|

市場調査レポート

商品コード

1750618

コンピュータビジョンにおけるAI市場の機会、成長促進要因、産業動向分析、2025年~2034年予測AI in Computer Vision Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| コンピュータビジョンにおけるAI市場の機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月12日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

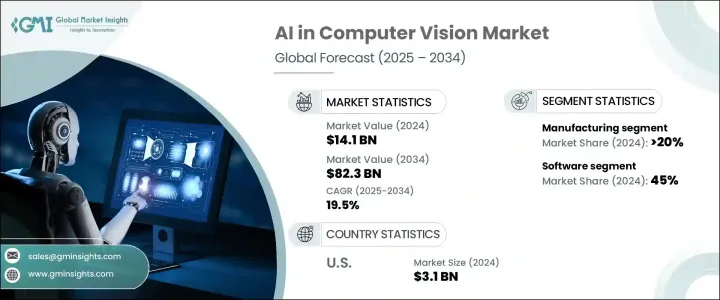

世界のコンピュータビジョンにおけるAI市場は、2024年に141億米ドルと評価され、CAGR 19.5%で成長し、2034年には823億米ドルに達すると推定されています。

ディープラーニング技術、特にCNN(Convolutional Neural Networks:畳み込みニューラルネットワーク)やトランスフォーマーモデルの進歩により、視覚データ処理の精度と効率が向上しています。これらの開発により、機械は複雑な視覚情報を解釈できるようになり、物体検出、分類、認識などの応用が容易になります。AIシステムが多様で複雑な視覚データの処理に習熟するにつれ、その有用性はヘルスケア、自動車、小売、製造などさまざまな分野に広がっています。監視カメラ、ドローン、スマートフォンなどのソースから得られる視覚データの量が増加しているため、自動分析ツールの開発が必要となっています。

AIを搭載したコンピュータビジョンシステムは、大規模な画像や映像のデータセットをリアルタイムで処理・分析し、セキュリティやヘルスケアなどの産業にとって極めて重要な洞察をタイムリーかつ正確に提供することができます。これらのシステムは、従来の方法をはるかに上回るスピードと精度で、異常の検出、顔の認識、物体の識別、活動の監視を行うことができます。セキュリティ分野では、プロアクティブな脅威検知や自動監視が可能になり、ヘルスケア分野では、医療画像による早期診断、手術支援、患者モニタリングの強化が可能になります。こうした技術が進化を続けるにつれ、幅広い用途で業務効率、安全性、意思決定の向上に不可欠な役割を果たすようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 141億米ドル |

| 予測金額 | 823億米ドル |

| CAGR | 19.5% |

2024年、製造業セクターのシェアは20%で、30億米ドルとなります。AI主導のビジョンシステムを製造業に組み込むことで、自動化された品質管理が促進され、人的ミスが減少し、一貫した製品規格が確保されます。これらのシステムは、リアルタイムで欠陥や異常を特定することで業務効率を高め、生産プロセスの最適化と無駄の削減につながります。AI、モノのインターネット(IoT)、ロボット工学を組み合わせたインダストリー4.0コンセプトの採用が、製造環境におけるコンピュータビジョン技術の展開を加速しています。

2024年にはソフトウェア分野が市場をリードし、45%のシェアを獲得しました。ソフトウェアソリューションはコンピュータビジョンにおけるAIに不可欠であり、顔認識、物体検出、画像分類などの複雑なタスクを可能にします。これらのソフトウェア・プラットフォームは高度にカスタマイズ可能で、医療画像、自律走行ナビゲーション、小売分析など、特定の業界のニーズに適応することができます。AIソフトウェアは柔軟性と拡張性に優れているため、技術力の強化と高い投資収益率の実現を目指す企業にとって好ましい投資先となっています。

北米市場は2024年に31億米ドルを創出しましたが、これは主要テクノロジー企業の存在、政府および民間セクターの多額の投資、強固な研究開発エコシステムに起因します。マサチューセッツ工科大学(MIT)やスタンフォード大学(Stanford)などの研究開発機関と企業の研究所がAI技術の開発に貢献しています。米国では、自動車、ヘルスケア、小売などの業界がAIを搭載したコンピュータビジョンツールをいち早く採用し、自動化、高度な監視、診断、物流業務に活用しています。

