|

市場調査レポート

商品コード

1773246

ヒアルロン酸の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Hyaluronic Acid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ヒアルロン酸の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月30日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

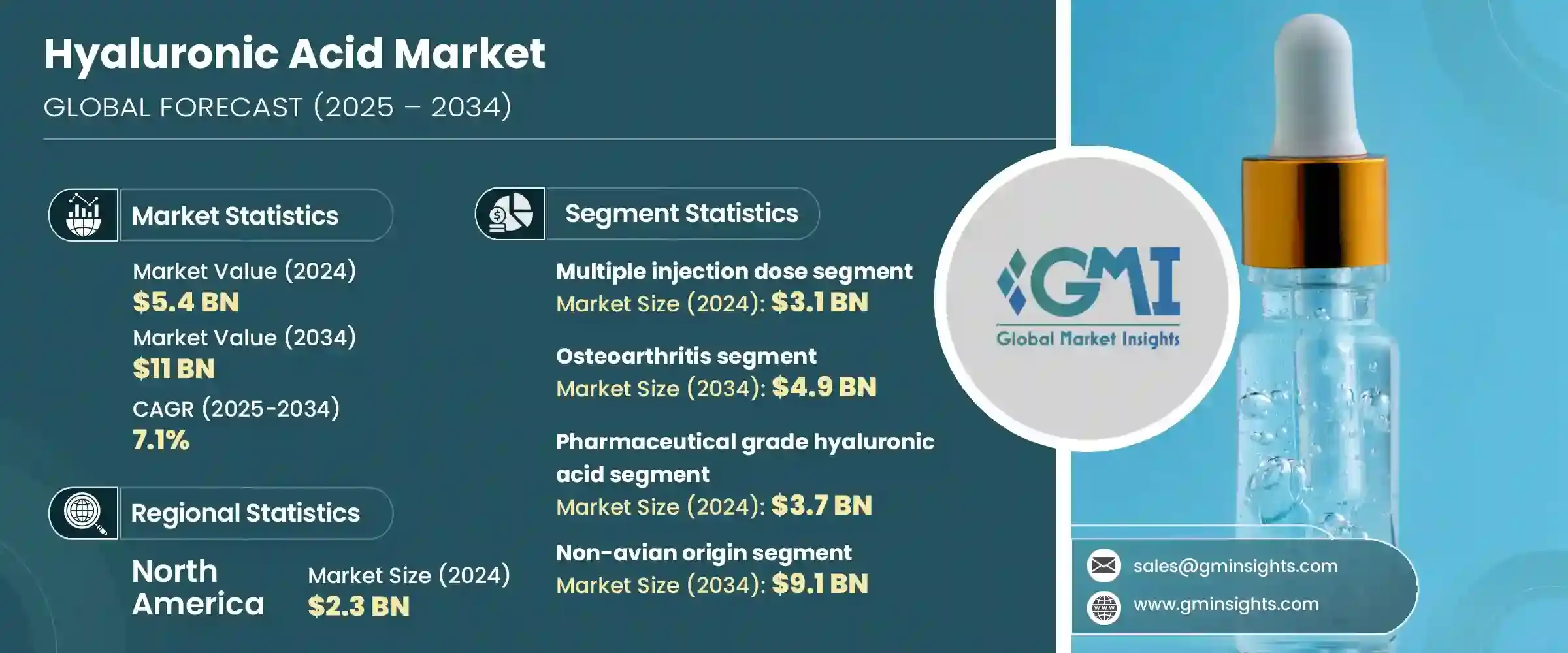

ヒアルロン酸の世界市場規模は、2024年には54億米ドルとなり、CAGR 7.1%で成長し、2034年には110億米ドルに達すると予測されています。

この上昇傾向に拍車をかけている主な要因のひとつは、医薬品と化粧品の両領域におけるヒアルロン酸ベースの製剤の急速な開発です。身だしなみへの関心の高まり、美容施術の増加、低侵襲治療への需要の高まりが、HA製品にとって肥沃な環境を作り出しています。また、より早く結果が得られ、副作用の少ない治療への嗜好の変化も目に見えています。若年層は、セルフイメージ意識の高まりやデジタル文化の影響もあって、美容整形に積極的に取り組んでいます。同時に、世界の高齢化により、関節に関連する疾患の管理におけるHAへのニーズが高まっています。

