|

市場調査レポート

商品コード

1773237

アスファルト乳化剤の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Bitumen Emulsifiers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| アスファルト乳化剤の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月20日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

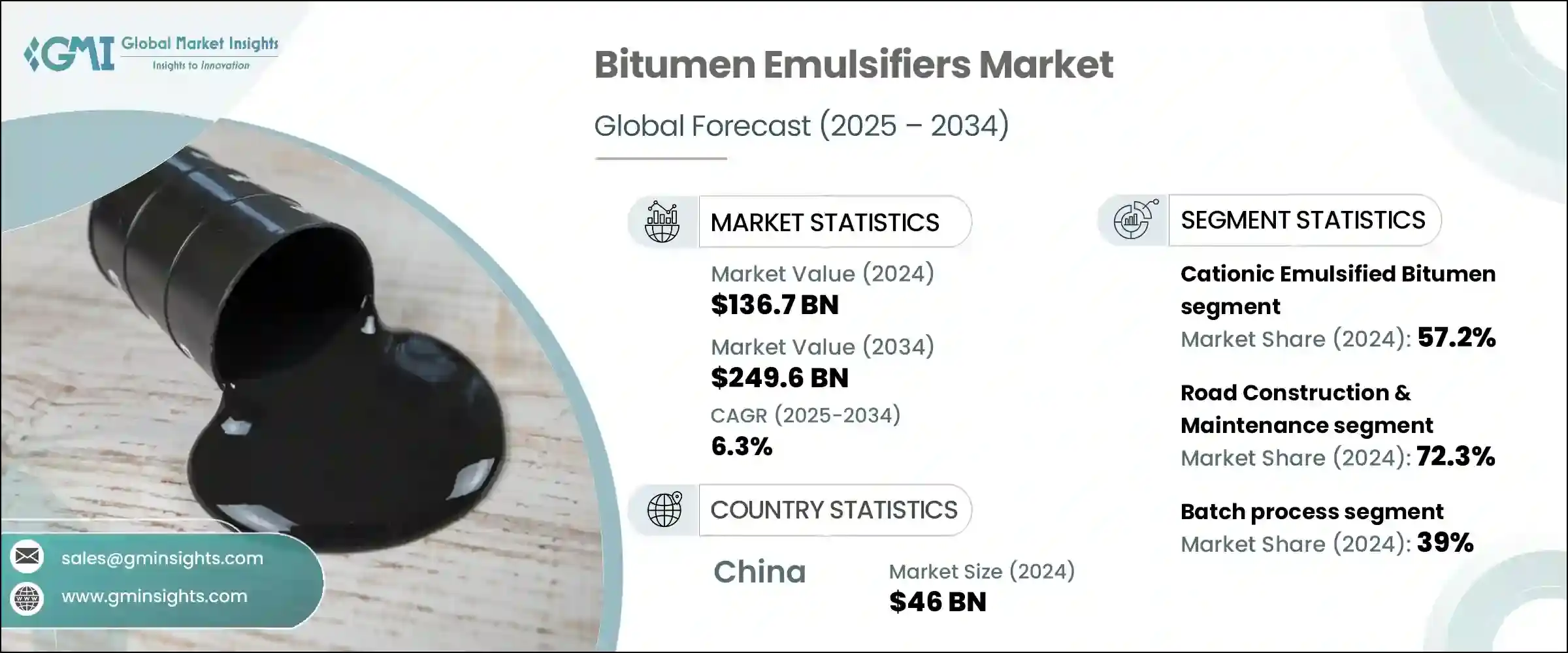

アスファルト乳化剤の世界市場規模は、2024年に1,367億米ドルとなり、CAGR 6.3%で成長し、2034年には2,496億米ドルに達すると予測されています。

この成長の主な要因は、インフラへの投資の増加、特に課題の多い地形における政府の大規模な取り組みです。アスファルト乳化剤は、寒冷地での使用や悪天候への強い耐性によりこれらのプロジェクトに好まれ、長持ちする道路建設やメンテナンスに理想的です。水性製剤は炭化水素の排出を大幅に削減し、加熱の必要性をなくすため、世界各地の厳しい環境・安全規制に適合しています。

