|

市場調査レポート

商品コード

1755316

宇宙サイバーセキュリティの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Space Cybersecurity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 宇宙サイバーセキュリティの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月22日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

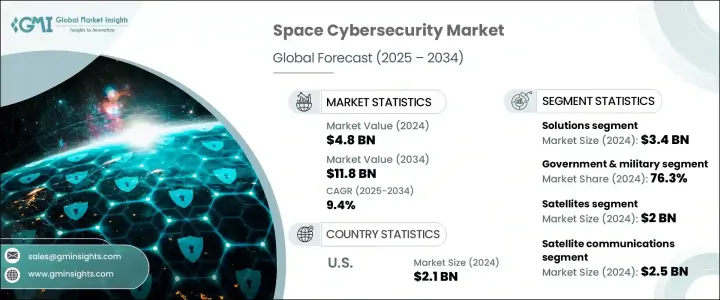

世界の宇宙サイバーセキュリティ市場は、2024年には48億米ドルと評価され、2034年には118億米ドルに達するまでCAGR 9.4%で成長すると予測されています。

これは、商業宇宙事業の継続的な増加に加えて、政府機関や防衛機関による宇宙に焦点を当てたサイバーセキュリティイニシアチブへの投資の増加によるものです。宇宙がますます戦略的な領域となるにつれ、軌道上のデジタルインフラの安全確保は国家的・世界の優先事項となっています。官民の事業体は、機密性の高い衛星ネットワーク、通信システム、ミッションクリティカルな宇宙資産を保護するため、サイバーセキュリティソリューションを展開しています。軌道技術が進化し、サイバー攻撃の脅威が軍事・商用プラットフォーム双方で強まるにつれ、宇宙事業におけるエンドツーエンドの保護に対する需要は高まり続けています。

戦略的防衛政策が宇宙システムの近代化を続ける中、軌道資産のサイバー保護が優先されています。衛星通信と宇宙監視への依存度が高まるにつれて、これらのシステムをサイバー脆弱性から保護する重要な必要性が生じています。この業界は、以前の関税政策により、暗号化システムや安全な通信ハードウェアのような必須コンポーネントの価格が上昇し、大きなコスト圧力に見舞われました。これらの関税は、主要な海外サプライヤーからの調達に影響を与え、米国に拠点を置く企業の運用コストを上昇させ、価格構造や納期に影響を与えました。同時に、グローバルサプライチェーンが不安定になったことで、衛星や基幹インフラ向けの主要なサイバーセキュリティソリューションの展開が長期化しました。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 48億米ドル |

| 予測金額 | 118億米ドル |

| CAGR | 9.4% |

2024年、衛星、ミッションコンピュータ、宇宙通信システムを新たなサイバー脅威から保護する高度なツールの需要が急増し、ソリューション分野の市場規模は34億米ドルとなり、強い勢いを見せています。暗号化ハードウェア、高度なサイバーセキュリティプラットフォーム、安全な通信プロトコルなどの技術は、現在、軌道上でのシームレスで安全な運用を確保するために不可欠です。商業衛星や防衛衛星の打ち上げが世界的に増加する中、堅牢で拡張性のある特殊なセキュリティソリューションに対するニーズは急速に拡大しています。

最終用途別に分類すると、政府・軍事分野が2024年に76.3%のシェアを占め、その優位性を浮き彫りにしています。同セグメントがリードしているのは、通信、監視、国家安全保障業務において、安全で暗号化された衛星ベースのシステムへの依存が高まっているためです。防衛インフラを狙ったサイバー攻撃により、国家機関はサイバーセキュリティに高い予算を割くようになりました。脅威の複雑化と地政学的不確実性の増大により、防衛組織は統合的かつ階層的なセキュリティアーキテクチャを採用することが不可欠となっています。

