|

市場調査レポート

商品コード

1755291

自動車用故障回路コントローラの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Automotive Fault Circuit Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用故障回路コントローラの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月28日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

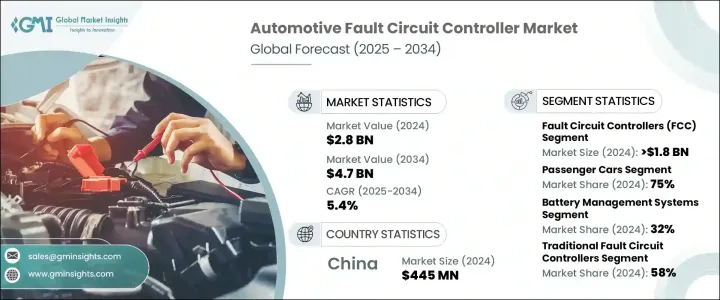

自動車用故障回路コントローラの世界市場規模は、2024年に28億米ドルとなり、CAGR 5.4%で成長し、2034年には47億米ドルに達すると予測されています。

この成長は、電気自動車(EV)やハイブリッドモデルへのシフトが進んでいることが大きな要因であり、電気自動車は複雑なパワーエレクトロニクスや高電圧バッテリーを搭載しているため、より高度な電気安全システムを必要としています。故障回路コントローラは、故障を迅速に特定して切り分け、重要な部品を損傷から保護するため、これらの自動車の安全な運転に不可欠です。

特に排ガス規制の強化や政府の奨励策によってEVの普及が進むにつれ、FCCに対する需要は高まっています。これらのデバイスは、自動車の安全性を確保し、ダウンタイムを最小限に抑え、電気システムの信頼性を維持するのに役立ちます。これは、自動車の性能、ナビゲーション、運転支援においてADAS(先進電子機器)への依存度が高まるにつれて極めて重要です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 28億米ドル |

| 予測金額 | 47億米ドル |

| CAGR | 5.4% |

コネクテッドカーや自律走行車(AV)の台頭は、自動車システムに新たな複雑性をもたらしています。これらの自動車は、高度なセンサー、通信ネットワーク、人工知能(AI)アルゴリズムに大きく依存し、リアルタイムの意思決定と環境ナビゲーションを行う。これらの技術が進化するにつれて、信頼性が高く安全な電気システムへの要求も高まっています。故障回路コントローラ(FCC)は、電気的な障害に直面しても、これらの複雑なシステムが確実に動作し続けるために極めて重要な役割を果たします。自律走行車では、パワートレインや通信システムに軽微な障害が発生しただけでも大惨事につながるため、こうした保護装置は車両の安全性と性能を維持するために不可欠です。

2024年、故障回路コントローラ(FCC)分野の売上高は18億米ドルに達しました。FCCは電気自動車のパワートレインにおいて特に重要であり、高電圧システムは故障が迅速に検出されないと重大な故障を引き起こす可能性があります。電気自動車は400Vから800Vの電圧範囲で作動するため、初期段階で故障を隔離して潜在的な災害を防止するFCCの役割は過大評価できないです。異常な電流の流れを検出し、故障した回路を切り離す能力は、これらの自動車の安全性を維持するために不可欠です。その結果、EVメーカーがこれらの安全装置を自動車に搭載する傾向が強まり、この市場セグメントは急成長しています。

バッテリー管理システム分野は2024年に32%のシェアを獲得し、2034年まで顕著な拡大が見込まれています。これらのシステム内のバッテリーモニタリングユニットは、電気自動車の安全性と信頼性を確保する上で極めて重要な役割を果たしています。これらのユニットは電圧、温度、電流などの主要パラメーターを追跡し、不良セルや回路の早期特定を可能にします。故障回路コントローラと組み合わせることで、これらのシステムは停電や熱問題の防止に役立ち、バッテリーの寿命と車両全体の性能を向上させます。安全スイッチとして機能するバッテリディスコネクトユニットは、故障時やメンテナンス時の車両電気系統の安全確保にさらに貢献します。

アジア太平洋自動車用故障回路コントローラ市場は2024年に43%のシェアを占め、4億4,500万米ドルを創出しました。中国が世界最大のEV市場であることは、FCC需要の重要な要因です。自動車の安全性に関する規制要件が厳しくなるにつれて、中国の自動車メーカーは、バッテリ管理システム、パワーエレクトロニクス、Eドライブユニットの過電流保護用に高度なFCCの採用を増やしています。自動車の安全性と信頼性の向上を目指す同国の動きは、FCCを電気ドライブトレインに不可欠なコンポーネントとし、市場の成長をさらに加速させています。

