半導体組立とテストのアウトソーシング市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Outsourced Semiconductor Assembly and Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766200

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

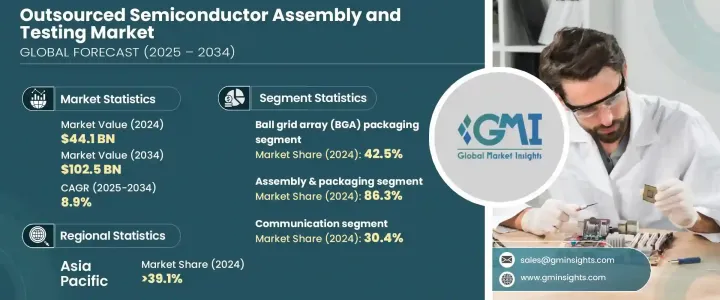

半導体組立とテストのアウトソーシングの世界市場規模は、2024年に441億米ドルとなり、CAGR 8.9%で成長し、2034年には1,025億米ドルに達すると推定されます。

この成長の主な要因は、スマートフォン、ウェアラブル端末、スマートホームデバイスを含むコンシューマーエレクトロニクス分野の拡大と、コスト効率に優れた特殊なパッケージングとテストソリューションに対する需要の高まりです。エレクトロニクス産業がデバイスの小型化と性能向上を続ける中、製品の信頼性と効率を確保するOSATサービスのニーズが高まっています。

最近の半導体パッケージングとテストの複雑化に伴い、内製に伴う高コストを管理するため、これらの業務をアウトソーシングする企業が増えています。この動向は、OSATインフラへの大規模な投資につながっており、特にこのようなサービスに対する需要が複数の業界で増加し続けています。コストの最適化が重視されるようになったことで、業界の主要企業を含む多くの半導体企業が、組立・検査サービスのアウトソーシングに依存するようになりました。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 441億米ドル |

| 予測金額 | 1,025億米ドル |

| CAGR | 8.9% |

半導体メーカーは、このような重要な機能をアウトソーシングすることで、社内運営に伴う多額の資本支出を回避することができます。こうした費用には、施設の建設や拡張、高価な機器の購入、大規模な専門作業員チームの雇用などが含まれることが多いです。アウトソーシングにより、企業はリソースを中核となる研究開発、製品開発、その他の優先度の高い分野に振り向けることができる一方、社内の組立ライン管理に伴う複雑さやオーバーヘッドを削減することができます。

組立・パッケージング分野の2024年の市場規模は382億米ドルで、CAGR 9.1%の堅調な成長率が予測されています。このセグメントは、特に人工知能(AI)、高性能コンピューティング、その他の革新的な半導体技術の進歩によって推進され、特殊なパッケージングとテストサービスを必要とします。半導体デバイスがますます複雑化・小型化するにつれて、高度に洗練された組立・パッケージング・ソリューションに対するニーズは高まり続けています。3Dパッケージング、システムインパッケージ(SiP)、マルチチップモジュール(MCM)などの先進パッケージング技術の統合は、最先端デバイスの信頼性と性能を確保する上で不可欠となっており、この分野の成長を牽引しています。

民生用電子機器分野の2024年の市場規模は113億米ドルで、CAGRは10.2%と推定されます。この成長の原動力となっているのは、より小型で効率的、かつ高機能な電子機器に対する需要の高まりです。携帯電話、タブレット、ウェアラブル、その他のポータブルガジェットの絶え間ない進化に伴い、メーカーは小型化と性能の厳しい要求を満たすために半導体組立とテストのアウトソーシングサービスに大きく依存しています。これらのデバイスが小型化、高機能化するにつれ、高性能、熱管理、信頼性向上を保証する先進パッケージングソリューションが必要とされています。

米国半導体組立とテストのアウトソーシング市場は2024年に107億米ドルを生み出し、CAGRは9.2%です。米国政府は、世界サプライチェーンへの依存を減らし、国内生産を促進することを目的としたCHIPS法のようなイニシアチブを通じて、国内半導体生産を強化する努力をしています。主要企業はパッケージングとテスト能力を強化するために多額の投資を受けており、米国はOSAT市場の主要プレーヤーとしての地位を強化しています。

