|

市場調査レポート

商品コード

1750533

藻類由来成分の市場機会、成長促進要因、産業動向分析、予測、2025年~2034年Algae-based Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 藻類由来成分の市場機会、成長促進要因、産業動向分析、予測、2025年~2034年 |

|

出版日: 2025年05月13日

発行: Global Market Insights Inc.

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

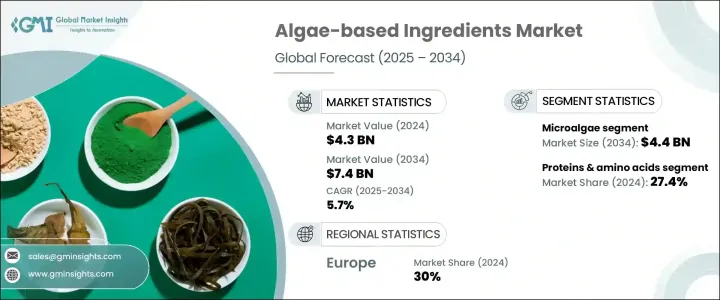

世界の藻類由来成分市場は、2024年に43億米ドルと評価され、消費者が生活習慣病と闘うための栄養代替品を求める傾向が強まる中、植物由来成分や機能性成分への需要が高まり、CAGR 5.7%で成長し、2034年には74億米ドルに達すると推定されます。

肥満、心血管疾患、2型糖尿病などの代謝異常が、食生活の乱れや座りっぱなしのライフスタイルのために一般的になりつつある中、健康をサポートする天然成分への嗜好が高まっています。藻類由来の化合物は、オメガ3脂肪酸、抗酸化物質、必須アミノ酸、植物性タンパク質など、ユニークなメリットを提供します。これらの特性により、藻類は機能性食品、栄養補助食品、栄養補助食品に最適な成分として位置づけられています。

ウェルネスが世界の優先事項になるにつれ、藻類由来成分は、人間の健康における予防的・治療的な役割について認知され続けています。消費者は、クリーンラベルや持続可能な生活の動向に沿った天然植物由来のソリューションにますます惹かれており、藻類はこのような動向にぴったりと当てはまる。これらの成分は、高い栄養密度、生物活性化合物、免疫力、心臓血管の健康、認知機能、炎症抑制をサポートする機能的な利点という珍しい組み合わせを提供します。その汎用性により、栄養補助食品や強化食品からスキンケアや医薬品製剤まで、さまざまな用途に組み込むことができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 43億米ドル |

| 予測金額 | 74億米ドル |

| CAGR | 5.7% |

微細藻類セグメントは、その栄養豊富なプロファイルと、食品、栄養補助食品、化粧品にまたがる広範なアプリケーションにより、2034年までに44億米ドルに達すると予想されています。スピルリナやアスタキサンチンのような化合物は、その高いタンパク質、脂質、抗酸化物質の含有量のおかげで人気を集めています。光バイオリアクターのような培養方法の革新は、微細藻類生産の効率と拡張性を向上させています。一方、ハイドロコロイド生産における有用性から、大藻は依然として重要です。寒天、アルギン酸、カラギーナンのような抽出物は、その安定化と増粘特性のために食品産業で不可欠であり、マクロ藻類を不可欠な原料にしています。

製品セグメンテーションに基づくと、2024年にはタンパク質とアミノ酸のセグメントが27.4%を占めて最大の市場シェアを占め、2034年までCAGR 5.7%で安定した成長が見込まれています。ベジタリアンやビーガンのライフスタイルの急増は、藻類ベースの代替タンパク質への需要を生み出しています。抽出技術の向上により、これらのタンパク質は従来の動物性・植物性タンパク質とより効果的に競合できるようになりました。藻類由来のタンパク質は、バランスのとれたアミノ酸組成と高い栄養密度により、ますます人気が高まっています。スポーツ栄養、代替食、機能性スナックなどでその存在感が増しています。藻類由来のオメガ3脂肪酸もまた、特に乳児用調製粉乳や心臓の健康サプリメントなど、健康志向の製品ラインに欠かせないものとなりつつあります。

