フォグコンピューティングの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Fog Computing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773254

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

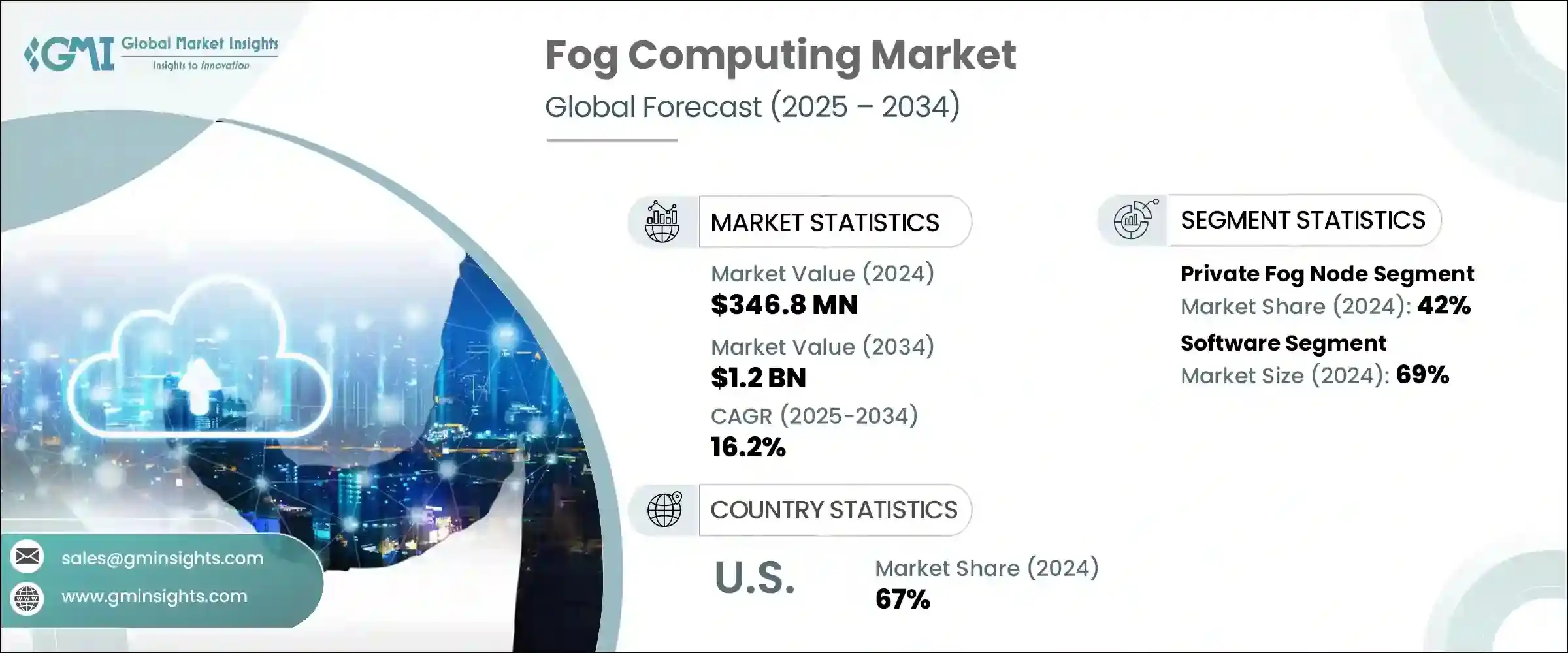

フォグコンピューティングの世界市場規模は、2024年に3億4,680万米ドルとなり、CAGR16.2%で成長し、2034年には12億米ドルに達すると予測されています。

この急拡大の背景には、通信、製造、スマートインフラ、ヘルスケアなどの業界における低遅延通信、分散処理、リアルタイム分析に対する需要の高まりがあります。組織がデジタルトランスフォーメーションへのシフトを続ける中、よりソースに近いところで効率的にデータを処理する必要性が高まっています。フォグコンピューティングは、データ処理の高速化、帯域幅への負荷の軽減、ローカルコンピューティングリソースによる意思決定の強化など、重要な役割を果たしています。接続デバイスの増加とインテリジェントでスケーラブルなソリューションの推進により、フォグコンピューティングは最新のエッジクラウドアーキテクチャのコアコンポーネントとなっています。

