緑内障治療の市場機会、成長促進要因、産業動向分析、予測、2025年~2034年

Glaucoma Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 162 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750580

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

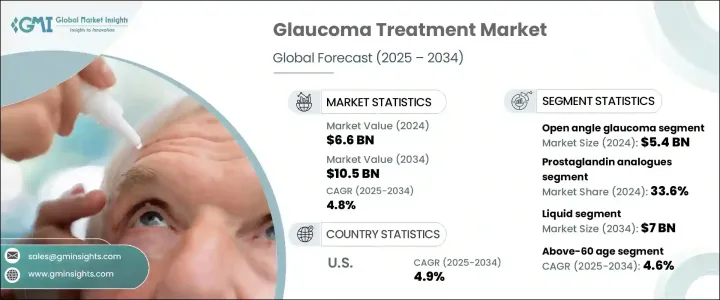

世界の緑内障治療市場は2024年に66億米ドルと評価され、CAGR 4.8%で成長し、2034年には105億米ドルに達すると推定されています。

世界人口の高齢化が進むにつれて、加齢に関連した眼疾患の症例はより頻繁に、より重篤になっており、早期診断と長期的ケアの必要性が高まっています。緑内障発症の重大な危険因子である糖尿病や高血圧などの慢性疾患も増加傾向にあり、様々な層で効果的かつ長期的な治療オプションに対する需要が高まる一因となっています。

政府や保健機関は、早期検診や定期的な眼科検診を推進する啓発キャンペーンに力を入れ始めており、緑内障の早期発見に役立っています。これにより、治療開始が顕著に増加しています。また、Rhoキナーゼ阻害薬や合剤治療など、新しい薬剤クラスの採用も、治療の選択肢を広げ、患者の転帰を改善しています。さらに、医療インフラの改善と可処分所得の増加(特に新興市場)により、眼科医療がより身近なものとなり、より幅広い層の人々がタイムリーで高度な緑内障管理を受けられるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 66億米ドル |

| 予測金額 | 105億米ドル |

| CAGR | 4.8% |

開放隅角緑内障は依然として最も多く診断される疾患であり、世界全体の症例の70%以上を占め、2024年の市場規模は54億米ドルです。緑内障の治療は、不可逆的な視神経損傷を防ぐために眼圧(IOP)を管理することが中心です。ほとんどの治療法は、β遮断薬、α作動薬、炭酸脱水酵素阻害薬、プロスタグランジンアナログなど、眼圧を下げる薬物に焦点を当てています。開放隅角緑内障はゆっくりと開発され、多くの場合、重大な視力低下が起こるまで明らかな症状はないです。その慢性的な性質は、患者が継続的かつ長期的なケアを必要とすることを意味し、医薬品ソリューションと定期的なモニタリングサービスに対する持続的な需要を生み出しています。

体液の排出を促進することで眼圧を下げるプロスタグランジンアナログは、2024年の治療市場で33.6%と最も高いシェアを占め、2034年には37億米ドルに達すると予測されています。その有効性と比較的穏やかな副作用プロファイルにより、開放隅角緑内障の管理に広く処方されています。高齢化が進む中、特に防腐剤フリーで使い勝手の良い点眼剤を選ぶ患者が増えるにつれて、これらの薬剤の需要はさらに高まると予想されます。

米国の緑内障治療2024年の市場規模は22億4,000万米ドルで、2034年までCAGR 4.9%で成長すると予測されています。同国では高齢化が進み、認知度が高いことに加え、医薬品イノベーターの存在感が強く、先進的な治療オプションへの需要が引き続き高まっています。確立されたヘルスケア・インフラが早期診断と処方療法への広範なアクセスを支える一方、臨床試験とFDA承認への継続的な投資が利用可能な医薬品パイプラインを急速に拡大しています。保険適用の拡大や有利な償還政策が、高齢者やハイリスクグループの治療導入をさらに後押ししています。

