|

市場調査レポート

商品コード

1755368

製造炭素管理システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Manufacturing Carbon Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 製造炭素管理システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月19日

発行: Global Market Insights Inc.

ページ情報: 英文 127 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

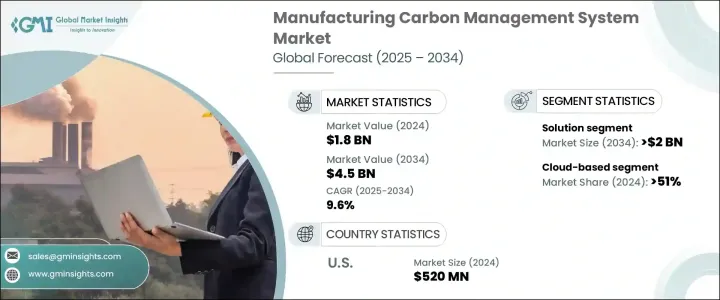

世界の製造炭素管理システム市場は、2024年には18億米ドルと評価され、2034年にはCAGR 9.6%で成長して45億米ドルに達すると推定されています。

世界各国の政府は、炭素排出を抑制するためにより厳しい法律を導入しており、気候変動目標を達成するため、カーボンプライシング、税金、キャップ・アンド・トレード制度、温室効果ガス(GHG)報告の義務化などの仕組みを取り入れています。これを受けて、企業は炭素管理ソリューションの採用を増やしており、メーカー各社は環境への影響を最小限に抑える技術の導入を進めています。

しかし、センサー、自動化ツール、エネルギー効率の高い機械などの輸入部品に対する貿易関税は、炭素管理システムのアップグレードのコストを引き上げる可能性があります。これは中堅メーカーのアクセスを制限するかもしれないが、輸入コスト上昇の影響を軽減しようと企業が努力する中で、国内の技術革新を促進し、現地調達の炭素管理ソリューションへの需要を高める可能性もあります。一方、AI、データ分析、IoT、ブロックチェーンなどの技術の進歩は、炭素管理ソリューションの効率を高め、企業が排出量を監視、管理、報告できるようにしています。こうした技術革新により、業界全体でこうしたシステムの導入が加速しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 18億米ドル |

| 予測金額 | 45億米ドル |

| CAGR | 9.6% |

炭素管理システム市場のソリューション分野は、規制上の要求の高まりと強固な環境報告の必要性によって、2034年までに20億米ドルに達すると予測されています。これらのソリューションは、リアルタイムの排出データを提供し、脱炭素化シナリオのモデリングを可能にし、GHGプロトコルやESG開示のような報告枠組みをサポートします。企業がより厳しい持続可能性規制を満たし、二酸化炭素排出量を削減しようと努力する中、こうした先進的なツールに対する需要は高まり続けています。

クラウドベースの炭素管理プラットフォーム・セグメントは、2024年までに51%のシェアを占めると思われます。企業がリアルタイムで炭素排出量を追跡・分析できる柔軟でスケーラブルなソリューションを提供できる点が、特に魅力的です。これらのプラットフォームは追跡をサポートするだけでなく、業界の持続可能性目標や環境基準にも適合しているため、透明性の向上、パフォーマンスの改善、進化する規制要件の遵守を目指す企業にとって重要なツールとなっています。

米国の製造炭素管理システム市場は2024年に5億2,000万米ドルを創出し、急速な技術革新、産業シフト、気候変動緩和重視の高まりがその原動力となっています。この市場は、環境・社会・ガバナンス(ESG)原則の採用の高まりと、カーボンフットプリントの開示に対する法的圧力の高まりによってさらに活性化しています。米国では、企業が持続可能性の目標や規制要件を満たすことへの圧力が高まっており、炭素管理ソリューションの市場は引き続き勢いを増しています。

世界の製造炭素管理システム業界の主要企業には、Accuvio、Carbon Footprint Ltd.、Dakota Software、Enablon、EnergyCap、Engie、Enviance、Envirosoft、ESP、IBM、Intelex、Isometrix、Locus Technologies、NativeEnergy、Salesforce、SAP、Schneider Electric、Trinity Consultantsなどがあります。世界の製造炭素管理システム業界の企業が市場での存在感を高めるために採用している主な戦略には、AI、ブロックチェーン、IoTなどの最先端技術の統合が含まれます。これは、企業がデータ追跡、排出量報告、持続可能性への取り組みを改善するのに役立ちます。政府機関や業界規制当局との戦略的パートナーシップも、拡大する環境政策への対応に不可欠です。スケーラブルなクラウドベースのソリューションを提供し、データ分析を活用することで、企業はリアルタイムの排出量モニタリングと透明性の高い報告に対する需要の高まりに応えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 供給側の影響(原材料)

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソリューション

- サービス

第6章 市場規模・予測:展開別、2021年~2034年

- 主要動向

- クラウド

- オンプレミス

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- Accuvio

- Carbon Footprint Ltd.