欧州の藻類由来成分市場は、2024年に30%の市場シェアを占め、持続可能性への積極的な姿勢とグリーン技術の革新が原動力となっています。カーボンニュートラルや植物由来の製品開発を支援する規制など、この地域全体の規制枠組みが藻類由来成分採用のための肥沃な環境を作り出しています。政府や民間の利害関係者は、バイオエコノミーの取り組みに多額の投資を行い、合成化合物や動物由来化合物に代わる実行可能な代替物として藻類の探求を奨励しています。飲食品分野では、ビーガン、アレルゲンフリー、栄養価の高い食材を求める消費者の需要の高まりに応えるため、メーカーが藻類に注目しています。

主な市場参入企業には、Corbion、Aliga Microalgae、Bioriginal Food and Science Corp、Cargill Inc、Marine Hydrocolloidsなどがあります。これらの企業は、市場での地位を強化するために積極的な戦略を推進しています。持続可能な生産方法に焦点を当て、環境に優しく拡張性のある培養システムを開発しています。いくつかの企業は、藻類ベースの化合物の生物学的利用能と機能性を高めるための研究開発に投資しています。製品リーチを拡大するため、食品や化粧品ブランドとの戦略的提携も進んでいます。さらに、より幅広い消費者層にアピールするため、クリーンラベル処方を模索し、藻類タンパク質パウダー、強化オイル、スキンケア活性剤などの革新的な製品を発売しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 主要メーカー

- 販売代理店

- 業界全体の利益率

- サプライチェーンと流通分析

- 原材料調達

- 生産と製造

- コールドチェーンインフラ

- 流通チャネル

- サプライチェーンの課題と最適化

- 持続可能な慣行

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国、2021-2024

- 主要輸出国、2021-2024

- 影響要因

- 促進要因

- 藻類製品の生産を促進する政府の取り組み

- 栄養補助食品業界からの利用の増加と需要の増加

- 冷凍技術の技術的進歩

- 藻類由来製品に対する消費者の認知度と受容度の高まり

- 業界の潜在的リスク&課題

- コールドチェーンインフラの課題

- 藻類栽培への環境影響

- 市場機会

- 促進要因

- 原材料の情勢

- 製造業の動向

- 技術の進化

- 価格分析とコスト構造

- 価格動向(米ドル/トン)

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東アフリカ

- 価格要因(原材料、エネルギー、労働力)

- 地域による価格差

- コスト構造の内訳

- 収益性分析

- 価格動向(米ドル/トン)

- 規制の枠組みと基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業ヒートマップ分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- 主要プレーヤーによる最近の動向と影響分析

- 企業分類

- 参加者の概要

- 財務実績

- 製品ベンチマーク

第5章 市場推定・予測:由来別、2021年~2034年

- 主要動向

- 微細藻類

- スピルリナ(アルスロスピラ)

- クロレラ

- ドゥナリエラ

- ヘマトコッカス

- シゾキトリウム

- ナンノクロロプシス

- その他

- 大型藻類(海藻)

- 紅藻(紅藻類)

- 褐藻(褐藻類)

- 緑藻(緑藻類)

- その他

- シアノバクテリア(藍藻類)

- アファニゾメノン・フロス・アクア

- その他

第6章 市場推定・予測:成分タイプ別、2021年~2034年

- 主要動向

- タンパク質とアミノ酸

- 藻類タンパク質(ホール)

- タンパク質濃縮物

- タンパク質分離物

- ペプチドとアミノ酸

- 脂質と脂肪酸

- オメガ3脂肪酸(DHA/EPA)

- 極性脂質

- その他

- 炭水化物と食物繊維

- アルギン酸塩

- カラギーナン

- 寒天

- フコイダン

- その他

- 色素と抗酸化物質

- クロロフィル

- フィコシアニン

- アスタキサンチン

- フコキサンチン

- その他

- ビタミンとミネラル

- 藻類成分(ホール)