半導体組立とテストのアウトソーシング市場の主要企業には、ASE Technology Holding Co.Ltd.、Amkor Technology Inc.、ChipMOS Technologies Inc.、Powertech Technology Inc.、King Yuan Electronics Co.Ltd.などです。半導体組立とテストのアウトソーシング市場におけるプレゼンスを強化するため、各社は最先端技術と高度なインフラに多額の投資を行っています。多くのOSATプロバイダーは、洗練された半導体製品に対する需要の高まりに対応するため、ハイエンド・パッケージング・ソリューションの能力を高めることに注力しています。半導体企業との戦略的提携や協力関係も、サービス提供の拡大や業務効率の向上に極めて重要です。さらに、企業は生産プロセスの合理化、コストの最小化、品質管理の強化のために自動化を導入しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 5Gインフラの拡張

- 自動車エレクトロニクスの進歩

- 家電製品の普及

- コスト効率の高い製造ソリューションの需要

- 小型化と先進パッケージング技術

- 落とし穴と課題

- 厳格な品質と信頼性の基準

- 高い資本投資要件

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:サービス種別、2021 –2034

- 主要動向

- 組み立てと梱包

- テスト

第6章 市場推計・予測:包装形態別、2021 –2034

- 主要動向

- ボールグリッドアレイ(BGA)パッケージ

- チップスケールパッケージ(CSP)

- スタックダイパッケージング

- マルチチップパッケージング

- クワッドフラットとデュアルインラインパッケージ

第7章 市場推計・予測:用途別、2021 –2034

- 主要動向

- コミュニケーション

- 家電

- 自動車

- コンピューティングとネットワーク

- 産業

- その他

- サービス

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- ASE Technology Holding Co. Ltd

- Amkor Technology Inc.

- Powertech Technology Inc.

- ChipMOS Technologies Inc.

- King Yuan Electronics Co. Ltd

- Formosa Advanced Technologies Co. Ltd

- Jiangsu Changjiang Electronics Technology Co. Ltd

- UTAC Holdings Ltd

- Lingsen Precision Industries Ltd

- Tongfu Microelectronics Co.

- Chipbond Technology Corporation

- Hana Micron Inc.

- Integrated Micro-electronics Inc.

- Tianshui Huatian Technology Co. Ltd

目次

The Global Outsourced Semiconductor Assembly and Testing Market was valued at USD 44.1 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 102.5 billion by 2034. This growth is primarily driven by the expansion of the consumer electronics sector, which includes smartphones, wearables, and smart home devices, as well as the increasing demand for cost-effective and specialized packaging and testing solutions. As the electronics industry continues to miniaturize devices and enhance performance, there is a growing need for OSAT services to ensure product reliability and efficiency.

With the complexity of modern semiconductor packaging and testing, more companies are outsourcing these operations to manage the high costs associated with in-house production. This trend has led to significant investments in OSAT infrastructure, especially as the demand for these services continues to rise across multiple industries. The growing focus on cost optimization has led many semiconductor companies, including major industry leaders, to rely on outsourcing assembly and testing services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $44.1 Billion |

| Forecast Value | $102.5 Billion |

| CAGR | 8.9% |

By outsourcing these essential functions, semiconductor manufacturers can avoid significant capital expenses associated with in-house operations. These expenses often include building or expanding facilities, purchasing expensive equipment, and employing large teams of specialized workers. Outsourcing allows companies to redirect resources toward core R&D, product development, and other high-priority areas while reducing the complexity and overhead involved in managing in-house assembly lines.

The assembly and packaging segment was valued at USD 38.2 billion in 2024, with projections indicating a robust growth rate of 9.1% CAGR. This segment is particularly driven by advancements in artificial intelligence (AI), high-performance computing, and other innovative semiconductor technologies that demand specialized packaging and testing services. As semiconductor devices become increasingly complex and miniaturized, the need for highly sophisticated assembly and packaging solutions continues to rise. The integration of advanced packaging techniques, such as 3D packaging, system-in-package (SiP), and multi-chip modules (MCM), has become critical to ensuring the reliability and performance of cutting-edge devices, thereby driving growth in this sector.

The consumer electronics segment was valued at USD 11.3 billion in 2024 and is estimated to grow at a CAGR of 10.2%. This growth is fueled by the increasing demand for smaller, more efficient, and highly functional electronic devices. With the continuous evolution of mobile phones, tablets, wearables, and other portable gadgets, manufacturers are relying heavily on outsourced semiconductor assembly and testing services to meet the rigorous demands of miniaturization and performance. As these devices become more compact and sophisticated, they require advanced packaging solutions that ensure high performance, thermal management, and enhanced reliability.