ドイツの宇宙サイバーセキュリティドイツ市場は、航空宇宙製造におけるリーダーシップと、宇宙インフラにおけるサイバー保護への継続的な重点を背景に、2034年までCAGR 9.6%で成長すると予想されます。衛星通信、地球観測、宇宙研究に対する国家機関の投資が引き続き需要を牽引しています。ドイツは、民間航空宇宙と防衛航空宇宙の両方の構想にサイバーセキュリティを統合することに重点を置いており、着実かつ持続的な市場成長を生み出しています。

競合情勢を形成している主な企業は、RTX Corporation、Thales Group、Lockheed Martin Corporation、Northrop Grummanなどです。これらの企業は、いくつかの重点戦略を通じて市場での存在感を高めています。これらの企業は、宇宙用途に合わせた次世代サイバーセキュリティシステムを開発するために研究開発に投資しています。また、防衛機関と戦略的提携を結んで長期契約を確保し、安定した収益を確保している企業も多いです。さらに、不安定なグローバルサプライチェーンへの依存を減らすため、企業は国内生産能力を強化しています。AIを活用したセキュリティプラットフォームと予測的脅威検知モデルを採用することで、宇宙ミッションのリアルタイム対応能力と長期的な回復力を向上させています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界の対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 影響要因

- 促進要因

- 政府と軍事投資

- 宇宙資産への脅威の高まり

- 商業宇宙活動の拡大

- 世界の宇宙探査の取り組み

- 宇宙交通の増加

- 業界の潜在的リスク&課題

- 導入コストが高め

- 熟練したサイバーセキュリティ専門家の不足

- 促進要因

- 成長可能性分析

- テクノロジーとイノベーションの情勢

- 主なニュースと取り組み

- 将来の市場動向

- ポーター分析

- PESTEL分析

- 規制情勢

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:提供別、2021年~2034年

- 主要動向

- ソリューション

- ネットワークセキュリティ

- エンドポイントとIoTセキュリティ

- アプリケーションセキュリティ

- クラウドセキュリティ

- データ保護

- アイデンティティとアクセス管理(IAM)

- その他

- サービス

- マネージドサービス

- 専門サービス

第6章 市場推計・予測:プラットフォーム別、2021年~2034年

- 主要動向

- 衛星

- 打ち上げロケット

- 地上局

- 宇宙港と打ち上げ施設

- 指揮統制センター

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 衛星通信

- 地球観測

- ナビゲーション

- 宇宙探査

- その他

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 政府と軍

- 商業用

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Airbus

- BAE Systems

- Boeing

- Booz Allen Hamilton Inc.

- CYSEC

- General Dynamics

- Kratos Defense &Security Solutions, Inc.

- L3Harris Technologies, Inc.

- Leidos

- Leonardo S.p.A.

- Lockheed Martin Corporation

- Microsoft

- Northrop Grumman

- OHB Digital Connect GmbH

- RTX Corporation

- SpiderOak Inc.

- Thales Group

- Xage Security

The Global Space Cybersecurity Market was valued at USD 4.8 billion in 2024 and is estimated to grow at a CAGR of 9.4% to reach USD 11.8 billion by 2034, fueled by increased investments in space-focused cybersecurity initiatives from government and defense bodies, alongside the ongoing rise in commercial space operations. As space becomes an increasingly strategic domain, securing digital infrastructure in orbit has become a national and global priority. Public and private entities deploy cybersecurity solutions to protect sensitive satellite networks, communications systems, and mission-critical space assets. The demand for end-to-end protection in space operations continues to grow as orbital technologies evolve and the threat of cyber-attacks intensifies across both military and commercial platforms.

