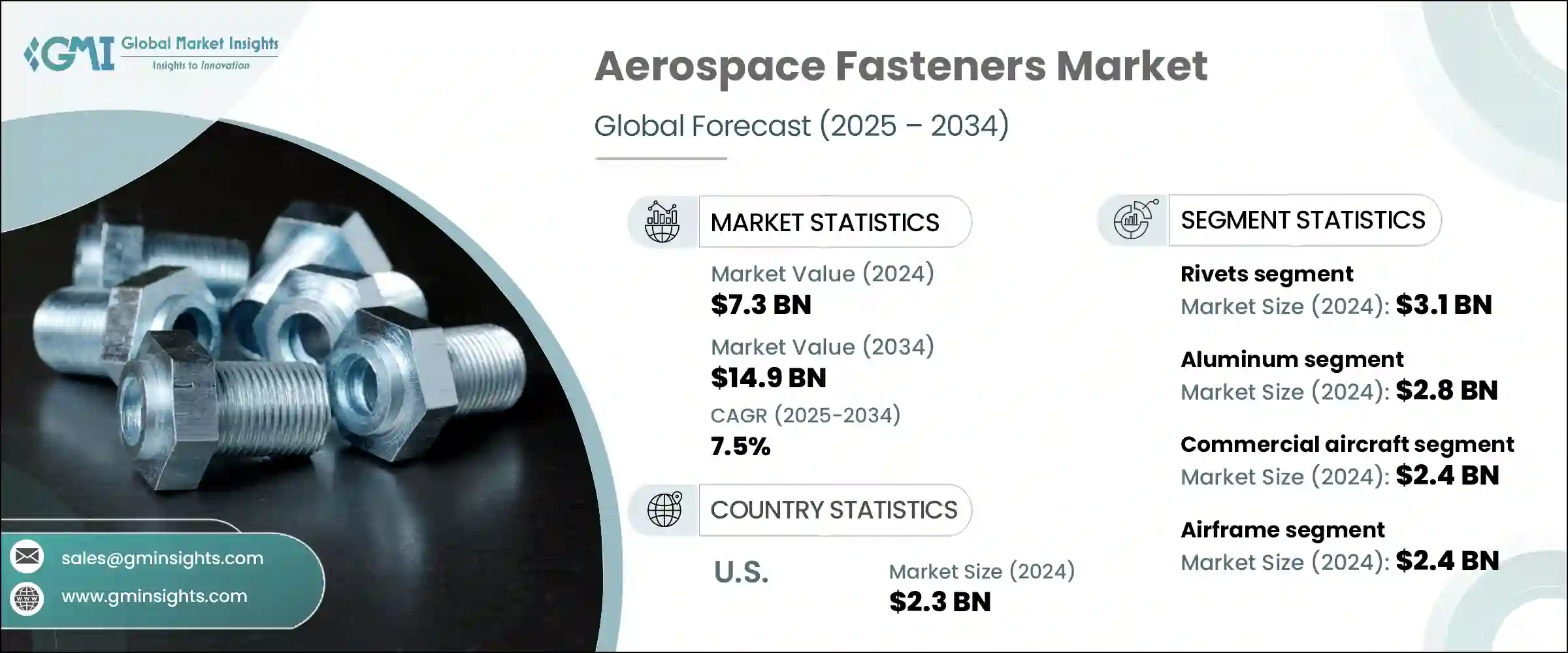

世界の航空宇宙用ファスナー市場は、2024年には73億米ドルと評価され、CAGR 7.5%で成長し、2034年には149億米ドルに達すると推定されています。

この力強い成長軌道は、民間航空会社の機体の急速な拡大や軍事航空インフラの継続的なアップグレードと密接に結びついています。新興経済圏における航空需要の増加は、国防への投資の増加と相まって、時代遅れの航空機部品をより新しく軽量で高性能な代替品に置き換える動きを加速させています。燃費効率と耐久性の重要性の高まりにより、航空宇宙用ファスナーは構造部品製造における技術革新の中心に位置づけられ、OEM組み立てとアフターマーケット整備の両方において不可欠なものとなっています。

