|

市場調査レポート

商品コード

1766219

導電性ポリマーの市場機会と促進要因、業界動向分析、2025年~2034年予測Conductive Polymers (PEDOT, PANI) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 導電性ポリマーの市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年06月05日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

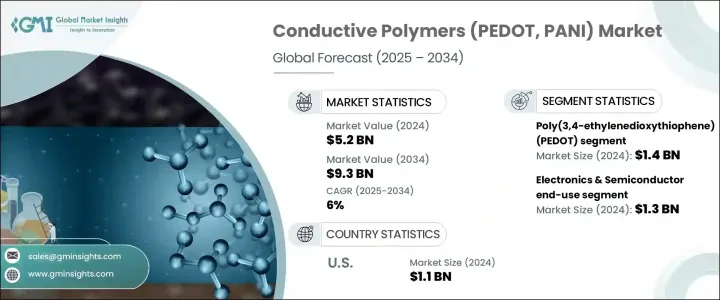

導電性ポリマー(PEDOT、PANI)の世界市場は、2024年には52億米ドルと評価され、CAGR 6%で成長し、2034年には93億米ドルに達すると予測されています。

市場の拡大は、インフラ開発、政府支出、広範な産業生産と密接に結びついており、これらはマクロ経済成長の触媒として作用し続けています。世界の製造業と都市化の着実な進展は、導電性材料の堅調な需要曲線に寄与しています。これらの動向は国際的な産業レポートと一致しており、世界の需要がデータと予測に影響される一方で、より広範な経済シフトによっても形成されることを示しています。加工技術の継続的な進歩は、生産コストを下げ、効率を高め、市場競争を促進しました。

同時に、環境施策規制は、サプライチェーン全体にわたって、よりクリーンな生産プラクティスとリサイクルを促しています。この移行は、サステイナブル成長のための新たな機会を生み出しています。新興市場における中産階級の台頭はさらに勢いを増し、エレクトロニクス、輸送、エネルギー貯蔵ソリューションなど、いずれも主要なエンドユーザー部門の需要を押し上げています。サプライチェーンの課題は世界的に根強いが、適応フレームワーク、自動化、技術革新により、市場は予測期間を通じて安定的に成長します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 52億米ドル |

| 予測金額 | 93億米ドル |

| CAGR | 6% |

ポリアニリン(PANI)セグメントは、その適応性の高い導電性と様々な環境条件下での回復力により、2024年に注目すべき収益を上げました。このポリマーは、産業と運輸セクタの活動活発化により、腐食保護とセンサベースのアプリケーションからの需要が年間約10%増加しています。今後も需要の加速に伴い、市場はこの増加傾向を維持すると予想されます。他タイプのポリマーは、複雑な加工上の課題や限られた拡大性による制約に依然として直面しています。これは、大規模使用における互換性、統合性、構造安定性を向上させる技術革新の必要性を示唆しています。

2024年には、本質的導電性ポリマー(ICP)セグメントは23億米ドルとなり、2034年までCAGR 6.1%で成長すると予想されています。導電性高分子複合材料、特に高分子-金属と高分子-炭素の組み合わせの使用増加が、その強化された機械的性能と導電性により需要を牽引しています。炭素系複合材料の年間需要は、自動車産業とエネルギー貯蔵産業での採用が主要原動力となり、20%成長したと報告されています。これらの複合材料は、ポリマーマトリクスと導電性フィラーの両方から強度を得ており、次世代用途向けの汎用性の高い材料を生み出しています。

ドイツの導電性ポリマー(PEDOT、PANI)市場は、最先端の製造方法とともにサステイナブルポリマー複合材料の統合に重点を置いているため、2024年には大きなシェアを占めます。よりエコフレンドリー生産への推進は、厳しい環境施策に沿ったものです。同地域への導電性ポリマーの輸入は年間12%増加しているが、これは主に自動車・航空宇宙メーカーの需要増に対応するためです。このことは、EUの持続可能性に関する指令に従って、現地の産業がいかに先進的でエコフレンドリー材料へとシフトしているかを浮き彫りにしています。