自動車用故障回路コントローラ世界市場の主要企業には、Siemens, Mitsubishi Electric, Honeywell International, Infineon Technologies, ABB, Panasonic Corporation, Eaton, Bosch Automotive Electronics, General Electric (GE), and Schneider Electric.などがいます。自動車用故障回路コントローラ市場での地位を強化するため、各社は自動車業界の進化する安全基準を満たす、最先端で信頼性が高く効率的なソリューションの開発に注力しています。各社は、高電圧の電気自動車やコネクテッドカーに最適な製品を提供するため、研究開発に多額の投資を行って故障保護技術を革新しています。さらに、これらの企業は自動車メーカーとの提携を拡大し、FCCを最新のパワートレインやバッテリー管理システムにシームレスに統合しています。また、さまざまな車種やタイプの特定のニーズに対応するカスタマイズ・ソリューションの提供も優先事項となっています。各社は、生産能力を拡大し、電気自動車の普及が進む新興市場での存在感を高めることで、市場での足場を固めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 車両の電動化と高電圧アーキテクチャの採用の急増

- 乗客の安全と規制遵守への重点が高まっている

- コネクテッドカーおよび自動運転車技術の拡大

- 先進運転支援システム(ADAS)への故障検出システムの統合

- 業界の潜在的リスク&課題

- 高い複雑さと統合コスト

- 過酷な自動車環境における信頼性の問題

- 市場機会

- 電気自動車(EV)製造の拡大

- ADAS(先進運転支援システム)(ADAS)との統合

- 電気安全遵守のための規制の推進

- 新興自動車市場の成長

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向s

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- 故障回路制御装置(FCC)

- 回路保護装置

- センサーと監視ユニット

- 制御モジュール

第6章 市場推計・予測:車種別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- SUV

- ハッチバック

- 商用車

- LCV(小型商用車)

- MCV(中型商用車)

- HCV(大型商用車)

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- エンジン管理システム

- バッテリー管理システム

- 照明システム

- インフォテインメントおよびコネクティビティシステム

- 安全システム

- HVAC(暖房、換気、空調)

第8章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 従来の故障回路制御装置

- スマート/インテリジェント故障回路コントローラ

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- OEM(オリジナル機器メーカー)

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- マレーシア

- シンガポール

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- ABB

- Alstom

- American Superconductor

- Autoliv

- Bosch Automotive Electronics

- Continental

- Denso

- Eaton

- General Electric(GE)

- Honeywell International

- Infineon Technologies

- Liaoning Rongxin Electric Power Electronic Co.

- Mitsubishi Electric

- Nexans

- Panasonic

- Schneider Electric

- Siemens

- Superconductor Technologies

- TE Connectivity

- Valeo

The Global Automotive Fault Circuit Controller Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 4.7 billion by 2034. This growth is largely driven by the increasing shift towards electric vehicles (EVs) and hybrid models, which require more sophisticated electrical safety systems due to their complex power electronics and high-voltage batteries. Fault circuit controllers are integral to the safe operation of these vehicles, as they identify and isolate faults quickly, protecting essential components from damage.

As the adoption of EVs continues to rise, especially with stricter emission regulations and government incentives, the demand for FCCs is growing. These devices help ensure vehicle safety, minimize downtime, and maintain the reliability of electrical systems, which is crucial as vehicles become increasingly dependent on advanced electronics for performance, navigation, and driver assistance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $4.7 Billion |

| CAGR | 5.4% |

The rise of connected and autonomous vehicles (AVs) introduces a new layer of complexity to automotive systems. These vehicles rely heavily on advanced sensors, communication networks, and artificial intelligence (AI) algorithms to make real-time decisions and navigate environments. As these technologies evolve, so does the demand for highly reliable and secure electrical systems. Fault circuit controllers (FCCs) play a pivotal role in ensuring that these intricate systems remain operational, even in the face of electrical disruptions. In autonomous vehicles, even a minor fault in the powertrain or communication system leads to catastrophic outcomes, making these protective devices critical for maintaining vehicle safety and performance.

In 2024, the fault circuit controller (FCC) segment generated USD 1.8 billion. FCCs are particularly critical in electric vehicle powertrains, where high-voltage systems can cause significant failures if faults are not detected quickly. With electric vehicles operating within voltage ranges of 400V to 800V, the role of FCCs in preventing potential disasters by isolating faults at the earliest stages cannot be overstated. Their ability to detect abnormal current flow and disconnect faulty circuits is essential for maintaining the safety of these vehicles. Consequently, this market segment has grown rapidly as EV manufacturers increasingly incorporate these safety devices into their automobiles.