Novartis, Pfizer, Santen Pharmaceutical, Sun Pharmaceutical, Thea, Alcon, Cipla, AbbVie, Bausch & Lomb, Inotek Pharmaceuticals, Eyepoint Pharmaceuticals, Teva Pharmaceutical, Merck, Grevis Pharmaceuticalsなどの企業が、この分野で積極的に競争しています。主要企業は緑内障治療市場での競争力を確保するため、有効性と安全性を向上させた次世代治療薬を開発するための研究開発に多額の投資を行っています。治療レジメンを簡素化し、患者のアドヒアランスを向上させるため、合剤に注力しています。パートナーシップや販売網を通じて高成長の新興市場に進出することも重要な戦略です。さらに、早期介入と継続的なケアをサポートするため、企業はデジタル関与ツールや遠隔患者モニタリング技術を強化しています。戦略的提携、パイプラインの多様化、製品ライフサイクル管理は、世界各地域での市場でのポジショニングを強化する上で、依然として中心的な役割を担っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界中で緑内障の罹患率が増加

- 治療介入における技術的進歩

- 緑内障治療の進行中の臨床試験と製品発売の増加

- 発展途上国および発展途上国における眼科医療に関する啓発活動の拡大

- 業界の潜在的リスク&課題

- 薬に伴う副作用

- 厳格な規制要件

- 促進要因

- 成長可能性分析

- パイプライン分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:疾患タイプ別、2021年~2034年

- 主要動向

- 開放隅角緑内障

- 閉塞隅角緑内障

- その他

第6章 市場推定・予測:薬剤クラス別、2021年~2034年

- 主要動向

- プロスタグランジン類似体

- ベータ遮断薬

- アルファアドレナリン作動薬

- 炭酸脱水酵素阻害剤

- その他

第7章 市場推定・予測:処方別、2021年~2034年

- 主要動向

- 固体

- 液体

第8章 市場推定・予測:年齢別、2021年~2034年

- 主要動向

- 18歳未満

- 19~40歳

- 41~60歳

- 60歳超

第9章 市場推定・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第10章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- AbbVie

- Alcon

- Bausch &Lomb

- Cipla

- Eyepoint Pharmaceuticals

- Grevis Pharmaceuticals

- Inotek Pharmaceuticals

- Merck

- Novartis

- Pfizer

- Santen Pharmaceutical

- Sun Pharmaceutical

- Teva Pharmaceutical

- Thea

目次

The Global Glaucoma Treatment Market was valued at USD 6.6 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 10.5 billion by 2034, attributed to the rising incidence of glaucoma worldwide, especially among older adults. As the global population continues to age, cases of age-related ocular disorders are becoming more frequent and severe, prompting a greater need for early diagnosis and long-term care. Chronic illnesses such as diabetes and hypertension-both significant risk factors for developing glaucoma-are also on the rise, which further contributes to increasing demand for effective and long-lasting treatment options across various demographics.

Governments and health agencies have started focusing on awareness campaigns to promote early screening and routine eye examinations, which is helping detect glaucoma at earlier stages. This has led to a notable rise in treatment initiations. The market is also benefiting from the adoption of novel drug classes, including Rho kinase inhibitors and fixed-dose combination therapies, which are expanding treatment alternatives and improving patient outcomes. Additionally, improving healthcare infrastructure and growing disposable incomes-especially in emerging markets-are making ophthalmic care more accessible, enabling a broader segment of the population to pursue timely and advanced glaucoma management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.6 Billion |

| Forecast Value | $10.5 Billion |

| CAGR | 4.8% |

Open-angle glaucoma remains the most diagnosed form of the disease, accounting for more than 70% of global cases and valued at USD 5.4 billion in 2024. Treating glaucoma revolves around managing intraocular pressure (IOP) to prevent irreversible optic nerve damage. Most therapies focus on medications that help reduce IOP, including beta-blockers, alpha agonists, carbonic anhydrase inhibitors, and prostaglandin analogs. Open angle glaucoma condition develops slowly and often without obvious symptoms until significant vision loss occurs. Its chronic nature means patients require continuous and long-term care, creating sustained demand for pharmaceutical solutions and regular monitoring services.

