|

市場調査レポート

商品コード

1773266

医療用X線の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Medical X-ray Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 医療用X線の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月16日

発行: Global Market Insights Inc.

ページ情報: 英文 141 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

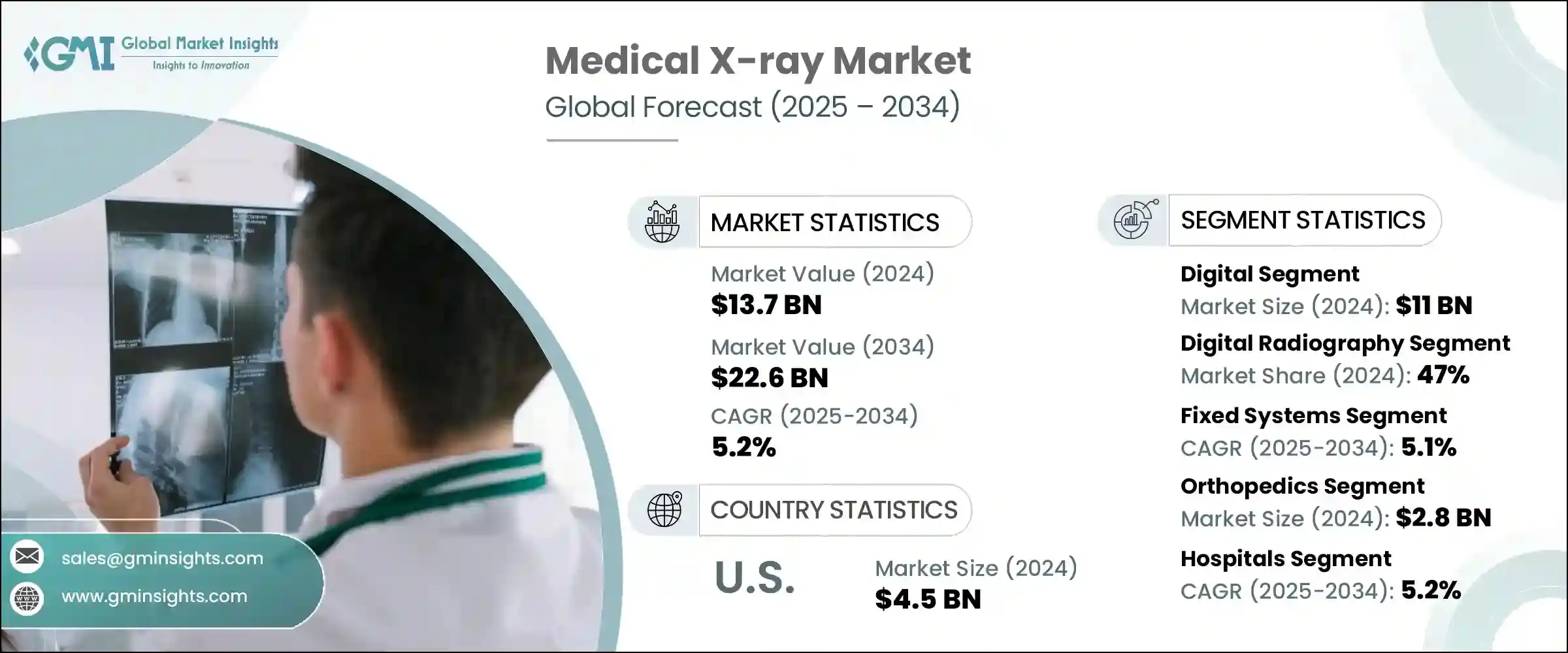

医療用X線の世界市場規模は、2024年に137億米ドルとなり、CAGR 5.2%で成長し、2034年には226億米ドルに達すると予測されています。

医療用X線機器の需要は、主にがん、心血管疾患、呼吸器疾患、神経疾患、筋骨格系疾患などの慢性疾患の有病率の上昇によって牽引されています。これらの疾患に対して早期かつ正確な診断を必要とする患者が増加しているため、医療用X線機器は必要不可欠な診断ツールとなっています。X線画像診断は、骨、臓器、組織の腫瘍、骨折、異常の発見に役立ちます。また、世界の人口の増加と高齢化も、特に高齢者の加齢関連疾患に対する画像診断ニーズの高まりに寄与しています。これらの要因が相まって、市場の拡大に拍車をかけています。

