オルニチントランスカルバミラーゼ欠損症治療の市場機会、成長促進要因、産業動向分析、予測、2025年~2034年

Ornithine Transcarbamylase Deficiency Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766173

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

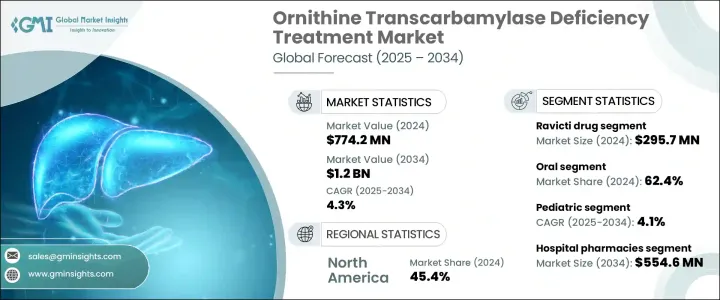

世界のオルニチントランスカルバミラーゼ欠損症治療市場は、2024年には7億7,420万米ドルとなり、2034年には12億米ドルに達し、CAGRで4.3%の成長が予測されています。

尿素サイクル障害(UCD)の罹患率の上昇、精密医療と遺伝子治療における継続的な技術革新が市場拡大の原動力となっています。医療専門家や患者の意識の高まりと、より高度な診断ツールが、より高い発見率と幅広い治療ニーズに寄与しています。特に女性における晩発症例の増加が患者層を拡大し、需要を促進しています。

遺伝子編集技術、酵素補充治療、肝臓を標的とした低分子化合物などの次世代治療法の開発は、研究と臨床試験への多額の投資によって支えられています。希少疾病用医薬品の指定、財政的優遇措置、迅速な承認プロセスなど、有利な規制の枠組みが市場をさらに前進させています。医療業界のこの分野は、尿素サイクルが障害されることで血中のアンモニア濃度が上昇し、継続的な管理を必要とする生命を脅かすことが多い稀な遺伝性疾患に対処する治療薬に焦点を当てています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億7,420万米ドル |

| 予測金額 | 12億米ドル |

| CAGR | 4.3% |

Ravictiセグメントは、2024年に2億9,570万米ドルを創出しました。このセグメントは、特に小児や高齢者にとって使いやすく、忍容性が向上しているため、患者から高い支持を得ています。その使いやすい製剤は、慢性的で生涯続く病態を管理する上で極めて重要な要素である治療のアドヒアランスを高める。同療法は複数の地域で規制当局の承認を得ており、さまざまな医療システムでの利用しやすさと取り込みが進んでいます。小児への適応が承認されたことで、対象となる人口が著しく拡大し、同分野の全体的な優位性に寄与しています。

経口投与セグメントは2024年に62.4%のシェアを占めました。経口投与が好まれるのは、その利便性と、継続的なケアが必要な病態の管理に不可欠な頻繁な通院への依存を軽減する能力に起因します。徐放化技術など医薬製剤の進歩により、経口薬の治療効果は向上し、静脈内投与に匹敵するものとなっています。この進歩は、患者のコンプライアンスを高めるだけでなく、より個別化された投与戦略を可能にし、経口OTC治療の幅広い普及に貢献しています。

米国のオルニチントランスカルバミラーゼ欠損症治療市場は、2024年の市場規模が3億1,560万米ドルでした。同国の医療支出は高く、OTC欠乏症のような希少疾患を抱える患者の治療選択肢へのアクセスが拡大しています。製薬開発企業、研究開発機関、バイオテクノロジー企業の協力により、この分野のイノベーションが加速しています。さらに、希少疾病用医薬品法(Orphan Drug Act)のような支援イニシアティブが、希少疾病を対象とする治療法の開発と迅速な承認を後押ししています。政府による資金援助やインセンティブプログラムは、研究と救命治療の普及に引き続き重要な役割を果たしています。

世界のオルニチントランスカルバミラーゼ欠損症治療市場を形成する主要企業には、Ultragenyx Pharmaceutical社、Abbott Laboratories社、Bausch Health Companies社、Arcturus Therapeutics社、Nutricia社(Danoneグループ)、Mead Johnson社(Reckitt Benckiser社)、Acer Therapeutics社、OrphanPacific社、Nestle社、Amgen社などがあります。市場ポジションを強化するため、オルニチントランスカルバミラーゼ欠損症治療市場の企業はいくつかの戦略的イニシアティブに注力しています。これには、革新的な遺伝子治療薬や酵素補充薬の臨床開発の加速、グローバルアクセスを拡大するためのパートナーシップやライセンシング契約への投資、希少疾病用医薬品の指定による規制上の優位性の確保などが含まれます。また多くの企業は、治療のアドヒアランスを高めるために患者支援プログラムを強化し、安定したサプライチェーンを確保するために製造能力を構築しています。さらに、新興市場をターゲットとして地理的なフットプリントを拡大し、診断と早期介入戦略を改善するために地域の保健機関と連携しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- OTC欠乏症の早期発見への意識向上

- 生命を脅かす疾患に対する満たされていない医療ニーズが高め

- 公的および民間保険会社による強力な保険と償還

- 業界の潜在的リスク&課題

- 承認された治療法の入手が限られている

- 治療費が高め

- 業界の潜在的リスク&課題

- 新生児スクリーニングの拡大による診断率の向上

- 専門薬局と希少疾患インフラの利用可能性の拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 将来の市場動向