Prostaglandin analogs, which help lower eye pressure by enhancing fluid drainage, commanded the highest share of the treatment market in 2024, making up 33.6% share and is projected to reach USD 3.7 billion by 2034. Their effectiveness and relatively mild side effect profile make them widely prescribed for managing open-angle glaucoma. With aging populations increasing, the demand for these medications is expected to climb further, particularly as more patients opt for preservative-free and user-friendly eye drop formulations.

U.S. Glaucoma Treatment Market generated USD 2.24 billion in 2024 and is set to grow at a 4.9% CAGR through 2034. The country's aging population and high awareness levels, coupled with the strong presence of pharmaceutical innovators, continue to fuel demand for advanced treatment options. A well-established healthcare infrastructure supports early diagnosis and widespread access to prescription therapies, while ongoing investments in clinical trials and FDA approvals are rapidly expanding the available drug pipeline. Increased insurance coverage and favorable reimbursement policies are further supporting treatment adoption among the elderly and high-risk groups.

Companies like Novartis, Pfizer, Santen Pharmaceutical, Sun Pharmaceutical, Thea, Alcon, Cipla, AbbVie, Bausch & Lomb, Inotek Pharmaceuticals, Eyepoint Pharmaceuticals, Teva Pharmaceutical, Merck, and Grevis Pharmaceuticals are actively competing in this space. To secure a competitive edge in the glaucoma treatment market, leading companies are investing heavily in R&D to develop next-generation therapies with improved efficacy and safety. They are focusing on fixed-dose combinations to simplify treatment regimens and improve patient adherence. Expanding into high-growth emerging markets through partnerships and distribution networks is another key strategy. Additionally, firms are enhancing digital engagement tools and remote patient monitoring technologies to support early intervention and ongoing care. Strategic collaborations, pipeline diversification, and product lifecycle management remain central to strengthening market positioning across global regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of glaucoma disease worldwide

- 3.2.1.2 Technological advancements in therapeutic interventions

- 3.2.1.3 Increasing ongoing clinical trials and product launches for glaucoma treatment

- 3.2.1.4 Growing awareness initiatives regarding eye care in underdeveloped and developing nations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects associated with the drugs

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pipeline analysis

- 3.5 Regulatory landscape

- 3.6 Trump administration tariffs

- 3.6.1 Impact on trade

- 3.6.1.1 Trade volume disruptions

- 3.6.1.2 Retaliatory measures

- 3.6.2 Impact on the Industry

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.2.1.1 Price volatility in key materials

- 3.6.2.1.2 Supply chain restructuring

- 3.6.2.1.3 Production cost implications

- 3.6.2.2 Demand-side impact (selling price)

- 3.6.2.2.1 Price transmission to end markets

- 3.6.2.2.2 Market share dynamics

- 3.6.2.2.3 Consumer response patterns

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.3 Key companies impacted

- 3.6.4 Strategic industry responses

- 3.6.4.1 Supply chain reconfiguration

- 3.6.4.2 Pricing and product strategies

- 3.6.4.3 Policy engagement

- 3.6.5 Outlook and future considerations

- 3.6.1 Impact on trade

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Open angle glaucoma

- 5.3 Angle closure glaucoma

- 5.4 Other disease types

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Prostaglandin analogs

- 6.3 Beta-blockers

- 6.4 Alpha adrenergic agonist

- 6.5 Carbonic anhydrase inhibitors

- 6.6 Other drug classes

Chapter 7 Market Estimates and Forecast, By Formulation, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Solid

- 7.3 Liquid

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Below 18

- 8.3 19 - 40

- 8.4 41 - 60

- 8.5 Above 60

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Retail pharmacies

- 9.4 Online pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbbVie

- 11.2 Alcon

- 11.3 Bausch & Lomb

- 11.4 Cipla

- 11.5 Eyepoint Pharmaceuticals

- 11.6 Grevis Pharmaceuticals

- 11.7 Inotek Pharmaceuticals

- 11.8 Merck

- 11.9 Novartis

- 11.10 Pfizer

- 11.11 Santen Pharmaceutical

- 11.12 Sun Pharmaceutical

- 11.13 Teva Pharmaceutical

- 11.14 Thea

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 162 Pages

- 納期

- 2~3営業日