As strategic defense policies continue to modernize space systems, cyber protection of orbital assets is prioritized. The rising dependency on satellite communication and space surveillance has created a critical need to shield these systems from cyber vulnerabilities. The industry experienced significant cost pressures due to earlier tariff policies, which drove up prices for essential components like encryption systems and secure communications hardware. These tariffs affected sourcing from major international suppliers and increased operational costs for US-based companies, impacting their pricing structures and delivery timelines. Simultaneously, global supply chain instability led to prolonged deployment delays of key cybersecurity solutions for satellite and mission-critical infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 Billion |

| Forecast Value | $11.8 Billion |

| CAGR | 9.4% |

In 2024, the solutions segment was valued at USD 3.4 billion witnessing strong momentum as demand surges for sophisticated tools that can secure satellites, mission computers, and space communications systems from emerging cyber threats. Technologies such as encryption hardware, advanced cybersecurity platforms, and secure communication protocols are now critical to ensuring seamless and safe operations in orbit. With commercial and defense satellite launches increasing globally, the need for robust, scalable, and specialized security solutions is rapidly expanding.

When segmented by end-use, the government and military segment accounted for a 76.3% share in 2024, highlighting its dominance. The segment's lead is attributed to growing reliance on secure, encrypted satellite-based systems for communication, surveillance, and national security operations. Cyberattacks targeting defense infrastructure have pushed state agencies to allocate higher budgets toward cybersecurity. The increasing complexity of threats and geopolitical uncertainty has made it essential for defense organizations to adopt integrated and layered security architectures.

Germany Space Cybersecurity Market is expected to grow at a CAGR of 9.6% through 2034, backed by its leadership in aerospace manufacturing and continued emphasis on cyber protection within space infrastructure. Investments from national agencies in satellite communications, earth observation, and space research continue to drive demand. Germany's focus on integrating cybersecurity across both commercial and defense aerospace initiatives is creating steady and sustained market growth.

Key players shaping the competitive landscape include RTX Corporation, Thales Group, Lockheed Martin Corporation, and Northrop Grumman. These companies are advancing their market presence through several focused strategies. They invest in R&D to create next-generation cybersecurity systems tailored for space applications. Many are forming strategic alliances with defense agencies to secure long-term contracts, ensuring consistent revenue flow. Additionally, companies are enhancing their domestic production capabilities to reduce reliance on volatile global supply chains. Adopting AI-powered security platforms and predictive threat detection models, improve real-time response capabilities and long-term resilience for space missions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 key companies impacted

- 3.2.4 strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Government and military investments

- 3.3.1.2 Rising threats to space assets

- 3.3.1.3 Expansion of commercial space activities

- 3.3.1.4 Global space exploration efforts

- 3.3.1.5 Increased space traffic

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High costs of implementation

- 3.3.2.2 Shortage of skilled cybersecurity professionals

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Technological & innovation landscape

- 3.6 Key news and initiatives

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Regulatory landscape

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Offerings, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Solutions

- 5.2.1 Network security

- 5.2.2 Endpoint and IoT security

- 5.2.3 Application security

- 5.2.4 Cloud security

- 5.2.5 Data protection

- 5.2.6 Identity and access management (IAM)

- 5.2.7 Others

- 5.3 Services

- 5.3.1 Managed services

- 5.3.2 Professional services

Chapter 6 Market Estimates & Forecast, By Platform, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Satellites

- 6.3 Launch vehicles

- 6.4 Ground stations

- 6.5 Spaceports & launch facilities

- 6.6 Command & control centers

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Satellite communications

- 7.3 Earth observation

- 7.4 Navigation

- 7.5 Space exploration

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 Government & military

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Airbus

- 10.2 BAE Systems

- 10.3 Boeing

- 10.4 Booz Allen Hamilton Inc.

- 10.5 CYSEC

- 10.6 General Dynamics

- 10.7 Kratos Defense & Security Solutions, Inc.

- 10.8 L3Harris Technologies, Inc.

- 10.9 Leidos

- 10.10 Leonardo S.p.A.

- 10.11 Lockheed Martin Corporation

- 10.12 Microsoft

- 10.13 Northrop Grumman

- 10.14 OHB Digital Connect GmbH

- 10.15 RTX Corporation

- 10.16 SpiderOak Inc.

- 10.17 Thales Group

- 10.18 Xage Security