|

市場調査レポート

商品コード

1773338

BOPET包装フィルムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測BOPET Packaging Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| BOPET包装フィルムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月18日

発行: Global Market Insights Inc.

ページ情報: 英文 189 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

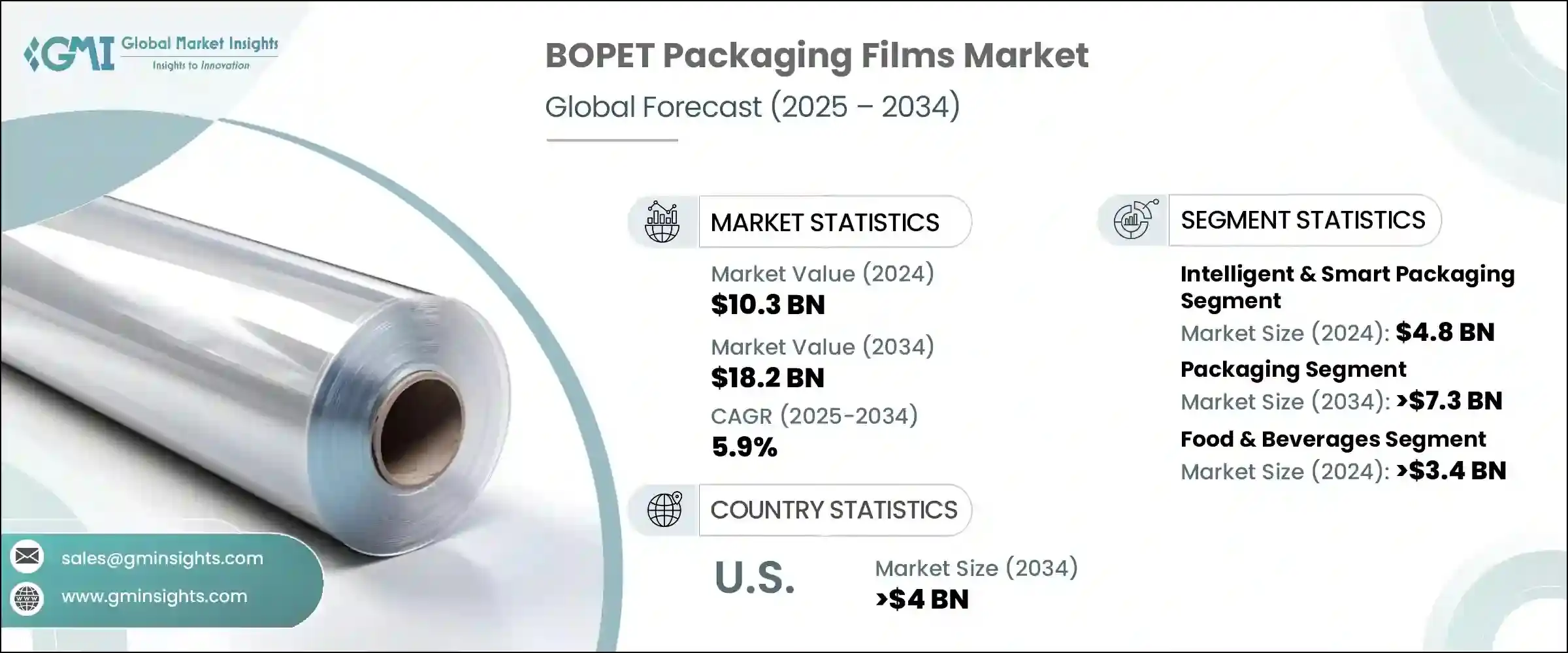

世界のBOPET包装フィルム市場は、2024年には103億米ドルと評価され、CAGR5.9%で成長し、2034年までには182億米ドルに達すると推定されています。

この成長は、eコマースプラットフォームやラストマイル配送システムの急速な開発、環境に優しい包装材を推進する持続可能性の義務付けや規制の厳格化によって大きく後押しされています。同市場は、国際的な貿易摩擦、特にトランプ政権が導入した報復関税による課題に直面しており、これにより輸入製造投入資材のコストが上昇しています。この分野の大手企業の多くは輸入原材料に大きく依存しているため、関税によってメーカーはコスト増を消費者に転嫁するか、費用対効果の高い国内代替品を探す必要に迫られています。

このような逆風にもかかわらず、軽量で費用対効果の高いフレキシブルな包装に対する需要は伸び続けています。BOPETフィルムは、異なる製品寸法への適応性が高く、容積重量の削減と出荷効率の最適化に貢献するため、硬質フォーマットと比較して明確な利点を提供します。消費者主導の期待やハイパーローカル配送の動向は、軽量包装設計の革新をさらに促しています。また、リサイクル可能、開封防止、賞味期限延長を求める世界の動きも、食品、医薬品、電子機器、パーソナルケア業界全体でBOPETフィルムの使用を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 103億米ドル |

| 予測金額 | 182億米ドル |

| CAGR | 5.9% |

耐久性と柔軟性を併せ持つ保護包装のニーズが高まっているため、硬い代替品よりもBOPETフィルム形式が支持され続けています。これらのフィルムは、さまざまな製品の形状やサイズに適合する能力が特に評価されており、出荷量の削減、ひいては物流コストの削減に役立っています。この動向は、規制と消費者の期待の両方を満たす環境に優しい包装に対する世界の需要の高まりと一致しています。