- Dakota Software

- Enablon

- EnergyCap.

- Engie

- Enviance

- Envirosoft

- ESP

- IBM

- Intelex

- Isometrix

- Locus Technlogies

- NativeEnergy

- Salesforce

- SAP

- Schneider Electric

- Trinity Consultants

The Global Manufacturing Carbon Management System Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 9.6% to reach USD 4.5 billion by 2034, attributed to the implementation of stringent environmental policies and rising regulations surrounding carbon management. Governments worldwide are introducing stricter laws to curb carbon emissions, incorporating mechanisms like carbon pricing, taxes, cap-and-trade systems, and mandatory greenhouse gas (GHG) reporting to meet climate change goals. In response, organizations are increasingly adopting carbon management solutions, driving manufacturers to embrace technologies that minimize their environmental impact.

However, trade tariffs on imported components, such as sensors, automation tools, and energy-efficient machinery, could potentially raise the cost of carbon management system upgrades. While this might restrict access for mid-sized manufacturers, it may also drive domestic innovation and increase demand for locally sourced carbon management solutions as companies strive to mitigate the impact of higher import costs. Meanwhile, advancements in technologies like AI, data analytics, IoT, and blockchain are enhancing the efficiency of carbon management solutions, allowing companies to monitor, manage, and report emissions. These innovations are accelerating the adoption of these systems across industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 9.6% |

The solution segment of the carbon management system market is anticipated to reach USD 2 billion by 2034, driven by increasing regulatory demands and the need for robust environmental reporting. These solutions offer real-time emissions data, enable decarbonization scenario modeling, and support reporting frameworks like the GHG Protocol and ESG disclosures, which are becoming essential for businesses to stay compliant and demonstrate environmental responsibility. As companies strive to meet stricter sustainability regulations and reduce their carbon footprint, the demand for these advanced tools continues to rise.

Cloud-based carbon management platforms segment will hold a 51% share by 2024. Their ability to offer flexible, scalable solutions that allow businesses to track and analyze carbon emissions in real time makes them particularly attractive. These platforms not only support tracking but also align with industry sustainability goals and environmental standards, making them critical tools for businesses aiming to enhance transparency, improve performance, and meet evolving regulatory requirements.

U.S. Manufacturing Carbon Management System Market generated USD 520 million in 2024, driven by rapid technological innovations, industry shifts, and the growing emphasis on climate change mitigation. This market is further fueled by the rising adoption of Environmental, Social, and Governance (ESG) principles and the increasing legal pressures to disclose carbon footprints. As companies in the U.S. face mounting pressure to meet sustainability objectives and regulatory requirements, the market for carbon management solutions continues to gain momentum.

Key players in the Global Manufacturing Carbon Management System Industry include Accuvio, Carbon Footprint Ltd., Dakota Software, Enablon, EnergyCap, Engie, Enviance, Envirosoft, ESP, IBM, Intelex, Isometrix, Locus Technologies, NativeEnergy, Salesforce, SAP, Schneider Electric, and Trinity Consultants. Key strategies adopted by companies in the Global Manufacturing Carbon Management System Industry to enhance their market presence include integrating cutting-edge technologies like AI, blockchain, and IoT. This helps companies improve their data tracking, emissions reporting, and sustainability efforts. Strategic partnerships with governmental bodies and industry regulators are also vital for compliance with growing environmental policies. By offering scalable cloud-based solutions and leveraging data analytics, firms are meeting the increasing demand for real-time emission monitoring and transparent reporting.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (Raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-side impact (Raw materials)

- 3.2.3 Demand-side impact (selling price)

- 3.2.3.1.1 Price transmission to end markets

- 3.2.3.1.2 Market share dynamics

- 3.2.3.1.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future Considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Component, 2021 - 2034, (USD Billion)

- 5.1 Key trends

- 5.2 Solution

- 5.3 Services

Chapter 6 Market Size and Forecast, By Deployment, 2021 - 2034, (USD Billion)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-premises

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034, (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 UK

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.5.3 UAE

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Accuvio

- 8.2 Carbon Footprint Ltd.

- 8.3 Dakota Software

- 8.4 Enablon

- 8.5 EnergyCap.

- 8.6 Engie

- 8.7 Enviance

- 8.8 Envirosoft

- 8.9 ESP

- 8.10 IBM

- 8.11 Intelex

- 8.12 Isometrix

- 8.13 Locus Technlogies

- 8.14 NativeEnergy

- 8.15 Salesforce

- 8.16 SAP

- 8.17 Schneider Electric

- 8.18 Trinity Consultants