世界の貿易情勢はこの市場に大きな影響を与えています。特に中国からの輸入航空宇宙グレードのアルミニウムと鉄鋼を対象とした以前の関税は、原材料コストの上昇と必須部品へのアクセスの制約につながりました。こうした混乱により、米国を拠点とするメーカーは調達戦略の見直しを余儀なくされ、多くのメーカーが国内サプライヤーへの転換やベンダーポートフォリオの多様化を行い、リスクの最小化を図りました。このような行動は、厳しいスケジュールの製造エコシステムの中で納期を維持しつつ、コスト圧力を相殺することを目的としていました。軽量設計と構造信頼性向上へのシフトが進む中、メーカーは複合材料とシームレスに機能するファスナーに注目しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 73億米ドル |

| 予測金額 | 149億米ドル |

| CAGR | 7.5% |

リベットセグメントは2024年に31億米ドルを生み出しました。リベットは、機体の完全性を維持する上で重要な、軽量でありながら耐久性のある接合部を提供する上で不可欠な役割を果たすため、優位性を維持しています。これらのファスナーは、民間航空機製造、特に主翼や胴体のような高振動、高荷重部分に広く使用されています。リベット取り付けの進歩-特にブラインド・リベット技術-は、効率と信頼性をさらに高め、OEM製造と継続的な保守作業の両方で不可欠なものとなっています。

2024年の航空宇宙用ファスナーセグメントのアルミニウム部門は、28億米ドルと評価されます。アルミニウムの人気は、優れた強度対重量比、耐食性、費用対効果に起因しており、航空機の質量を減らして燃費を改善するために選択される材料となっています。航空機の設計が軽量化にますます重点を置くようになるにつれ、アルミニウム製ファスナーの需要は、特に重要でない構造用途や内装部品で増加の一途をたどっています。アルミニウム合金の配合が強化されたことで、最新の複合材構造との材料適合性も向上し、製造部門とサービス部門の両方で採用が進んでいます。

米国航空宇宙用ファスナー2024年の市場規模は23億米ドルでした。同国の優位性は、民間航空および防衛航空分野の大手メーカーの本拠地である、世界の航空宇宙ハブとしての地位にまで遡ることができます。この分野の大手企業は、継続的な機体整備と次世代システムの統合の両方で国内需要を刺激し続けています。米国はまた、世界で最も包括的なMROネットワークのひとつを擁しており、大規模な民間・軍用機の定期的なサービスサイクルやシステムのアップグレードをサポートしています。次世代爆撃機や極超音速航空機などの戦略的航空能力に焦点を当てた国防費の増加は、チタン合金、高温インコネル、炭素ベースの複合材料で作られた特殊ファスナーへの需要を強化しています。

航空宇宙用ファスナー市場を積極的に形成している主要企業には、TriMas Corporation、Boeing、LISI Aerospace、Wurth Group、B&B Specialties Inc.、Cherry Aerospace、Precision Castparts Corp.、National航空宇宙用ファスナーCorporation、Preci-Manufacturing、Stanley Black &Decker Inc.、M.S Aerospace、Bollhoff Group、Howmet Aerospace Inc.などがあります。競争力を高めるために、航空宇宙用ファスナー業界の企業はいくつかの重要な戦略を採用しています。過酷な条件下でも確実に機能する、より軽量で耐食性に優れたファスナーを開発するため、研究開発に多額の投資を行っています。航空機OEMとの戦略的提携は、新しいプラットフォーム設計への早期統合を確実にするのに役立っています。さらに、企業は現地生産とデジタル調達システムを通じてサプライチェーンの最適化に注力し、混乱を最小限に抑えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界の航空交通量の増加と航空機の拡大

- 軍用機の近代化の急増

- MRO(メンテナンス、修理、オーバーホール)サービスの成長

- 高度な製造技術の導入

- 宇宙探査と衛星打ち上げの増加

- 業界の潜在的リスク&課題

- 高度なファスナー材料の高コスト

- 厳格な規制と認証要件

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 将来の市場動向

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 国防予算分析

- 世界の防衛費の動向

- 地域防衛予算配分

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 主要な防衛近代化プログラム

- 予算予測(2025~2034年)