医療分野、特に整形外科では、HA注射は関節のこわばりや痛みを和らげる方法として広く受け入れられています。特に股関節と膝関節における変形性関節症の増加により、HAを関節に直接注入する技術である関節内補充療法を選択する患者の数が増加しています。このアプローチは関節の潤滑を回復させ、摩擦を減らすのに役立ち、関節置換術に代わる侵襲の少ない方法を提供します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 54億米ドル |

| 予測金額 | 110億米ドル |

| CAGR | 7.1% |

患者が手術を遅らせたり避けたりする治療法を求める中、ヒアルロン酸注射の需要は一貫した成長を見せています。HAは結合組織や滑液中に天然に存在する物質であるため、医療用途ではさらに優位性を発揮し、衝撃吸収剤や潤滑剤として機能し、関節の可動性と快適性を向上させる。さらに、その特性は創傷治癒製品やスキンケアのような外部用途にも利用され、その商業的範囲はさらに多様化しています。

製品タイプ別では、市場は複数回注射タイプと単回注射タイプに分かれます。2024年の世界市場は、複数回注射投与型が31億米ドルを占め、優位を占めています。このタイプは、長期間にわたって関節の不快感を軽減する効果が実証されているため、変形性関節症を管理する臨床医や患者の間で依然として人気があります。通常、治療プロトコールでは、特に中等度から重度の関節機能低下を経験している患者に対して、持続的な緩和を提供する注射を週1回連続して行う。これらの製品は、豊富な臨床データに裏打ちされ、一般的に保険が適用され、安全性と有効性の実績から支持されています。

用途別に分析すると、変形性関節症分野が市場を牽引し、2034年には約49億米ドルに達すると予測されています。高齢化社会の中で関節痛が増加し続ける中、症状を管理するためにHAをベースとした解決策を模索する人が増えています。ヒアルロン酸は、従来の鎮痛剤や内服薬では効果が限定的な場合に特に評価されます。これらの注射の低侵襲性は、関節機能を回復させ外科的介入の必要性を遅らせる能力とともに、ますます魅力的な選択肢となっています。

グレード別では、医薬品グレードのヒアルロン酸が2024年の評価額が約37億米ドルとなり、支配的なカテゴリーに浮上しました。このグレードは、制御された分子量や強化された生体適合性など、その厳しい品質基準から高い人気があります。関節注射、眼科手術、ドラッグデリバリーシステムなどの治療に広く使用されています。高純度で安全性が高いため、注射剤としての使用が可能で、臨床現場での採用が拡大しています。

エンドユーザーについては、病院が2024年に最大のシェアを占め、予測期間中も堅調な需要が続くと予想されます。これらの施設は、特に整形外科、眼科、美容外科病棟において、HAベースの治療法の採用において極めて重要な役割を果たしています。熟練したヘルスケア提供者の集中、支援的な償還の枠組み、そして規制の明確化が、病院におけるHA製品使用の主要な推進力となっています。医療行為が非侵襲的あるいは低侵襲的介入をますます好むようになるにつれ、医薬品グレードのヒアルロン酸への依存は強まり続けています。

米国では、市場は強い勢いを見せています。2021年の16億米ドルから2022年には17億米ドルに増加し、2024年には21億米ドルに達します。この成長は、変形性関節症の有病率の高さ、美容施術の普及、関節内補充療法注射をカバーする有利な保険政策を反映しています。同国は、医療需要と美容技術革新の組み合わせによって、HAにとって最も成熟した市場のひとつであり続けています。