このような環境に優しい利点により、特にカーボンニュートラルと労働安全を優先する地域では、持続可能な建設慣行におけるアスファルト乳化剤の採用が大幅に加速しています。乳化剤は塗布時の高温加熱が不要なため、燃料消費量とそれに伴う温室効果ガス排出量を大幅に削減します。このようなエネルギー使用量の削減は、グリーン・インフラやネット・ゼロ目標に向けた世界のシフトに合致します。さらに、低温塗布という性質により、火災の危険性や作業員が有害なガスにさらされるリスクを最小限に抑え、建設現場の安全性を高めることができます。北米、欧州、アジア太平洋地域の政府や規制機関は、公共インフラプロジェクトにおいて低VOCで環境に配慮した材料の使用を義務付けるようになってきており、従来のアスファルトに代わる、より安全でクリーンかつ効率的な材料として、アスファルト乳化剤の需要がさらに高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,367億米ドル |

| 予測金額 | 2,496億米ドル |

| CAGR | 6.3% |

カチオン系アスファルト乳化剤分野は2024年の市場シェア57.2%で圧倒的な地位を占めており、その主な理由はマイナスに帯電した骨材表面との優れた接着能力にあります。この優れた接着力により、交通量が多く天候が変化しやすい路面の耐久性と弾力性が向上します。また、カチオン配合は汎用性があるため、山岳地帯から沿岸気候まで、さまざまな建設環境に適しています。さまざまな温度や水分レベルの下で安定した性能を発揮することから、特に大規模な都市開発や主要道路インフラ・プロジェクトでの需要が続いています。

2024年の道路建設・保守セグメントのシェアは72.3%でした。アスファルト乳化剤は、タックコート、パッチングコンパウンド、チップシール、表面ドレッシングに広く使用されているため、現代の舗装作業において重要です。その低温塗布特性により、作業上の危険性が軽減され、低温条件下でも施工が可能になるため、エネルギー使用量とプロジェクトの遅延が削減されます。このような利点から、特に交通量の多い道路や迅速な復旧工事など、新設工事と日常的な維持管理の両方に理想的な製品となっています。また、硬化が早いため、都市部では不可欠な交通の混乱も最小限に抑えることができます。

中国のアスファルト乳化剤2024年の市場規模は460億米ドル。同国では、国道、農村道路、スマートシティ回廊などの交通インフラへの投資が続いており、高性能アスファルト乳化剤の普及に拍車をかけています。持続可能な低排出ガス建設に重点を置く政府のイニシアチブは、VOCの放出が少なくエネルギー消費量も少ない低温乳化アスファルトの環境面での利点とさらに合致しています。長期的な戦略的インフラプロジェクトが実施される中、環境にやさしく耐久性のある道路資材の需要は増加し、市場成長の最前線における中国の地位はさらに強化されるものと思われます。

アスファルト乳化剤業界に影響を与える主な企業は、Ingevity Corporation、Arkema Group、Evonik Industries AG、Nouryon、BASF SEなどです。これらの企業は、継続的な製品開発と市場開拓を通じて競合環境を形成しています。アスファルト乳化剤分野の企業は、その地位を強化するため、気候や環境の変化に対応する高度な配合の研究開発を優先しています。また、地域の流通網を拡大し、道路建設会社や公共インフラ機関と戦略的パートナーシップを結んでいます。持続可能性は中核的な焦点であり、企業は環境に優しい低VOC乳化剤への投資を増やし、グリーン建設義務に適合するソリューションを推進しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- インフラ開発の増加

- 環境上の利点と規制

- 費用対効果

- 技術的進歩

- 業界の潜在的リスク&課題

- 適用温度範囲が限られている

- 保管安定性に関する懸念

- ホットミックスアスファルトに比べて強度が低い

- 変動する原油価格

- 市場機会

- 新興国における需要の増加

- 持続可能な建設への注目が高まる

- バイオベース乳化剤の開発

- コールドリサイクル技術の採用増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- カチオン系アスファルト乳化剤

- 急速設定(CRS)

- 中速設定(CMS)

- 低速設定(CSS)

- アニオン性アスファルト乳化剤

- 急速設定(RS)

- 中速設定(MS)

- 低速設定(SS)