The battery management systems segment captured a 32% share in 2024 and is expected to see notable expansion through 2034. Battery monitoring units within these systems play a pivotal role in ensuring the safety and reliability of electric vehicles. These units track key parameters like voltage, temperature, and current, allowing early identification of faulty cells or circuits. When paired with fault circuit controllers, these systems help prevent power failures and thermal issues, thus enhancing battery longevity and overall vehicle performance. Battery disconnects units, which act as safety switches, further contribute to ensuring the safety of the vehicle's electrical system during faults or maintenance.

Asia Pacific Automotive Fault Circuit Controller Market held a 43% share and generated USD 445 million in 2024. China's status as the largest EV market globally is a key factor in the demand for FCCs, as local manufacturers are rapidly expanding their electric vehicle offerings. As regulatory requirements for vehicle safety become stricter, Chinese automakers are increasingly adopting advanced FCCs for overcurrent protection in battery management systems, power electronics, and e-drive units. The country's push toward enhancing vehicle safety and reliability has made FCCs a vital component in electric drivetrains, further accelerating market growth.

Key players in the Global Automotive Fault Circuit Controller Market include Siemens, Mitsubishi Electric, Honeywell International, Infineon Technologies, ABB, Panasonic Corporation, Eaton, Bosch Automotive Electronics, General Electric (GE), and Schneider Electric. To strengthen their position in the automotive fault circuit controller market, companies are focusing on developing cutting-edge, reliable, and efficient solutions that meet the evolving safety standards of the automotive industry. They are investing heavily in research and development to innovate fault protection technologies, ensuring their products are optimized for high-voltage electric vehicles and connected cars. Additionally, these companies are expanding their partnerships with automotive manufacturers to integrate FCCs seamlessly into modern powertrains and battery management systems. Offering customized solutions that cater to the specific needs of different vehicle models and types has also become a priority. Companies enhance their market foothold by expanding their production capabilities and increasing their presence in emerging markets, where the adoption of electric vehicles rises.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Application

- 2.2.5 Technology

- 2.2.6 End use

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in vehicle electrification and high-voltage architecture adoption

- 3.2.1.2 Growing emphasis on passenger safety and regulatory compliance

- 3.2.1.3 Expansion of connected and autonomous vehicle technologies

- 3.2.1.4 Integration of fault detection systems in advanced driver-assistance systems (ADAS)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High complexity and cost of integration

- 3.2.2.2 Reliability issues in harsh automotive environments

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in electric vehicle (EV) manufacturing

- 3.2.3.2 Integration with advanced driver assistance systems (ADAS)

- 3.2.3.3 Regulatory push for electrical safety compliance

- 3.2.3.4 Growth in emerging automotive markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD, Million, Units)

- 5.1 Key trends

- 5.2 Fault circuit controllers (FCC)

- 5.3 Circuit protection devices

- 5.4 Sensors & monitoring units

- 5.5 Control modules

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD, Million, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedan

- 6.2.2 SUV

- 6.2.3 Hatchback

- 6.3 Commercial vehicles

- 6.3.1 LCVs (light commercial vehicles)

- 6.3.2 MCVs (medium commercial vehicles)

- 6.3.3 HCVs (heavy commercial vehicles)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD, Million, Units)

- 7.1 Key trends

- 7.2 Engine management systems

- 7.3 Battery management systems

- 7.4 Lighting systems

- 7.5 Infotainment and connectivity systems

- 7.6 Safety systems

- 7.7 HVAC (heating, ventilation, air conditioning)

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD, Million, Units)

- 8.1 Key trends

- 8.2 Traditional fault circuit controllers

- 8.3 Smart/intelligent fault circuit controllers

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD, Million, Units)

- 9.1 Key trends

- 9.2 OEM (original equipment manufacturers)

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Alstom

- 11.3 American Superconductor

- 11.4 Autoliv

- 11.5 Bosch Automotive Electronics

- 11.6 Continental

- 11.7 Denso

- 11.8 Eaton

- 11.9 General Electric (GE)

- 11.10 Honeywell International

- 11.11 Infineon Technologies

- 11.12 Liaoning Rongxin Electric Power Electronic Co.

- 11.13 Mitsubishi Electric

- 11.14 Nexans

- 11.15 Panasonic

- 11.16 Schneider Electric

- 11.17 Siemens

- 11.18 Superconductor Technologies

- 11.19 TE Connectivity

- 11.20 Valeo