- 業界の成長への影響

- 国別防衛予算

- サプライチェーンのレジリエンス

- 地政学的分析

- 人材分析

- デジタル変革

- 合併、買収、戦略的提携の情勢

- リスク評価と管理

- 主要契約の締結(2021~2024年)

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 市場集中分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展、2021~2024年

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:製品タイプ別、2021~2034年

- 主要動向

- リベット

- ネジ

- ナットとボルト

- その他

第6章 市場推計・予測:材料別、2021~2034年

- 主要動向

- アルミニウム

- 鋼鉄

- 超合金

- チタン

第7章 市場推計・予測:プラットフォーム別、2021~2034年

- 主要動向

- 民間航空機

- ナローボディ

- ワイドボディ

- リージョナルジェット

- 軍用機

- ビジネスジェット

- ヘリコプター

- 無人航空機(UAV)

第8章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 機体

- インテリア

- エンジン

- 操縦翼面

- 着陸装置

- その他

第9章 市場推計・予測:最終用途別、2021~2034年

- 主要動向

- OEM(オリジナル機器メーカー)

- MRO(メンテナンス、修理、オーバーホール)

第10章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- B&B Specialties Inc.

- Boeing

- Bollhoff Group

- Cherry Aerospace

- Howmet Aerospace Inc.

- LISI Aerospace

- M.S Aerospace

- National Aerospace Fasteners Corporation

- Preci-Manufacturing

- Precision Castparts Corp.

- Stanley Black &Decker, Inc.

- TriMas Corporation

- Wurth Group

The Global Aerospace Fasteners Market was valued at USD 7.3 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 14.9 billion by 2034. This robust growth trajectory is closely tied to the rapid expansion of commercial airline fleets and the continuous upgrades in military aviation infrastructure. Rising air travel demand across emerging economies, coupled with increasing investments in national defense, is fueling the replacement of outdated aircraft components with newer, lightweight, and high-performance alternatives. The growing importance of fuel efficiency and durability has placed aerospace fasteners at the center of innovation in structural component manufacturing, making them essential in both OEM assembly and aftermarket servicing.

The global trade landscape has had a significant influence on this market. Previous tariffs targeting imported aerospace-grade aluminum and steel-especially those from China-led to elevated raw material costs and constrained access to essential components. These disruptions forced US-based manufacturers to rethink sourcing strategies, with many turning to domestic suppliers or diversifying vendor portfolios to minimize risk. These actions aimed to offset cost pressures while maintaining delivery timelines in a tightly scheduled manufacturing ecosystem. With an ongoing shift toward lightweight design and enhanced structural reliability, manufacturers are focusing on fasteners that can work seamlessly with composite materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.3 Billion |

| Forecast Value | $14.9 Billion |

| CAGR | 7.5% |

The rivets segment generated USD 3.1 billion in 2024. Rivets maintain dominance due to their essential role in delivering lightweight yet durable joints that are critical in maintaining airframe integrity. These fasteners are widely used in commercial aircraft production, particularly for high-vibration, load-bearing areas such as wings and fuselages. Advances in rivet installation-particularly blind rivet technology-have further increased efficiency and reliability, making them indispensable across both OEM manufacturing and ongoing maintenance operations.

Aluminum segment in the aerospace fasteners segment in 2024, valued at USD 2.8 billion. Its popularity stems from a superior strength-to-weight ratio, corrosion resistance, and cost-effectiveness, making it the material of choice for reducing aircraft mass and improving fuel economy. As aircraft designs increasingly focus on weight reduction, demand for aluminum fasteners continues to climb, particularly in non-critical structural applications and interior components. Enhanced aluminum alloy formulations are also boosting material compatibility with modern composite structures, driving adoption across both manufacturing and servicing divisions.