- 非イオン性アスファルト乳化剤

- 変更されたアスファルト乳化剤

- ポリマー改質

- SBS修正

- SBR改良

- その他

- ラテックス改質

- その他

- ポリマー改質

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 道路建設とメンテナンス

- 表面ドレッシング

- タックコート

- プライムコート

- スラリーシール

- マイクロサーフェシング

- コールドミックスアスファルト

- フォグシール

- チップシール

- 防水

- 建築工事

- インフラストラクチャー

- 舗装リサイクル

- 全深度埋め立て(FDR)

- コールドインプレースリサイクル(CIR)

- コールドセントラルプラントリサイクル(CCPR)

- その他

- 土壌安定化

- 接着剤

- 産業用途

第7章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 道路・高速道路建設

- 空港建設

- 建築工事

- 住宅用

- 商業用

- 産業用

- その他

- 鉄道

- 海洋

- 農業

第8章 市場推計・予測:製造工程別、2021年~2034年

- 主要動向

- バッチ処理

- 連続プロセス

- 半連続プロセス

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Alternative Environmental Technologies(AET)

- Arkema Group

- BASF SE

- Bharat Petroleum Corporation Limited(BPCL)

- BTBA

- Dow Chemical Company

- Evonik Industries AG

- GlobeCore

- Hindustan Colas Limited(HINCOL)

- Hindustan Petroleum Corporation Limited(HPCL)

- Ingevity Corporation

- Jey Oil Refining Company

- Kao Corporation

- Marathon Petroleum Asphalt &Emulsions

- Nouryon

- Nynas AB

- Petro Naft

- Pro-Road Global

- Royal Dutch Shell plc

- Tiki Tar Industries

- Total Energies SE

- Winstrol Petrochemicals Pvt. Ltd.

The Global Bitumen Emulsifiers Market was valued at USD 136.7 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 249.6 billion by 2034. This growth is primarily driven by increased investment in infrastructure, particularly large-scale government initiatives across challenging terrains. Bitumen emulsifiers are preferred for these projects due to their cold application and strong resistance to adverse weather, making them ideal for long-lasting road construction and maintenance. Their water-based formulation significantly reduces hydrocarbon emissions and eliminates the need for heating, aligning well with stricter environmental and safety regulations across global regions.

These eco-friendly benefits have significantly accelerated the adoption of bitumen emulsifiers in sustainable construction practices, particularly in regions prioritizing carbon neutrality and occupational safety. Since emulsifiers eliminate the need for high-temperature heating during application, they drastically lower fuel consumption and associated greenhouse gas emissions. This reduction in energy usage aligns with the global shift toward green infrastructure and net-zero targets. Additionally, their cold-application nature minimizes risks of fire hazards and worker exposure to harmful fumes, enhancing safety on construction sites. Governments and regulatory bodies across North America, Europe, and Asia-Pacific are increasingly mandating the use of low-VOC and environmentally responsible materials in public infrastructure projects, which has further reinforced the demand for bitumen emulsifiers as a safer, cleaner, and more efficient alternative to conventional asphalt.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $136.7 Billion |

| Forecast Value | $249.6 Billion |

| CAGR | 6.3% |

The cationic bitumen emulsifiers segment held the dominant position with a 57.2% market share in 2024, largely attributed to its excellent bonding ability with negatively charged aggregate surfaces. This superior adhesion ensures better durability and resilience of road surfaces under heavy traffic and shifting weather conditions. Cationic formulations also offer versatility, making them highly suitable for a range of construction environments-from mountainous terrains to coastal climates. Their consistent performance under various temperature and moisture levels continues to drive their demand, particularly in large-scale urban development and major roadway infrastructure projects.

The road construction and maintenance segment held a 72.3% share in 2024. Bitumen emulsifiers are critical in modern paving operations as they are widely used in tack coats, patching compounds, chip seals, and surface dressings. Their cold-application properties reduce operational hazards and allow construction even in low-temperature conditions, cutting down on energy usage and project delays. These advantages make them ideal for both new construction and routine maintenance, especially for high-traffic roads and rapid rehabilitation efforts. Their quick-setting nature also minimizes traffic disruptions, which is essential in urban areas.

China Bitumen Emulsifiers Market generated USD 46 billion in 2024. The country's ongoing investments in transportation infrastructure-including national highways, rural roads, and smart city corridors-have fueled the widespread adoption of high-performance bitumen emulsifiers. Government initiatives focused on sustainable, low-emission construction practices further align with the environmental benefits of cold-applied emulsified bitumen, which releases fewer VOCs and requires less energy. With long-term strategic infrastructure projects in place, the demand for eco-friendly, durable road materials is set to increase, reinforcing China's position at the forefront of market growth.