U.S Outsourced Semiconductor Assembly and Testing Market generated USD 10.7 billion in 2024 with a CAGR of 9.2%. The U.S. government is making efforts to bolster domestic semiconductor production through initiatives like the CHIPS Act, aimed at reducing reliance on global supply chains and boosting local manufacturing. Major companies are receiving significant investments to enhance their packaging and testing capabilities, reinforcing the U.S. as a key player in the OSAT market.

Prominent companies in the Outsourced Semiconductor Assembly and Testing Market include ASE Technology Holding Co. Ltd, Amkor Technology Inc., ChipMOS Technologies Inc., Powertech Technology Inc., and King Yuan Electronics Co. Ltd. To strengthen their presence in the outsourced semiconductor assembly and testing market, companies are investing heavily in state-of-the-art technologies and advanced infrastructure. Many OSAT providers are focusing on increasing their capabilities in high-end packaging solutions to cater to the growing demand for sophisticated semiconductor products. Strategic partnerships and collaborations with semiconductor companies are also pivotal for expanding service offerings and improving operational efficiency. Additionally, companies are embracing automation to streamline production processes, minimize costs, and enhance quality control.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and Definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.1.3.1 Supply-side impact

- 3.2.1.3.1.1 Price volatility

- 3.2.1.3.1.2 Supply chain restructuring

- 3.2.1.3.1.3 Production cost implications

- 3.2.1.3.2 Demand-side impact

- 3.2.1.3.2.1 Price transmission to end markets

- 3.2.1.3.2.2 Market share dynamics

- 3.2.1.3.2.3 Consumer response patterns

- 3.2.1.3.1 Supply-side impact

- 3.2.1.4 Key companies impacted

- 3.2.1.5 Strategic industry responses

- 3.2.1.5.1 Supply chain reconfiguration

- 3.2.1.5.2 Pricing and product strategies

- 3.2.1.5.3 Policy engagement

- 3.2.1.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Expansion of 5G infrastructure

- 3.3.1.2 Advancements in automotive electronics

- 3.3.1.3 Proliferation of consumer electronics

- 3.3.1.4 Demand for cost-effective manufacturing solutions

- 3.3.1.5 Miniaturization and advanced packaging technologies

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 Stringent quality and reliability standards

- 3.3.2.2 High capital investment requirements

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 Pestel analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market estimates and forecast, by Service Type, 2021 – 2034 (USD million)

- 5.1 Key trends

- 5.2 Assembly & Packaging

- 5.3 Testing

Chapter 6 Market estimates and forecast, by Packaging Type, 2021 – 2034 (USD million)

- 6.1 Key trends

- 6.2 Ball grid array (BGA) packaging

- 6.3 Chip scale packaging (CSP)

- 6.4 Stacked die packaging

- 6.5 Multi chip packaging

- 6.6 Quad Flat and Dual-inline Packaging

Chapter 7 Market estimates and forecast, by Application, 2021 – 2034 (USD million)

- 7.1 Key trends

- 7.2 Communication

- 7.3 Consumer electronics

- 7.4 Automotive

- 7.5 Computing and networking

- 7.6 Industrial

- 7.7 Others

- 7.8 Services

Chapter 8 Market estimates and forecast, by Region, 2021 – 2034 (USD million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company profiles

- 9.1 ASE Technology Holding Co. Ltd

- 9.2 Amkor Technology Inc.

- 9.3 Powertech Technology Inc.

- 9.4 ChipMOS Technologies Inc.

- 9.5 King Yuan Electronics Co. Ltd

- 9.6 Formosa Advanced Technologies Co. Ltd

- 9.7 Jiangsu Changjiang Electronics Technology Co. Ltd

- 9.8 UTAC Holdings Ltd

- 9.9 Lingsen Precision Industries Ltd

- 9.10 Tongfu Microelectronics Co.

- 9.11 Chipbond Technology Corporation

- 9.12 Hana Micron Inc.

- 9.13 Integrated Micro-electronics Inc.

- 9.14 Tianshui Huatian Technology Co. Ltd

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日