市場企業は製品の性能とユーザーの利便性の向上に注力しています。Allergan Aesthetics社、Anika Therapeutics社、Ferring Pharmaceuticals社、BLOOMAGE社、Bioventus社を含む主要企業は、治療レジメンの簡素化を目的とした単回投与オプションを含む先進的製剤への投資を行っています。これらの企業は合計で世界市場シェアの40%以上を占めています。顕著な業界動向は、安全性、純度、患者適合性を向上させる細菌発酵によって生産された非アビアンHAへの嗜好の高まりです。競争力を維持するためには、企業は進化する規制に対応し、実際の使用データを作成し、エビデンスに基づいた製品採用をサポートするために医療従事者との積極的な関わりを維持する必要があります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 変形性関節症の有病率の増加

- 美容施術件数の増加

- 低侵襲手術の需要増加

- HAベース製品の技術的進歩

- 業界の潜在的リスク&課題

- 治療費が高め

- 潜在的な有害反応と副作用

- 機会

- 医療ツーリズムの拡大

- eコマースと遠隔皮膚科の統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 製品別の価格動向

- 将来の市場動向

- 償還シナリオ

- 消費者行動分析

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- 世界のその他の地域

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 複数回注射投与

- 単回注射用量

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 変形性関節症

- 皮膚充填剤

- 眼科

- 膀胱尿管逆流症

- その他の用途

第7章 市場推計・予測:グレード別、2021年~2034年

- 主要動向

- 医薬品グレードヒアルロン酸

- 化粧品グレードヒアルロン酸

第8章 市場推計・予測:由来別、2021年~2034年

- 主要動向

- 非鳥類起源

- 鳥類起源

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 皮膚科クリニック

- 外来手術センター

- その他の用途

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Allergan Aesthetics

- altergon

- ANIKA

- bioventus

- BLOOMAGE

- FERRING PHARMACEUTICALS

- GALDERMA

- kewpie

- LG Chem

- Lifecore BIOMEDICAL

- Roche

- Sanofi

- SEIKAGAKU CORPORATION

- Teleflex(Deflux)

- TOPSCIENCE

The Global Hyaluronic Acid Market was valued at USD 5.4 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 11 billion by 2034. One of the core factors fueling this upward trend is the rapid development of hyaluronic acid-based formulations across both pharmaceutical and cosmetic domains. The increasing focus on personal appearance, growing uptake of aesthetic procedures, and rising demand for minimally invasive treatments have created a fertile landscape for HA products. There is also a visible shift in public preference towards treatments that offer faster results and fewer side effects. Younger populations are engaging more with cosmetic enhancements, largely influenced by greater self-image awareness and digital culture. At the same time, aging demographics globally are creating a growing need for HA in managing joint-related conditions.

In the medical sector, particularly in orthopedics, HA injections have become a widely accepted method for alleviating joint stiffness and pain. The rising incidence of osteoarthritis-particularly in hips and knees-has increased the number of patients opting for viscosupplementation, a technique where HA is injected directly into the joints. This approach helps restore joint lubrication and reduce friction, offering a less invasive alternative to joint replacement surgeries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.4 Billion |

| Forecast Value | $11 Billion |

| CAGR | 7.1% |

As patients seek treatments that delay or avoid surgery, demand for hyaluronic acid injections is seeing consistent growth. HA's role as a naturally occurring substance in connective tissues and synovial fluids gives it an added edge in medical applications, where it functions as a shock absorber and lubricant, improving joint mobility and comfort. Additionally, its properties are being harnessed in external applications like wound healing products and skincare, further diversifying its commercial reach.

In terms of product segmentation, the market is split into multiple injection dose and single injection dose types. The multiple injection dose segment dominated the global market in 2024, accounting for USD 3.1 billion. This form remains popular among clinicians and patients managing osteoarthritis due to its proven efficacy in reducing joint discomfort over a longer duration. Typically, treatment protocols involve a series of weekly injections that offer sustained relief, especially for those experiencing moderate to severe joint degradation. These products are backed by a wealth of clinical data, are generally covered by insurance, and are favored for their track record of safety and effectiveness.