フォグコンピューティングは、ローカルストレージ、分析、アクションを可能にし、データの移動距離を短縮することで、従来のクラウドモデルとは一線を画しています。エッジシステムを導入する企業が増えるにつれ、データをオンサイトで遅延なく処理する柔軟なリアルタイム・プラットフォームへの需要が加速しています。特にプライバシーとスピードが重要な、時間的制約のあるデータに依存する業界では、ローカルオペレーションと広範なクラウドシステムの橋渡しをする、信頼性が高く安全なインフラソリューションとして、フォグコンピューティングが急速に注目されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 3億4,680万米ドル |

| 予測金額 | 12億米ドル |

| CAGR | 16.2% |

プライベート・フォグ・ノードの導入は42%のシェアを占め、2034年までのCAGRは17.2%と予測されます。このようなローカライズされたノードにより、企業はインフラストラクチャをより直接的に制御できるようになり、カスタマイズされたパフォーマンス、セキュリティ、コンプライアンス・ソリューションを提供できるようになります。ヘルスケア、防衛、エネルギーなど、重要な業務や機密データを管理する企業は、データガバナンスを確保し、レイテンシを削減しながら、機密ワークロードを独立して安全に処理できるプライベートノードを引き続き支持しています。

2024年のソフトウェア分野のシェアは69%。産業がニッチ技術からエッジインテリジェンスの重要な原動力へと進化するにつれ、堅牢なフォグコンピューティングソフトウェアが不可欠となります。企業は、複雑なエッジ・エコシステム全体でシームレスな管理と展開を可能にするオーケストレーション・ツール、分析プラットフォーム、仮想化技術への依存度を高めています。これらのプラットフォームは、分散したインフラ全体で一貫したパフォーマンスをサポートし、エッジ環境からの迅速で正確な洞察に依存する企業のオペレーションを合理化します。

米国のフォグコンピューティング市場は67%のシェアを占め、2024年には1億1,420万米ドルを創出。強力なデジタルインフラ、急速に進むイノベーションエコシステム、ローカライズされた処理に対する企業の需要の高まりにより、同国はこの分野のフロントランナーとして位置づけられています。フォグコンピューティングは現在、リアルタイムデータが不可欠な分野の事業戦略に不可欠なものとなっており、効率性の向上と即時対応能力を通じて競争優位性を提供しています。

フォグコンピューティング市場の主要企業には、シュナイダー、ARMホールディングス、フォグホーン、シスコ、インテル、富士通、GE、マイクロソフト、IBM、デルなどがあります。フォグコンピューティング分野の企業は、市場の足場を強化するために重要な戦略を活用しています。エッジ・デバイス・メーカーやクラウド・サービス・プロバイダーとの戦略的協業は、ベンダーがリーチを広げ、プラットフォーム間のシームレスな統合を可能にするのに役立っています。

各社は、高度なオーケストレーション・ソフトウェア、セキュリティ・プロトコル、AIを活用した分散環境向け自動化機能を開発するため、研究開発に多額の投資を行っています。また、特にエネルギー、ヘルスケア、製造業など、業界固有の使用事例に対応したフォグ・ソリューションのカスタマイズも増加しています。多くの企業が、高まるパフォーマンスとコンプライアンスへの要求に応えるため、クラウドとフォグのハイブリッドモデルへと移行しています。さらに、政府やスマートシティ開発企業との提携により、新たな展開の機会が生まれています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- IoTデバイスの拡大

- リアルタイムのデータ処理と分析に対する需要の高まり

- 低遅延処理の必要性

- 5Gネットワークの台頭

- インダストリー4.0の導入

- 業界の潜在的リスク&課題

- 標準化の欠如

- 初期費用が高め

- 市場機会

- IoTとエッジデバイスの統合

- スマートエネルギーとユーティリティ

- 促進要因

- 成長可能性分析

- 規制情勢

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許分析

- コスト内訳分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- ゲートウェイ

- ルーターとスイッチ

- IPビデオカメラ

- センサー

- マイクロデータセンサー

- ソフトウェア

- フォグコンピューティングプラットフォーム

- カスタマイズされたアプリケーションソフトウェア

第6章 市場推計・予測:展開モデル別、2021年~2034年

- 主要動向

- Bプライベートフォグノード

- コミュニティフォグノード

- パブリックフォグノード

- ハイブリッドフォグノード

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- セキュリティ

- インテリジェントエネルギー

- スマート製造

- 交通と物流

- コネクテッドヘルス

- ビル&ホームオートメーション

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

第9章 企業プロファイル

- ADLINK

- Amazon Web Services

- ARM Holdings

- Cisco Systems

- Cradlepoint

- Dell

- FogHorn

- Fujitsu

- GE

- Hitachi

- Huawei

- IBM

- Intel

- MachineShop

- Microsoft

- Nebbiolo

- SAP

- Schneider

- Toshiba

- Zebra

目次

The Global Fog Computing Market was valued at USD 346.8 million in 2024 and is estimated to grow at a CAGR of 16.2% to reach USD 1.2 billion by 2034. This rapid expansion is being fueled by rising demand for low-latency communication, decentralized processing, and real-time analytics across industries such as telecom, manufacturing, smart infrastructure, and healthcare. As organizations continue to shift toward digital transformation, the need for efficient data handling closer to the source is growing. Fog computing plays a critical role by enabling faster data processing, reducing pressure on bandwidth, and enhancing decision-making through local computing resources. The increasing number of connected devices and the push for intelligent, scalable solutions are making fog computing a core component of modern edge-cloud architectures.