コンピュータビジョンにおけるAI業界の主要企業には、Amazon、NVIDIA、IBM、Microsoft、Intel、Google、Advanced Micro Devices Inc.、Cognex Corporation、Teledyne Technologies、Basler AGなどがあります。これらの企業は、さまざまな分野でAIを活用したビジョンシステムの開発と導入の最前線に立ち、イノベーションを推進し、市場の裾野を広げています。市場ポジションを強化するために、コンピュータビジョンにおけるAI業界の企業はいくつかの重要な戦略を採用しています。これには、AIアルゴリズムとハードウェアの能力を強化するための研究開発への投資、技術的専門知識と市場リーチを拡大するための戦略的パートナーシップと協力関係の形成、さまざまな業界の進化するニーズに対応するための製品イノベーションへの注力などが含まれます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- ハードウェアプロバイダー

- ソフトウェアプロバイダー

- サービスプロバイダー

- テクノロジープロバイダー

- 最終用途

- 利益率分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーとイノベーションの情勢

- ロボティックプロセスオートメーション

- AIに最適化されたハードウェア

- ディープラーニングプラットフォーム

- 特許分析

- 主なニュースと取り組み

- コンピュータビジョンにおけるAIの使用例

- 規制情勢

- 影響要因

- 促進要因

- ディープラーニングとAIアルゴリズムの急速な進歩

- 視覚データ量の増加

- 自動化と品質管理の必要性の高まり

- エッジコンピューティングの統合の増加

- 業界の潜在的リスク&課題

- データのプライバシーとセキュリティに関する懸念

- レガシーシステムとの統合

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021~2034年

- 主要動向

- ハードウェア

- カメラと画像センサー

- プロセッサ(GPU、TPU、VPU)

- 統合システム

- エッジコンピューティングデバイス

- ソフトウェア

- 開発フレームワークとツール

- ビジョンAPIとSDK

- 事前学習済みモデル

- カスタムビジョンソリューション

- クラウドベースのビジョンサービス

- サービス

- 実装と統合

- トレーニングとサポート

- コンサルティング

- メンテナンスとアップグレード

第6章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 予測メンテナンス

- 品質保証と検査

- ポジショニングとガイダンス

- 識別と測定

- その他

第7章 市場推計・予測:最終用途別、2021~2034年

- 主要動向

- 自動車および輸送

- 製造業

- 政府

- 小売り

- BFSI

- ヘルスケア

- その他

第8章 市場推計・予測:機能別、2021~2034年

- 主要動向

- トレーニング

- 推論

第9章 市場推計・予測:技術別、2021~2034年

- 主要動向

- ML

- Gen AI

第10章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Advanced Micro Device

- Amazon

- Basler

- Clarifai

- Cognex

- Deepomatic

- Graphcore

- Hailo

- IBM

- Intel

- Keyence

- Microsoft

- NVIDIA

- Omron

- Qualcomm

- Sick

- Sony

- Teledyne Technologies

- Texas Instruments

The Global AI in Computer Vision Market was valued at USD 14.1 billion in 2024 and is estimated to grow at a CAGR of 19.5% to reach USD 82.3 billion by 2034, driven by the advancements in deep learning technologies, particularly Convolutional Neural Networks (CNNs) and transformer models, have enhanced the accuracy and efficiency of visual data processing. These developments enable machines to interpret complex visual information, facilitating applications such as object detection, classification, and recognition. As AI systems become more adept at handling diverse and intricate visual data, their utility spans various sectors, including healthcare, automotive, retail, and manufacturing. The increasing volume of visual data from sources like surveillance cameras, drones, and smartphones necessitates the development of automated analysis tools.