When analyzed by application, the osteoarthritis segment led the market and is projected to reach approximately USD 4.9 billion by 2034. As joint pain continues to rise among aging populations, more individuals are exploring HA-based solutions to manage symptoms. Hyaluronic acid is especially valued in cases where conventional pain relievers and oral medications provide limited results. The minimally invasive nature of these injections, along with their ability to restore joint function and delay the need for surgical intervention, makes them an increasingly attractive option.

On the basis of grade, pharmaceutical-grade hyaluronic acid emerged as the dominant category, with a valuation of around USD 3.7 billion in 2024. This grade is highly sought-after for its stringent quality standards, including controlled molecular weight and enhanced biocompatibility. It is extensively used in treatments such as joint injections, ocular surgeries, and controlled drug delivery systems. Its high purity and safety profile enable its use in injectable formats, expanding its adoption across clinical settings.

Regarding end users, hospitals accounted for the largest share in 2024 and are expected to continue seeing robust demand over the forecast period. These institutions play a pivotal role in the adoption of HA-based therapies, particularly in orthopedic departments, ophthalmology units, and cosmetic surgery wards. The concentration of skilled healthcare providers, supportive reimbursement frameworks, and regulatory clarity are key drivers for HA product use in hospitals. As medical practices increasingly favor non-invasive or minimally invasive interventions, the reliance on pharmaceutical-grade hyaluronic acid continues to strengthen.

In the United States, the market has shown strong momentum. From USD 1.6 billion in 2021, it rose to USD 1.7 billion in 2022, reaching USD 2.1 billion by 2024. This growth reflects the high prevalence of osteoarthritis, widespread adoption of aesthetic procedures, and favorable insurance policies that cover viscosupplementation injections. The country remains one of the most mature markets for HA, driven by a combination of medical demand and cosmetic innovation.

Market players are focused on improving product performance and user convenience. Key companies, including Allergan Aesthetics, Anika Therapeutics, Ferring Pharmaceuticals, BLOOMAGE, and Bioventus, are channeling investments into advanced formulations, including single-dose options aimed at simplifying treatment regimens. These firms collectively represent over 40% of the global market share. A prominent industry trend is the growing preference for non-avian HA produced via bacterial fermentation, which offers enhanced safety, purity, and patient compatibility. Staying competitive requires companies to align with evolving regulations, generate real-world usage data, and maintain active engagement with healthcare professionals to support evidence-based product adoption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 Grade

- 2.2.5 Source of origin

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of osteoarthritis

- 3.2.1.2 Rise in number of aesthetic procedures

- 3.2.1.3 Growing demand for minimally invasive procedures

- 3.2.1.4 Technological advancements in HA-based products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Potential adverse reactions and side effects

- 3.2.3 Opportunities

- 3.2.3.1 Expanding medical tourism

- 3.2.3.2 E-commerce and teledermatology integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends, by product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.9 Consumer behaviour analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Rest of the world

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Multiple injection dose

- 5.3 Single injection dose

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Osteoarthritis

- 6.3 Dermal fillers

- 6.4 Ophthalmic

- 6.5 Vesicoureteral reflux

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Grade, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pharmaceutical grade hyaluronic acid

- 7.3 Cosmetic grade hyaluronic acid

Chapter 8 Market Estimates and Forecast, By Source of Origin, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Non-Avian origin

- 8.3 Avian origin

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Dermatology clinics

- 9.4 Ambulatory surgical centers

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Allergan Aesthetics

- 11.2 altergon

- 11.3 ANIKA

- 11.4 bioventus

- 11.5 BLOOMAGE

- 11.6 FERRING PHARMACEUTICALS

- 11.7 GALDERMA

- 11.8 kewpie

- 11.9 LG Chem

- 11.10 Lifecore BIOMEDICAL

- 11.11 Roche

- 11.12 Sanofi

- 11.13 SEIKAGAKU CORPORATION

- 11.14 Teleflex (Deflux)

- 11.15 TOPSCIENCE