Fog computing enables local storage, analysis, and action, distinguishing itself from traditional cloud models by reducing the distance data must travel. As more organizations deploy edge systems, demand for flexible, real-time platforms that process data on-site without delays is accelerating. Industries relying on time-sensitive data, particularly where privacy and speed are key, are rapidly turning to fog computing as a dependable and secure infrastructure solution that bridges local operations and broader cloud systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $346.8 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 16.2% |

Private fog node deployments segment 42% share and is projected to grow at a CAGR of 17.2% through 2034. These localized nodes give enterprises more direct control over infrastructure, offering tailored performance, security, and compliance solutions. Businesses managing critical operations or sensitive data, including those in healthcare, defense, and energy, continue to favor private nodes for their ability to handle confidential workloads independently and securely while ensuring data governance and reducing latency.

The software segment held a 69% share in 2024. As industry evolves from a niche technology to a key driver of edge intelligence, robust fog computing software becomes essential. Companies increasingly rely on orchestration tools, analytics platforms, and virtualization technologies that allow seamless management and deployment across complex edge ecosystems. These platforms support consistent performance across distributed infrastructures, streamlining operations for enterprises that rely on fast, accurate insights from their edge environments.

United States Fog Computing Market held a 67% share and generated USD 114.2 million in 2024. Strong digital infrastructure, a fast-moving innovation ecosystem, and growing enterprise demand for localized processing have positioned the country as a frontrunner in this space. Fog computing is now integral to operational strategies in sectors where real-time data is vital, offering a competitive advantage through improved efficiency and immediate response capabilities.

Major companies in the Fog Computing Market include Schneider, ARM Holdings, FogHorn, Cisco, Intel, Fujitsu, GE, Microsoft, IBM, and Dell. Companies in the fog computing sector are leveraging key strategies to enhance their market foothold. Strategic collaborations with edge device manufacturers and cloud service providers are helping vendors extend their reach and enable seamless integration across platforms.

Firms are heavily investing in R&D to develop advanced orchestration software, security protocols, and AI-powered automation for distributed environments. Customization of fog solutions for industry-specific use cases, especially in energy, healthcare, and manufacturing, is also on the rise. Many businesses are transitioning toward hybrid cloud-fog models to meet growing performance and compliance demands. Additionally, partnerships with governments and smart city developers are unlocking new deployment opportunities.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of IoT devices

- 3.2.1.2 Growing demand for real-time data processing and analytics

- 3.2.1.3 Need for low-latency processing

- 3.2.1.4 Rise of 5G networks

- 3.2.1.5 Industry 4.0 adoption

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Lack of standardization

- 3.2.2.2 High initial costs

- 3.2.3 Market opportunities

- 3.2.3.1 IoT and edge device integration

- 3.2.3.2 Smart energy and utilities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Gateways

- 5.2.2 Routers & switches

- 5.2.3 IP video cameras

- 5.2.4 Sensors

- 5.2.5 Micro data sensors

- 5.3 Software

- 5.3.1 Fog computing platform

- 5.3.2 Customized application software

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 B Private fog node

- 6.3 Community fog node

- 6.4 Public fog node

- 6.5 Hybrid fog node

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Security

- 7.3 Intelligent energy

- 7.4 Smart manufacturing

- 7.5 Traffic & logistics

- 7.6 Connected health

- 7.7 Building & home automation

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 ADLINK

- 9.2 Amazon Web Services

- 9.3 ARM Holdings

- 9.4 Cisco Systems

- 9.5 Cradlepoint

- 9.6 Dell

- 9.7 FogHorn

- 9.8 Fujitsu

- 9.9 GE

- 9.10 Hitachi

- 9.11 Huawei

- 9.12 IBM

- 9.13 Intel

- 9.14 MachineShop

- 9.15 Microsoft

- 9.16 Nebbiolo

- 9.17 SAP

- 9.18 Schneider

- 9.19 Toshiba

- 9.20 Zebra

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日