さらに、医療用X線は、さまざまな慢性疾患やその他の医療問題の診断に重要な役割を果たしています。骨、臓器、軟部組織などの体内構造の高解像度画像を提供し、骨折、腫瘍、感染症、各種臓器の異常の特定に不可欠です。これらの詳細な画像は、医師が怪我や病気の重症度を評価し、進行中の治療をモニターし、必要に応じて外科的介入を計画するのに役立ちます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 137億米ドル |

| 予測金額 | 226億米ドル |

| CAGR | 5.2% |

さらに、X線技術は早期発見に不可欠であり、ヘルスケアプロバイダーは、より深刻な健康リスクに発展する前に問題を特定することができます。非侵襲的で正確な結果が得られるX線技術は、正確な診断と効果的な治療計画に不可欠なツールです。デジタルX線システムの進歩に伴い、画像の鮮明度と診断能力は向上し続けており、医師は患者の治療について十分な情報に基づいた意思決定を行いやすくなっています。

デジタルX線分野は、デジタルシステムの技術革新に牽引され、2024年には110億米ドルを創出しました。デジタルX線装置は、正確な診断に不可欠な高解像度と優れたコントラストを備えた優れたイメージング機能を提供します。また、画像の迅速な取り込みと処理が可能なため、患者の待ち時間が大幅に短縮されます。さらに、AIを搭載した画像ソリューションなどの進歩により、診断結果の効率性と一貫性が向上しています。これらの特長により、デジタルX線技術はヘルスケア施設に広く普及しています。X線撮影に関しては、主にデータ管理とアクセシビリティを向上させる最新のITインフラとの統合により、デジタルシステムの普及が進んでいます。

病院分野は、2034年までCAGR 5.2%で成長すると予測されます。開発途上地域と先進地域の両方における病院数の増加は、人口増加、慢性疾患の有病率の増加、医療画像技術の進歩などの要因によってもたらされています。これらの要因が相まって、新設の病院や既存のヘルスケア施設の両方で、最先端の医療用X線システムに対する需要が高まっています。さらに、中東・アフリカ、アジア太平洋などの地域では、医療インフラが拡大しているため、病院での高度な医療用X線技術の採用が加速しています。

欧州の医療用X線市場規模は2024年に38億米ドル。この成長の背景には、慢性疾患の罹患率の上昇と、同地域の政府によるヘルスケアインフラの改善への継続的な取り組みがあります。さらに、X線技術、特にデジタルシステムとポータブルシステムの進歩が欧州の市場成長をさらに促進します。また、この地域には大手市場参入企業が存在することも、欧州の競争力を強化しています。同地域で事業を展開する企業は、革新的なソリューションに積極的に投資し、提供する製品を継続的にアップグレードしており、市場全体の拡大に貢献しています。

世界の医療用X線市場の主要企業には、Agfa-Gevaert Group、Allengers Medical Systems、Canon、Carestream Health、Dentsply Sirona、Fujifilm Holdings Corporation、GE Healthcare Technologies、Hologic、Koninklijke Philips N.V.、Konica Minolta、Midmark、Neusoft Medical Systems、Perlong Medical Equipment、Samsung Electronics、Shimadzu、Siemens Healthineers、Trivitron Healthcareなど、さまざまな企業が名を連ねています。競争の激しい市場競争での地位を固めるため、各社はいくつかの戦略的イニシアティブに注力しています。診断精度を高めるAI機能を備えたデジタルX線システムなど、先進的な画像ソリューションを市場に投入するために研究開発に多額の投資を行っています。

さらに、各社は自社製品をITインフラと統合することを優先しており、データへのアクセス性、保存性、管理性を高めています。また、ヘルスケアプロバイダーに高い柔軟性と利便性を提供するため、多くの企業がポータブルX線システムやワイヤレスX線システムを開発しています。従来のフィルム処理が不要なデジタルX線撮影ソリューションによるコスト削減も、コスト意識の高い医療機関にアピールするために採用されている戦略です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 先進国における画像診断技術の進歩

