|

市場調査レポート

商品コード

1871323

頭蓋顎顔面デバイス市場における機会、成長要因、業界動向分析、および2025年から2034年までの予測Craniomaxillofacial Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 頭蓋顎顔面デバイス市場における機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年10月29日

発行: Global Market Insights Inc.

ページ情報: 英文 177 Pages

納期: 2~3営業日

|

概要

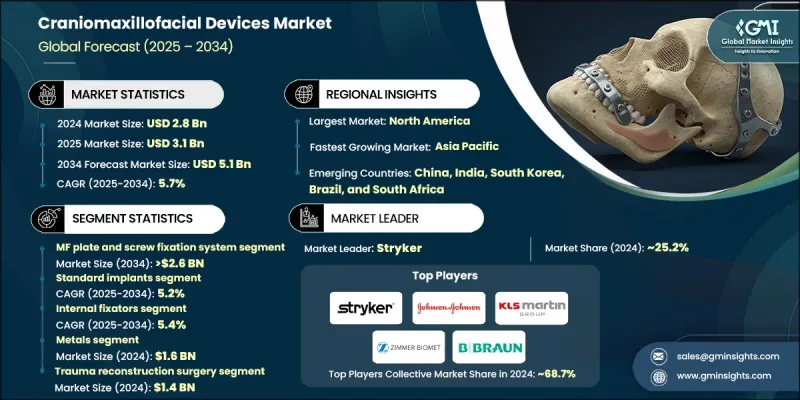

世界の頭蓋顎顔面用医療機器市場は、2024年に28億米ドルと評価され、2034年までにCAGR5.7%で成長し、51億米ドルに達すると予測されております。

市場成長の背景には、交通事故、スポーツ関連事故、暴力事件に起因する顔面損傷の増加があり、これが再建手術の需要を促進しております。さらに、小児における先天性顔面奇形も、小児外科手術における頭蓋顎顔面用医療機器の需要増加に寄与しております。回復が早く入院期間が短縮される低侵襲手術の動向も、市場成長の一因となっております。生体適合性金属などの外科用材料の進歩や、画像技術の継続的な改善は、手術結果の向上に重要な役割を果たしています。これらの革新により、外科医はより正確で低侵襲な手術を実施できるようになり、回復時間の短縮と合併症リスクの低減につながっています。先進的な画像システムの継続的な開発により、手術中のリアルタイム可視化が可能となり、精度と患者の全体的な安全性が向上しています。これらの技術が進化を続ける中、頭蓋顔面装置市場の成長に大きく寄与することが期待されています。さらに、発展途上国における医療費支出の増加が、頭蓋顔面装置へのアクセス拡大を促進しています。これらの地域における償還政策の改善は、特に複雑な顔面再建症例において、これらの装置をより利用しやすくするのに役立っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025-2034 |

| 開始時価値 | 28億米ドル |

| 予測金額 | 51億米ドル |

| CAGR | 5.7% |

MFプレートおよびスクリュー固定システムセグメントは、下顎骨、中顔面、頭蓋骨の骨折治療における信頼性から、2024年に52.4%のシェアを占めました。これらのシステムは、頭蓋顎顔面外科手術において最も広く使用されているものひとつであり続けています。骨片の正確な位置合わせを可能にし、回復の促進と治癒の向上に貢献します。MFプレートおよびスクリュー固定システムは、その簡便な適用性と効率的な安定化能力から、外科医に好まれています。

製品セグメント別では、内部固定器セグメントが2034年までCAGR 5.4%で成長すると予測されます。内部固定器は体内の安定化を実現し、外部感染リスクを低減する利点から普及が進んでいます。回復過程における骨癒合促進能力により、低侵襲手術において特に高く評価されています。この低侵襲手術への志向は、患者と外科医双方が求める、外傷性の少ない手術と回復期間の短縮というニーズに合致するものです。

米国頭蓋顔面外科用デバイス市場は、交通事故やスポーツ傷害の発生率が高く、これらが再建手術を必要とするケースが多いため、2024年には13億米ドルと評価されました。政府による医療アクセス改善プログラムと医療機器の技術革新により、米国の病院や診療所では先進的な頭蓋顎顔面(CMF)用医療機器の導入が拡大しています。顔面再建手術への高い需要と最先端医療技術へのアクセス向上という相乗効果により、今後数年間にわたり米国市場の成長が持続すると予想されます。

メドトロニック、ストライカー、ジョンソン・エンド・ジョンソンなど、世界の頭蓋顎顔面デバイス市場の主要企業は、戦略的な買収、製品の革新、技術の進歩を通じて、市場での存在感の拡大に注力しています。B BraunやIntegraなどの企業は、手術の成果を向上させるための先進的な画像診断システムや生体適合性材料を取り入れることで、自社製品ポートフォリオの強化を図っています。さらに、Zimmer Biomet社やKLSマーティン社などの企業は、競争力を維持し、高品質で効率的、かつ低侵襲のソリューションを提供するために、研究開発への投資を増やしています。これらの戦略は、急速に進化する頭蓋顎顔面デバイス市場において、これらの企業が足場を強化するのに役立っています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 顔面損傷および外傷の発生率の増加

- 美容整形手術の普及拡大

- 先天性顔面奇形の増加傾向

- 拡大する医療支出

- 業界の潜在的リスク&課題

- 頭蓋顎顔面手術の高コスト

- 市場機会

- 生体吸収性および生体適合性材料の成長

- 新興市場における拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 価格分析、2024

- 頭蓋顎顔面インプラントの数量(単位)、地域別、2021-2034

- 患者特異的頭蓋顎顔面インプラント(競合別)

- バリューチェーン分析

- 将来の市場動向

- 償還シナリオ

- 技術情勢

- 現行技術

- 新興技術

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- MFプレートおよびスクリュー固定システム

- 頭蓋骨皮弁固定システム

- 頭蓋顔面骨延長システム

- 顎関節置換システム

- 骨移植代替システム

第6章 市場推計・予測:インプラントの種類別、2021-2034

- 主要動向

- 標準インプラント

- カスタム/患者特異的インプラント

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 内固定器

- 外固定器

第8章 市場推計・予測:材料別、2021-2034

- 主要動向

- 金属

- 生体吸収性材料

- セラミックス

- ポリマー

第9章 市場推計・予測:用途別、2021-2034

- 主要動向

- 外傷再建手術

- 頭蓋手術

- 中顔面手術

- 下顎手術

- 眼窩底再建手術

- 矯正歯科手術

- 形成外科

第10章 市場推計・予測:吸収性別、2021-2034

- 主要動向

- 非吸収性固定具

- 吸収性固定具

第11章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- その他の最終用途

第12章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- オランダ

- スイス

- ベルギー

- スウェーデン

- ポーランド

- オーストリア

- デンマーク

- アイルランド

- ポルトガル

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- タイ

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- チリ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第13章 企業プロファイル

- Acumed

- Anatomics

- B. BRAUN

- Beijing Naton Medical Technology

- BIOPLATE

- Cavendish Implants

- CranioTech

- JEIL MEDICAL

- Johnson &Johnson

- Kelyniam Global

- KLS Martin Group

- Matrix Surgical USA

- Medartis AG

- MEDPRIN

- Medtronic

- Stryker

- Xilloc Medical

- Zimmer Biomet