世界の導電性ポリマー(PEDOT、PANI)市場を独占している主要企業には、Heraeus HoldingとSigma-Aldrich(親会社グループであるMerck傘下で事業展開)があり、両社は強力な製品ポートフォリオと確立された市場影響力を持ち、継続的な産業拡大に大きく貢献しています。導電性ポリマー市場で事業を展開する企業は、市場での存在感を高めるため、技術革新、垂直統合、地域拡大を組み合わせた取り組みに注力しています。大手企業は、ポリマーの加工方法を進歩させ、電気特性を向上させ、進化する工業規格に適合する複合材料を開発するため、研究開発に投資しています。特にエレクトロニクス、自動車、エネルギー貯蔵などの最終用途産業との提携により、各社は用途に特化した材料を共同開発しています。企業はまた、サプライチェーンの脆弱性を軽減するために、世界の流通チャネルを強化し、原料へのアクセスを確保しています。リサイクル可能なポリマーを開発し、グリーン製造技術を導入している企業もあります。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主要動向

- 一次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:タイプ別、2021~2034年

- ポリ(3,4-エチレンジオキシチオフェン)(PEDOT)

- ポリアニリン(PANI)

- ポリピロール(PPy)

- ポリチオフェン(PTh)

- その他の導電性ポリマー

第6章 市場推定・予測:導電性メカニズム別、2021~2034年

- 主要動向

- 本質的導電性ポリマー(ICP)

- 導電性ポリマー複合材料(CPC)

- ポリマーカーボン複合材料

- ポリマー金属複合材料

- その他の複合材料

- 有機混合イオン電子伝導体(OMIEC)

第7章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 帯電防止包装

- コンデンサ

- 電池

- センサ

- 有機発光ダイオード(OLED)

- 太陽電池

- アクチュエータ

- エレクトロクロミックデバイス

- 電磁干渉(EMI)シールド

- プリント回路基板(PCB)

- スーパーコンデンサ

- その他

第8章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- エレクトロニクスと半導体

- エネルギー

- ヘルスケアとバイオメディカル

- 自動車

- 航空宇宙と防衛

- 繊維・ウェアラブル

- 産業

- 包装

- その他

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第10章 企業プロファイル

- Agfa-Gevaert N.V.

- Celanese Corporation

- Merck KGaA

- Solvay S.A.

- 3M Company

- SABIC

- Covestro AG

- Henkel AG & Co. KGaA

- Heraeus Holding GmbH

- PolyOne Corporation(Avient Corporation)

- Rieke Metals, LLC

- RTP Company

- Lubrizol Corporation

- Asbury Carbons

- Sigma-Aldrich Corporation(Merck Group)

- Panipol Oy

- Polyone Corporation

- Premix Group

- Hyperion Catalysis International

- Ormecon GmbH

The Global Conductive Polymers (PEDOT, PANI) Market was valued at USD 5.2 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 9.3 billion by 2034. Market expansion is closely tied to infrastructure development, government spending, and broader industrial output, which continue to act as macroeconomic growth catalysts. The steady rise in global manufacturing and urbanization contributes to a robust demand curve for conductive materials. These trends align with international industry reports and illustrate how global demand, while influenced by data and projections, is also shaped by broader economic shifts. The continued progress in processing technologies has lowered production costs and boosted efficiency, driving market competitiveness.

At the same time, environmental policy regulations have prompted cleaner production practices and recycling across supply chains. This transition is creating new opportunities for sustainable growth. The rising middle class in emerging markets adds further momentum, boosting demand for electronics, transportation, and energy storage solutions-all key end-user sectors. While supply chain challenges persist globally, adaptive frameworks, automation, and technical innovation are enabling the market to grow steadily throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 billion |

| Forecast Value | $9.3 billion |

| CAGR | 6% |

The polyaniline (PANI) segment generated notable revenues in 2024 due to its adaptable conductivity and resilience under varying environmental conditions. The polymer has seen approximately 10% annual growth in demand from corrosion protection and sensor-based applications, driven by increased activity across industrial and transportation sectors. Looking ahead, the market is expected to maintain this upward trend as demand accelerates. Other polymer types still face constraints due to complex processing challenges and limited scalability. This points to a need for innovation to improve compatibility, integration, and structural stability in large-scale use.