Key players influencing the Bitumen Emulsifiers Industry include Ingevity Corporation, Arkema Group, Evonik Industries AG, Nouryon, and BASF SE. These companies shape the competitive environment through ongoing product development and market expansion. To strengthen their position, companies in the bitumen emulsifiers space are prioritizing R&D for advanced formulations that address varying climatic and environmental demands. They are expanding their regional distribution networks and engaging in strategic partnerships with road construction firms and public infrastructure agencies. Sustainability is a core focus-firms are increasing investment in eco-friendly, low-VOC emulsifiers and promoting solutions that meet green construction mandates.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.2.5 Manufacturing process

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising infrastructure development

- 3.2.1.2 Environmental benefits & regulations

- 3.2.1.3 Cost-effectiveness

- 3.2.1.4 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited temperature range for application

- 3.2.2.2 Storage stability concerns

- 3.2.2.3 Lower strength compared to hot mix asphalt

- 3.2.2.4 Fluctuating crude oil prices

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand in emerging economies

- 3.2.3.2 Increasing focus on sustainable construction

- 3.2.3.3 Development of bio-based emulsifiers

- 3.2.3.4 Rising adoption in cold recycling technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cationic bitumen emulsifiers

- 5.2.1 Rapid setting (CRS)

- 5.2.2 Medium setting (CMS)

- 5.2.3 Slow setting (CSS)

- 5.3 Anionic bitumen emulsifiers

- 5.3.1 Rapid setting (RS)

- 5.3.2 Medium setting (MS)

- 5.3.3 Slow setting (SS)

- 5.4 Non-ionic bitumen emulsifiers

- 5.5 Modified bitumen emulsifiers

- 5.5.1 Polymer modified

- 5.5.1.1 SBS modified

- 5.5.1.2 SBR modified

- 5.5.1.3 Others

- 5.5.2 Latex modified

- 5.5.3 Others

- 5.5.1 Polymer modified

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Road construction & maintenance

- 6.2.1 Surface dressing

- 6.2.2 Tack coat

- 6.2.3 Prime coat

- 6.2.4 Slurry seal

- 6.2.5 Micro surfacing

- 6.2.6 Cold mix asphalt

- 6.2.7 Fog seal

- 6.2.8 Chip seal

- 6.3 Waterproofing

- 6.3.1 Building construction

- 6.3.2 Infrastructure

- 6.4 Pavement recycling

- 6.4.1 Full depth reclamation (FDR)

- 6.4.2 Cold in-place recycling (CIR)

- 6.4.3 Cold central plant recycling (CCPR)

- 6.5 Others

- 6.5.1 Soil stabilization

- 6.5.2 Adhesives

- 6.5.3 Industrial applications

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Road & highway construction

- 7.3 Airport construction

- 7.4 Building construction

- 7.4.1 Residential

- 7.4.2 Commercial

- 7.4.3 Industrial

- 7.5 Others

- 7.5.1 Railways

- 7.5.2 Marine

- 7.5.3 Agriculture

Chapter 8 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Batch process

- 8.3 Continuous process

- 8.4 Semi-continuous process

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alternative Environmental Technologies (AET)

- 10.2 Arkema Group

- 10.3 BASF SE

- 10.4 Bharat Petroleum Corporation Limited (BPCL)

- 10.5 BTBA

- 10.6 Dow Chemical Company

- 10.7 Evonik Industries AG

- 10.8 GlobeCore

- 10.9 Hindustan Colas Limited (HINCOL)

- 10.10 Hindustan Petroleum Corporation Limited (HPCL)

- 10.11 Ingevity Corporation

- 10.12 Jey Oil Refining Company

- 10.13 Kao Corporation

- 10.14 Marathon Petroleum Asphalt & Emulsions

- 10.15 Nouryon

- 10.16 Nynas AB

- 10.17 Petro Naft

- 10.18 Pro-Road Global

- 10.19 Royal Dutch Shell plc

- 10.20 Tiki Tar Industries

- 10.21 Total Energies SE

- 10.22 Winstrol Petrochemicals Pvt. Ltd.