United States Aerospace Fasteners Market generated USD 2.3 billion in 2024. The country's dominance can be traced to its position as a global aerospace hub, home to leading manufacturers across commercial and defense aviation. Major players in this space continue to fuel domestic demand with both ongoing fleet maintenance and the integration of next-generation systems. The U.S. also hosts one of the world's most comprehensive MRO networks, supporting regular service cycles and system upgrades for large civilian and military fleets. Rising defense expenditures, focused on strategic air capabilities such as next-gen bombers and hypersonic aircraft, have intensified demand for specialized fasteners made from titanium alloys, high-temperature Inconel, and carbon-based composites.

Key players actively shaping the Aerospace Fasteners Market include TriMas Corporation, Boeing, LISI Aerospace, Wurth Group, B&B Specialties Inc., Cherry Aerospace, Precision Castparts Corp., National Aerospace Fasteners Corporation, Preci-Manufacturing, Stanley Black & Decker Inc., M.S Aerospace, Bollhoff Group, and Howmet Aerospace Inc. To enhance their competitive edge, companies in the aerospace fasteners industry are adopting several key strategies. They're investing heavily in R&D to develop lighter, corrosion-resistant fasteners that perform reliably under extreme conditions. Strategic collaborations with aircraft OEMs help ensure early integration into new platform designs. Additionally, firms are focusing on supply chain optimization through localized manufacturing and digital procurement systems to minimize disruptions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Material trends

- 2.2.3 Platform trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO Perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing global air traffic & fleet expansion

- 3.2.1.2 Surge in military aircraft modernization

- 3.2.1.3 Growth in MRO (maintenance, repair, and overhaul) services

- 3.2.1.4 Adoption of advanced manufacturing technologies

- 3.2.1.5 Rising space exploration & satellite launches

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced fastener materials

- 3.2.2.2 Stringent regulatory and certification requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Pricing strategies

- 3.11 Emerging business models

- 3.12 Compliance requirements

- 3.13 Defense budget analysis

- 3.14 Global defense spending trends

- 3.15 Regional defense budget allocation

- 3.15.1 North America

- 3.15.2 Europe

- 3.15.3 Asia Pacific

- 3.15.4 Middle East and Africa

- 3.15.5 Latin America

- 3.16 Key defense modernization programs

- 3.17 Budget forecast (2025-2034)

- 3.17.1 Impact on industry growth

- 3.17.2 Defense budgets by country

- 3.18 Supply chain resilience

- 3.19 Geopolitical analysis

- 3.20 Workforce analysis

- 3.21 Digital transformation

- 3.22 Mergers, acquisitions, and strategic partnerships landscape

- 3.23 Risk assessment and management

- 3.24 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Million & Million Units)

- 5.1 Key trends

- 5.2 Rivets

- 5.3 Screws

- 5.4 Nuts & bolts

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Million & Million Units)

- 6.1 Key trends

- 6.2 Aluminum

- 6.3 Steel

- 6.4 Superalloys

- 6.5 Titanium

Chapter 7 Market Estimates and Forecast, By Platform, 2021 – 2034 (USD Million & Million Units)

- 7.1 Key trends

- 7.2 Commercial aircraft

- 7.2.1 Narrow-body

- 7.2.2 Wide-body

- 7.2.3 Regional jets

- 7.3 Military aircraft

- 7.4 Business jets

- 7.5 Helicopters

- 7.6 Unmanned aerial vehicles (UAVs)

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Million Units)

- 8.1 Key trends

- 8.2 Airframe

- 8.3 Interiors

- 8.4 Engine

- 8.5 Control surfaces

- 8.6 Landing gear

- 8.7 Other

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Million & Million Units)

- 9.1 Key trends

- 9.2 OEM (Original Equipment Manufacturers)

- 9.3 MRO (Maintenance, Repair, and Overhaul)

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 B&B Specialties Inc.

- 11.2 Boeing

- 11.3 Bollhoff Group

- 11.4 Cherry Aerospace

- 11.5 Howmet Aerospace Inc.

- 11.6 LISI Aerospace

- 11.7 M.S Aerospace

- 11.8 National Aerospace Fasteners Corporation

- 11.9 Preci-Manufacturing

- 11.10 Precision Castparts Corp.

- 11.11 Stanley Black & Decker, Inc.

- 11.12 TriMas Corporation

- 11.13 Wurth Group