In 2024, the inherently conductive polymers (ICPs) segment stood at USD 2.3 billion and is anticipated to grow at a 6.1% CAGR through 2034. The rising use of conductive polymer composites-especially Polymer-Metal and Polymer-Carbon combinations-is driving demand due to their enhanced mechanical performance and conductivity. Annual demand for carbon-based composites has reportedly grown by 20%, largely fueled by adoption in the automotive and energy storage industries. These composites gain strength from both their polymer matrices and conductive fillers, creating highly versatile materials for next-gen applications.

Germany Conductive Polymers (PEDOT, PANI) Market held a sizeable share in 2024, due to its strong focus on integrating sustainable polymer composites alongside cutting-edge manufacturing practices. The push toward greener production is aligned with strict environmental policies. Imports of conductive polymers into the region have seen a 12% annual increase, largely to meet the rising demand from automotive and aerospace manufacturers. This highlights how local industries are shifting toward advanced, eco-friendly materials in compliance with EU sustainability mandates.

Key players dominating the Global Conductive Polymers (PEDOT, PANI) Market include Heraeus Holding and Sigma-Aldrich (operating under its parent group, Merck), both of which possess strong product portfolios and established market influence that contribute significantly to ongoing industry expansion. Companies operating in the conductive polymers market are focusing on a mix of innovation, vertical integration, and regional expansion to reinforce their market presence. Leading firms are investing in R&D to advance polymer processing methods, enhance electrical properties, and develop composites that meet evolving industrial standards. Partnerships with end-use industries-especially in electronics, automotive, and energy storage-allow companies to co-develop application-specific materials. Firms are also strengthening their global distribution channels and securing raw material access to reduce supply chain vulnerabilities. Sustainability is another major strategic pillar, with several companies developing recyclable polymers and implementing green manufacturing techniques.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Conduction mechanism

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Poly(3,4-ethylenedioxythiophene) (PEDOT)

- 5.2 Polyaniline (PANI)

- 5.3 Polypyrrole (PPy)

- 5.4 Polythiophene (PTh)

- 5.5 Other conductive polymers

Chapter 6 Market Estimates & Forecast, By Conduction Mechanism, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Inherently conductive polymers (ICPs)

- 6.3 Conductive polymer composites (CPCs)

- 6.3.1 Polymer-carbon composites

- 6.3.2 Polymer-metal composites

- 6.3.3 Other composites

- 6.4 Organic mixed ionic-electronic conductors (OMIECs)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Anti-static packaging

- 7.3 Capacitors

- 7.4 Batteries

- 7.5 Sensors

- 7.6 Organic light-emitting diodes (OLEDs)

- 7.7 Solar cells

- 7.8 Actuators

- 7.9 Electrochromic devices

- 7.10 Electromagnetic interference (EMI) shielding

- 7.11 Printed circuit boards (PCBs)

- 7.12 Supercapacitors

- 7.13 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Electronics & semiconductor

- 8.3 Energy

- 8.4 Healthcare & biomedical

- 8.5 Automotive

- 8.6 Aerospace & defense

- 8.7 Textiles & wearables

- 8.8 Industrial

- 8.9 Packaging

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Agfa-Gevaert N.V.

- 10.2 Celanese Corporation

- 10.3 Merck KGaA

- 10.4 Solvay S.A.

- 10.5 3M Company

- 10.6 SABIC

- 10.7 Covestro AG

- 10.8 Henkel AG & Co. KGaA

- 10.9 Heraeus Holding GmbH

- 10.10 PolyOne Corporation (Avient Corporation)

- 10.11 Rieke Metals, LLC

- 10.12 RTP Company

- 10.13 Lubrizol Corporation

- 10.14 Asbury Carbons

- 10.15 Sigma-Aldrich Corporation (Merck Group)

- 10.16 Panipol Oy

- 10.17 Polyone Corporation

- 10.18 Premix Group

- 10.19 Hyperion Catalysis International

- 10.20 Ormecon GmbH