BOPETフィルムはまた、インテリジェントでアクティブな包装技術の理想的な基材としても人気を集めています。2024年、スマート包装分野は48億米ドルに達しました。これらの革新的な包装ソリューションには、脱酸素剤、抗菌剤、水分調整剤などの機能性成分が含まれ、パッケージ内部の環境と相互作用して製品の鮮度と安全性を保ちます。BOPETフィルムは、その高い熱安定性、優れたバリア性、化学的耐久性により、これらの用途を効果的にサポートします。このような特性により、BOPETフィルムは食品・飲料、ヘルスケア、化粧品など、製品の長寿命と完全性が重要な分野で好まれています。

より広範な包装用途分野は、2034年までに73億米ドルに達すると予測されています。この分野では、BOPETフィルムがその優れた機械的強度、透明性、水分・ガスバリア性により優位を占めています。BOPETフィルムは、特に医薬品、食品、パーソナルケアなど、高い性能が要求される産業における多層・フレキシブル包装システムに非常に適しています。食品安全法の厳格化、持続可能性に関する消費者の意識の高まり、リサイクル可能なソリューションの必要性により、一次包装と二次包装の両方でBOPET材料の使用が加速しています。さらに、世界のオンライン小売の拡大が、製品の安全性を確保し、賞味期限を延長する包装に対する需要を押し上げています。

米国のBOPET包装フィルム市場は2034年までに40億米ドルに達すると予測されています。連邦政府のロジスティクス、医薬品、食品、エレクトロニクスなどのセクターからの需要が、フレキシブル包装の技術革新を牽引し続けています。米国メーカーは、消費者の期待や持続可能性の目標に沿うため、リサイクル可能な素材やバイオベースの素材へのシフトを迫られています。このような要求の高まりは、軽量フレキシブルメーラーやリサイクル可能な緩衝材といった先進的なソリューションの開発を促しています。世界のMitsubishi Polyester Film GmbHのようなメーカーは、性能と持続可能性のバランスを取りながら、オムニチャネル小売モデル向けに設計された環境に優しいパッケージの開発を主導しています。

世界のBOPET包装フィルム市場の主要企業には、itsubishi Polyester Film GmbH、SKC、SRF Limited、Polyplex、UFlex Limitedなどが挙げられます。BOPET包装フィルム業界の企業は、市場基盤を強化するため、垂直統合、持続可能な製品開拓への投資、戦略的パートナーシップに注力しています。大手企業は、輸入品への依存度を下げ、関税の影響を軽減するために、生産能力を増強し、サプライチェーンを現地化しています。イノベーションが主な役割を担っており、研究開発チームは、変化する規制要件や消費者の需要に対応するため、リサイクル可能、生分解性、軽量フィルムのソリューションを開発しています。また、各社はeコマースやFMCGブランドと提携し、動きの速い配送システムに合わせた特殊な包装形態を共同開発しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 食品・飲料および医薬品業界の成長

- 高性能断熱材およびラミネート用途での使用が増加

- 柔軟で軽量な包装ソリューションに対する需要の高まり

- 持続可能でリサイクル可能な包装材料の急増

- BOPETフィルムは水分やガスに対する優れたバリア性を備えています

- 業界の潜在的リスク・課題

- 多層フィルム構造によるリサイクルの課題

- 原材料価格の変動(例:PTA、MEG)

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- インテリジェントでスマートな包装

- アクティブ包装

第6章 市場推計・予測:用途別、2021年~2034年

- 包装

- 産業

- 電気・電子工学

- 画像診断

- その他

第7章 市場推計・予測:最終用途別、2021年~2034年

- 食品・飲料

- 医薬品

- パーソナルケア・化粧品

- 家電

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Amcor PLC

- Avery Dennison

- BASF SE

- CCL Industries Inc.

- Checkpoint Systems, Inc

- DuPont Teijin Films

- Klockner Pentaplast

- Sealed Air Corporation

- Sonoco Products Company

- Tetra Pak International S.A.

The Global BOPET Packaging Films Market was valued at USD 10.3 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 18.2 billion by 2034. This growth is largely fueled by the rapid development of e-commerce platforms and last-mile delivery systems, along with stricter sustainability mandates and regulations promoting eco-friendly packaging materials. The market faces challenges from international trade tensions, particularly the retaliatory tariffs introduced by the Trump administration, which have increased the cost of imported manufacturing inputs. Since many major players in this sector depend heavily on imported raw materials, the tariffs have forced manufacturers to either pass the increased costs on to consumers or find cost-effective domestic alternatives.