AI-powered computer vision systems can process and analyze large image and video datasets in real time, providing timely and accurate insights crucial for industries like security and healthcare. These systems can detect anomalies, recognizing faces, identifying objects, and monitoring activities with a level of speed and precision that far exceeds traditional methods. In security, this enables proactive threat detection and automated surveillance, while in healthcare, it facilitates early diagnosis through medical imaging, supports surgical assistance, and enhances patient monitoring. As these technologies continue to evolve, they are playing an increasingly integral role in improving operational efficiency, safety, and decision-making across a wide range of applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.1 Billion |

| Forecast Value | $82.3 Billion |

| CAGR | 19.5% |

In 2024, the manufacturing sector held a 20% share, valued at USD 3 billion. Integrating AI-driven vision systems in manufacturing facilitates automated quality control, reducing human error and ensuring consistent product standards. These systems enhance operational efficiency by identifying defects and anomalies in real time, leading to optimized production processes and reduced waste. The adoption of Industry 4.0 concepts, which combine AI, the Internet of Things (IoT), and robotics, is accelerating the deployment of computer vision technologies in manufacturing environments.

The software segment led the market in 2024, capturing 45% share. Software solutions are integral to AI in computer vision, enabling complex tasks such as facial recognition, object detection, and image classification. These software platforms are highly customizable, allowing adaptation to specific industry needs, including medical imaging, autonomous vehicle navigation, and retail analytics. The flexibility and scalability of AI software make it a preferred investment for companies seeking to enhance their technological capabilities and achieve a higher return on investment.

North America AI in Computer Vision Market generated USD 3.1 billion in 2024, attributed to the presence of leading technology companies, substantial government and private sector investments, and a robust research and development ecosystem. Institutions such as MIT and Stanford, along with corporate research labs, contribute to developing AI technologies. Industries in the U.S., including automotive, healthcare, and retail, are early adopters of AI-powered computer vision tools, leveraging them for automation, advanced surveillance, diagnostics, and logistical operations.

Key players in the AI in Computer Vision Industry include Amazon, NVIDIA, IBM, Microsoft, Intel, Google, Advanced Micro Devices Inc., Cognex Corporation, Teledyne Technologies, and Basler AG. These companies are at the forefront of developing and deploying AI-driven vision systems across various sectors, driving innovation and expanding the market's reach. To strengthen their market position, companies in the AI in computer vision industry are adopting several key strategies. These include investing in research and development to enhance the capabilities of AI algorithms and hardware, forming strategic partnerships and collaborations to expand their technological expertise and market reach, and focusing on product innovation to meet the evolving needs of different industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Hardware providers

- 3.2.2 Software providers

- 3.2.3 Service providers

- 3.2.4 Technology providers

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Impact of Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook & future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.5.1 Robotic process automation

- 3.5.2 AI optimized hardware

- 3.5.3 Deep learning platform

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Use cases of AI in computer vision

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rapid advancements in deep learning & AI algorithms

- 3.10.1.2 Rise in amount of visual data

- 3.10.1.3 Growing need for automation and quality control

- 3.10.1.4 Increase in the edge computing integration

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Data privacy and security concerns

- 3.10.2.2 Integration with legacy systems

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Cameras and image sensors

- 5.2.2 Processors (GPUs, TPUs, VPUs)

- 5.2.3 Integrated systems

- 5.2.4 Edge computing devices

- 5.3 Software

- 5.3.1 Development frameworks and tools

- 5.3.2 Vision APIs and SDKs

- 5.3.3 Pre-trained models

- 5.3.4 Custom vision solutions

- 5.3.5 Cloud-based vision services

- 5.4 Services

- 5.4.1 Implementation and integration

- 5.4.2 Training and support

- 5.4.3 Consulting

- 5.4.4 Maintenance and upgrades

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Predictive maintenance

- 6.3 Quality assurance and inspection

- 6.4 Positioning and guidance

- 6.5 Identification and measurement

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Automotive and transportation

- 7.3 Manufacturing

- 7.4 Government

- 7.5 Retail

- 7.6 BFSI

- 7.7 Healthcare

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Function, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Training

- 8.3 Inferences

Chapter 9 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 ML

- 9.3 Gen AI

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Advanced Micro Device

- 11.2 Amazon

- 11.3 Basler

- 11.4 Clarifai

- 11.5 Cognex

- 11.6 Deepomatic

- 11.7 Google

- 11.8 Graphcore

- 11.9 Hailo

- 11.10 IBM

- 11.11 Intel

- 11.12 Keyence

- 11.13 Microsoft

- 11.14 NVIDIA

- 11.15 Omron

- 11.16 Qualcomm

- 11.17 Sick

- 11.18 Sony

- 11.19 Teledyne Technologies

- 11.20 Texas Instruments