- パイプライン分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な開発

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

第5章 市場推定・予測:製品別、2021年~2034年

- 主要動向

- Buphenyl

- Ravicti

- Ammonul

- 栄養補助食品

- その他の製品

第6章 市場推定・予測:投与経路別、2021年~2034年

- 主要動向

- 経口

- 静脈内

第7章 市場推定・予測:年齢層別、2021年~2034年

- 主要動向

- 小児

- 成人

第8章 市場推定・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第9章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott Laboratories

- Acer Therapeutics

- Amgen

- Arcturus Therapeutics

- Bausch Health Companies

- Nutricia(Danone Group)

- Mead Johnson(Reckitt Benckiser)

- Nestle

- OrphanPacific

- Ultragenyx Pharmaceutical

目次

The Global Ornithine Transcarbamylase Deficiency Treatment Market was valued at USD 774.2 million in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 1.2 billion by 2034. Market expansion is being driven by the rising incidence of urea cycle disorders (UCDs) and continued innovation in precision medicine and gene therapies. Increased awareness among healthcare professionals and patients, along with more advanced diagnostic tools, are contributing to higher detection rates and broader treatment needs. A growing number of late-onset cases, particularly in females, is expanding the patient base and fueling demand.

The development of next-generation therapies, including gene editing technologies, enzyme replacement treatments, and liver-targeted small molecules, is being supported by significant investments in research and clinical trials. A favorable regulatory framework, including orphan drug designations, financial incentives, and accelerated approval processes, is further propelling the market forward. This segment of the healthcare industry focuses on therapies that address a rare genetic disorder where the urea cycle is impaired, leading to elevated ammonia levels in the bloodstream, an often life-threatening condition requiring ongoing management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $774.2 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 4.3% |

The Ravicti segment generated USD 295.7 million in 2024. This segment benefits from strong patient preference due to its ease of use and improved tolerability, especially for children and the elderly. Its user-friendly formulation enhances treatment adherence, a crucial factor in managing chronic, lifelong conditions. The therapy has gained regulatory approval across several regions, increasing its accessibility and uptake across various healthcare systems. Its approval for pediatric use has notably expanded the eligible population, contributing to the segment's overall dominance.

The oral treatments segment held a 62.4% share in 2024. The preference for oral administration stems from its convenience and ability to reduce dependency on frequent hospital visits, which is essential for managing a condition that requires continuous care. Advancements in pharmaceutical formulations, such as extended-release technologies, have improved the therapeutic effectiveness of oral medications, making them comparable to intravenous options. This progress not only enhances patient compliance but also allows for more personalized dosing strategies, contributing to the broader adoption of oral OTC treatments.

United States Ornithine Transcarbamylase Deficiency Treatment Market was valued at USD 315.6 million in 2024. High healthcare spending in the country ensures greater access to treatment options for patients dealing with rare conditions like OTC deficiency. Collaborative efforts among pharmaceutical developers, research institutes, and biotechnology firms are accelerating innovation in this space. Additionally, supportive initiatives such as the Orphan Drug Act are encouraging the development and faster approval of therapies targeting rare diseases. Government funding and incentive programs continue to play a critical role in advancing research and the availability of life-saving treatments.

Key players shaping the Global Ornithine Transcarbamylase Deficiency Treatment Market include Ultragenyx Pharmaceutical, Abbott Laboratories, Bausch Health Companies, Arcturus Therapeutics, Nutricia (Danone Group), Mead Johnson (Reckitt Benckiser), Acer Therapeutics, OrphanPacific, Nestle, and Amgen. To strengthen their market positions, companies in the ornithine transcarbamylase deficiency treatment market are focusing on several strategic initiatives. These include accelerating clinical development of innovative gene therapies and enzyme replacement solutions, investing in partnerships and licensing deals to expand global access, and securing regulatory advantages through orphan drug designations. Many firms are also enhancing patient support programs to increase treatment adherence and building manufacturing capabilities to ensure steady supply chains. Additionally, they are broadening their geographic footprint by targeting emerging markets and aligning with regional health agencies to improve diagnosis and early intervention strategies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.1.1 Key market trends

- 2.1.2 Regional

- 2.1.3 Product

- 2.1.4 Route of administration

- 2.1.5 Age group

- 2.1.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased awareness for earlier detection of OTC deficiency

- 3.2.1.2 High unmet medical need for life-threatening condition

- 3.2.1.3 Strong insurance and reimbursement by public and private insurers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited availability of approved therapies

- 3.2.2.2 High cost of treatment

- 3.2.3 Industry pitfalls and challenges

- 3.2.3.1 Increasing diagnosis rates due to expanded newborn screening

- 3.2.3.2 Growing availability of specialty pharmacies and rare disease infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Pipeline analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key development

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New Product Launches

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Buphenyl

- 5.3 Ravicti

- 5.4 Ammonul

- 5.5 Dietary supplements

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Intravenous

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatrics

- 7.3 Adults

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Acer Therapeutics

- 10.3 Amgen

- 10.4 Arcturus Therapeutics

- 10.5 Bausch Health Companies

- 10.6 Nutricia (Danone Group)

- 10.7 Mead Johnson (Reckitt Benckiser)

- 10.8 Nestle

- 10.9 OrphanPacific

- 10.10 Ultragenyx Pharmaceutical

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日