- 世界中で慢性疾患の有病率が上昇

- 診断画像検査の増加

- 医療用X線手続きの償還の有無

- 業界の潜在的リスク&課題

- 高放射線被曝のリスク

- 医療画像診断装置の導入に伴う高コスト

- 市場機会

- 高画質を維持しながら放射線被曝を最小限に抑える低線量X線技術の使用が増えています

- 画像解釈を強化し、診断ミスを削減するためのAI統合X線システムの需要が高まっています

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- デジタル

- アナログ

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- フィルムベースの放射線撮影

- コンピュータラジオグラフィー

- デジタルレントゲン撮影

第7章 市場推計・予測:ポータビリティ別、2021年~2034年

- 主要動向

- 固定システム

- ポータブルシステム

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 歯科

- 口腔内画像

- 口腔外画像

- 獣医

- 腫瘍学

- 整形外科

- 心臓病学

- 神経学

- その他の獣医用途

- マンモグラフィー

- 胸

- 心血管系

- 整形外科

- その他の用途

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 診断センター

- その他の用途

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- 日本

- インド

- ベトナム

- 韓国

- タイ

- オセアニア

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- エジプト

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Agfa-Gevaert Group

- Allengers Medical Systems

- Canon

- Carestream Health

- Dentsply Sirona

- Fujifilm Holdings Corporation

- GE HealthCare Technologies

- Hologic

- Koninklijke Philips N.V.

- Konica Minolta

- Midmark

- Neusoft Medical Systems

- Perlong Medical Equipment

- Samsung Electronics

- Shimadzu

- Siemens Healthineers

- Trivitron Healthcare

The Global Medical X-ray Market was valued at USD 13.7 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 22.6 billion by 2034. The demand for medical X-ray devices is primarily driven by the rising prevalence of chronic diseases, including cancer, cardiovascular issues, respiratory conditions, neurological disorders, and musculoskeletal problems. As more patients require early and precise diagnoses for these conditions, medical X-ray machines have become an essential diagnostic tool. X-ray imaging helps detect tumors, fractures, and abnormalities in bones, organs, and tissues. The growing and aging global population is also contributing to the rise in the need for diagnostic imaging, particularly for age-related conditions in elderly patients. These factors combine to fuel the market's expansion.

Additionally, medical X-rays play a vital role in diagnosing a wide range of chronic conditions and other medical issues. They provide high-resolution images of the body's internal structures, such as bones, organs, and soft tissues, which are essential for identifying fractures, tumors, infections, and abnormalities in various organs. These detailed images help physicians assess the severity of injuries or diseases, monitor ongoing treatments, and plan surgical interventions if necessary.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.7 Billion |

| Forecast Value | $22.6 Billion |

| CAGR | 5.2% |

Furthermore, X-ray technology is indispensable in early detection, allowing healthcare providers to identify problems before they develop into more serious health risks. Its non-invasive nature and ability to deliver precise results make it an indispensable tool for accurate diagnosis and effective treatment planning. With advancements in digital X-ray systems, image clarity, and diagnostic capabilities continue to improve, making it easier for doctors to make informed decisions about patient care.

The digital X-ray segment generated USD 11 billion in 2024 driven by technological innovations in digital systems. Digital X-ray devices offer superior imaging capabilities with high resolution and better contrast, critical for accurate diagnoses. Their ability to quickly capture and process images significantly reduces patient waiting times. Furthermore, advancements like AI-powered imaging solutions are increasing the efficiency and consistency of diagnostic results. These features contribute to the widespread adoption of digital X-ray technology across healthcare facilities. In terms of radiography, digital systems have become increasingly popular, mainly due to their integration with modern IT infrastructure, which improves data management and accessibility.

The hospital segment is expected to grow at a CAGR of 5.2% through 2034. The growth in the number of hospitals, both in developing and developed regions, is being driven by factors such as population growth, the increasing prevalence of chronic diseases, and advancements in medical imaging technologies. These factors are collectively fueling the demand for state-of-the-art medical X-ray systems, both in newly built hospitals and within existing healthcare facilities. Additionally, the expanding healthcare infrastructure in regions like the Middle East, Africa, and Asia Pacific is accelerating the adoption of advanced medical X-ray technologies in hospital settings.