Despite these headwinds, the demand for lightweight, cost-effective, and flexible packaging continues to grow. BOPET films offer a distinct advantage over rigid formats, as they are highly adaptable to different product dimensions, helping reduce volumetric weight and optimizing shipping efficiency. Consumer-driven expectations and hyperlocal delivery trends are further encouraging innovation in lightweight packaging design. The expanding global push for recyclable, tamper-evident, and extended-shelf-life packaging is also pushing the use of BOPET films across food, pharmaceuticals, electronics, and personal care industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.3 billion |

| Forecast Value | $18.2 billion |

| CAGR | 5.9% |

The growing need for protective packaging that combines durability with flexibility continues to favor BOPET film formats over rigid alternatives. These films are especially valued for their ability to conform to various product shapes and sizes, which helps in reducing shipping volumes and, ultimately, logistics costs. This trend is in line with the increasing global demand for environmentally friendly packaging that meets both regulatory and consumer expectations.

BOPET films are also gaining popularity as ideal substrates for intelligent and active packaging technologies. In 2024, the smart packaging segment reached USD 4.8 billion. These innovative packaging solutions include functional components such as oxygen scavengers, antimicrobial agents, and moisture regulators, which interact with the internal package environment to preserve product freshness and safety. BOPET films support these applications effectively due to their high thermal stability, excellent barrier resistance, and chemical durability. These qualities make them a preferred choice for sectors such as food and beverage, healthcare, and cosmetics, where product longevity and integrity are critical.

The broader packaging application segment is forecasted to reach USD 7.3 billion by 2034. Within this space, BOPET films dominate due to their superior mechanical strength, transparency, and moisture and gas barrier capabilities. They are highly suitable for multilayer and flexible packaging systems, especially in industries demanding high performance, such as pharmaceuticals, food, and personal care. Stricter food safety laws, growing consumer awareness regarding sustainability, and the need for recyclable solutions have accelerated the use of BOPET materials in both primary and secondary packaging. Additionally, the expansion of global online retail is boosting demand for packaging that ensures product security and extends shelf life.

United States BOPET Packaging Films Market is projected to reach USD 4 billion by 2034. Demand from sectors such as federal logistics, pharmaceuticals, food, and electronics continue to drive innovation in flexible packaging. US manufacturers are under increasing pressure to shift toward recyclable and bio-based materials to align with consumer expectations and sustainability goals. These evolving demands are inspiring the development of advanced solutions such as lightweight flexible mailers and recyclable cushioning formats. Manufacturers like Mitsubishi Polyester Film GmbH worldwide are leading the charge in creating eco-friendly packaging designed for omnichannel retail models while balancing performance and sustainability.

Key players in the Global BOPET Packaging Films Market include Mitsubishi Polyester Film GmbH, SKC, SRF Limited, Polyplex, and UFlex Limited. To strengthen their market foothold, companies in the BOPET packaging films industry focus on vertical integration, investment in sustainable product development, and strategic partnerships. Leading firms are ramping up production capacities and localizing supply chains to reduce dependency on imports and mitigate tariff impacts. Innovation plays a key role, with R&D teams developing recyclable, biodegradable, and lightweight film solutions to meet shifting regulatory requirements and consumer demands. Companies are also forming alliances with e-commerce and FMCG brands to co-develop specialized packaging formats tailored for fast-moving delivery systems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growth in food & beverage and pharmaceutical industries

- 3.3.1.2 Increasing use in high-performance insulation and lamination applications

- 3.3.1.3 Rising demand for flexible and lightweight packaging solutions

- 3.3.1.4 Surge in sustainable and recyclable packaging materials

- 3.3.1.5 Excellent barrier properties of BOPET films against moisture and gases

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Recycling challenges due to multi-layer film structures

- 3.3.2.2 Volatility in raw material prices (e.g., PTA and MEG)

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market estimates & forecast, By Type, 2021 - 2034 (USD Billion)

- 5.1 Intelligent & smart packaging

- 5.2 Active packaging

Chapter 6 Market estimates & forecast, By Application, 2021 - 2034 (USD Billion)

- 6.1 Packaging

- 6.2 Industrial

- 6.3 Electrical and electronics

- 6.4 Imaging

- 6.5 Others

Chapter 7 Market estimates & forecast, By End Use, 2021 - 2034 (USD Billion)

- 7.1 Food & beverages

- 7.2 Pharmaceuticals

- 7.3 Personal care & cosmetics

- 7.4 Consumer electronics

- 7.5 Others

Chapter 8 Market estimates and forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amcor PLC

- 9.2 Avery Dennison

- 9.3 BASF SE

- 9.4 CCL Industries Inc.

- 9.5 Checkpoint Systems, Inc

- 9.6 DuPont Teijin Films

- 9.7 Klockner Pentaplast

- 9.8 Sealed Air Corporation

- 9.9 Sonoco Products Company

- 9.10 Tetra Pak International S.A.