Europe Medical X-ray market was valued at USD 3.8 billion in 2024. This growth can be attributed to the rising incidence of chronic diseases and the ongoing efforts by governments in the region to improve healthcare infrastructure. Additionally, advancements in X-ray technology, particularly in digital and portable systems, will further drive market growth in Europe. The presence of major market players in the region also strengthens Europe's competitive edge. Companies operating in the region are actively investing in innovative solutions and continuously upgrading their offerings, contributing to the overall expansion of the market.

The key players in the Global Medical X-ray market include a diverse range of companies such as Agfa-Gevaert Group, Allengers Medical Systems, Canon, Carestream Health, Dentsply Sirona, Fujifilm Holdings Corporation, GE Healthcare Technologies, Hologic, Koninklijke Philips N.V., Konica Minolta, Midmark, Neusoft Medical Systems, Perlong Medical Equipment, Samsung Electronics, Shimadzu, Siemens Healthineers, and Trivitron Healthcare. To solidify their position in the competitive medical X-ray market, companies are focusing on several strategic initiatives. They are heavily investing in research and development to bring advanced imaging solutions to the market, such as digital X-ray systems with AI capabilities that enhance diagnostic accuracy.

Additionally, companies are prioritizing the integration of their products with IT infrastructure, allowing for better data accessibility, storage, and management. Many players are also developing portable and wireless X-ray systems to offer greater flexibility and convenience to healthcare providers. Cost reduction through digital radiography solutions, which eliminate the need for traditional film processing, is another strategy being employed to appeal to cost-conscious institutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Market scope and definitions

- 1.3 Research design

- 1.3.1 Research approach

- 1.3.2 Data collection methods

- 1.4 Data mining sources

- 1.4.1 Global

- 1.4.2 Regional/Country

- 1.5 Base estimates and calculations

- 1.5.1 Base year calculation

- 1.5.2 Key trends for market estimation

- 1.6 Primary research and validation

- 1.6.1 Primary sources

- 1.7 Forecast model

- 1.8 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Portability

- 2.2.5 Application

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements in diagnostic imaging in developed countries

- 3.2.1.2 Rising prevalence of chronic diseases worldwide

- 3.2.1.3 Growing number of diagnostic imaging procedures

- 3.2.1.4 Presence of reimbursement for medical x-ray procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of high radiation exposure

- 3.2.2.2 High cost associated with installation of medical imaging modalities

- 3.2.3 Market opportunities

- 3.2.3.1 Growing use of low-dose X-ray technologies to minimize radiation exposure while maintaining high image quality.

- 3.2.3.2 Increasing demand for AI-integrated X-ray systems to enhance image interpretation and reduce diagnostic errors.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Digital

- 5.3 Analog

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Film-based radiography

- 6.3 Computed radiography

- 6.4 Digital radiography

Chapter 7 Market Estimates and Forecast, By Portability, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Fixed systems

- 7.3 Portable systems

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Dental

- 8.2.1 Intraoral imaging

- 8.2.2 Extraoral imaging

- 8.3 Veterinary

- 8.3.1 Oncology

- 8.3.2 Orthopedics

- 8.3.3 Cardiology

- 8.3.4 Neurology

- 8.3.5 Other veterinary applications

- 8.4 Mammography

- 8.5 Chest

- 8.6 Cardiovascular

- 8.7 Orthopedics

- 8.8 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Diagnostic centers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Vietnam

- 10.4.5 South Korea

- 10.4.6 Thailand

- 10.4.7 Oceania

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Egypt

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Agfa-Gevaert Group

- 11.2 Allengers Medical Systems

- 11.3 Canon

- 11.4 Carestream Health

- 11.5 Dentsply Sirona

- 11.6 Fujifilm Holdings Corporation

- 11.7 GE HealthCare Technologies

- 11.8 Hologic

- 11.9 Koninklijke Philips N.V.

- 11.10 Konica Minolta

- 11.11 Midmark

- 11.12 Neusoft Medical Systems

- 11.13 Perlong Medical Equipment

- 11.14 Samsung Electronics

- 11.15 Shimadzu

- 11.16 Siemens Healthineers

- 11.17 Trivitron Healthcare