- その他

第7章 市場推定・予測:形態別、2021年~2034年

- 主要動向

- 粉末

- 液体

- ジェル

- フレーク

- 錠剤・カプセル

- その他

第8章 市場推定・予測:生産方法別、2021年~2034年

- 主要動向

- 開放型培養池システム

- 閉鎖型培養システム

- 光バイオリアクター

- 発酵槽

- その他

- ハイブリッドシステム

- 野生採取(大型藻類)

- その他

第9章 市場推定・予測:用途別、2021年~2034年

- 主要動向

- 食品・飲料

- ベーカリー&菓子類

- 乳製品・乳製品代替品

- 肉と魚介類の代替品

- 飲料

- スナックとコンビニ食品

- ソース、ドレッシング、調味料

- その他

- 栄養補助食品

- タンパク質サプリメント

- オメガ3サプリメント

- 抗酸化サプリメント

- 一般健康サプリメント

- その他

- 動物飼料

- 養殖飼料

- 家禽飼料

- 豚飼料

- ペットフード

- その他

- 化粧品・パーソナルケア

- スキンケア

- ヘアケア

- その他

- 医薬品

- バイオ燃料とバイオエネルギー

- その他

第10章 市場推定・予測:最終用途産業別、2021年~2034年

- 主要動向

- 食品・飲料業界

- 栄養補助食品業界

- 動物飼料業界

- 化粧品・パーソナルケア業界

- 製薬業界

- エネルギー業界

- その他

第11章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第12章 企業プロファイル

- AEP Colloids

- AgarGel

- Aliga Microalgae

- Bioriginal Food &Science Corp

- Cargill Inc.

- Corbion

- CP Kelco U.S. Inc

- Gino Biotech

- Hispanagar SA

- KIMICA

- Marine Hydrocolloids

- Taiwan Chlorella Manufacturing Company

- Triton

The Global Algae-based Ingredients Market was valued at USD 4.3 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 7.4 billion by 2034, driven by the rising demand for plant-based and functional ingredients, as consumers increasingly seek nutritional alternatives to combat lifestyle-related diseases. With metabolic disorders such as obesity, cardiovascular conditions, and type 2 diabetes becoming more common due to poor eating habits and sedentary lifestyles, there's a growing preference for natural health-supportive ingredients. Algae-derived compounds offer a unique set of benefits, including omega-3 fatty acids, antioxidants, essential amino acids, and plant-based proteins. These properties have positioned algae as a go-to ingredient in functional foods, dietary supplements, and nutraceutical formulations.

As wellness becomes a global priority, algae-based ingredients continue gaining recognition for their preventative and therapeutic roles in human health. Consumers are increasingly drawn to natural, plant-derived solutions that align with clean-label and sustainable living trends, and algae fits perfectly into this narrative. These ingredients offer a rare combination of high nutritional density, bioactive compounds, and functional benefits that support immunity, cardiovascular health, cognitive function, and inflammation reduction. Their versatility allows them to be incorporated across various applications, from dietary supplements and fortified foods to skincare and pharmaceutical formulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.3 Billion |

| Forecast Value | $7.4 Billion |

| CAGR | 5.7% |

The microalgae segment is expected to reach USD 4.4 billion by 2034, due to their nutrient-rich profile and broad application across food, nutraceutical, and cosmetic products. Compounds like spirulina and astaxanthin are gaining traction thanks to their high protein, lipid, and antioxidant content. Innovations in cultivation methods, such as photobioreactors, are improving the efficiency and scalability of microalgae production. On the other hand, macroalgae remain relevant due to their utility in hydrocolloid production. Extracts like agar, alginate, and carrageenan are vital in the food industry for their stabilizing and thickening properties, making macroalgae an essential raw material.

Based on product segmentation, the proteins and amino acids segment held the largest market share in 2024, accounting for 27.4%, and is expected to grow steadily at a CAGR of 5.7% through 2034. The surge in vegetarian and vegan lifestyles creates demand for algae-based protein alternatives. Improved extraction technologies have allowed these proteins to compete more effectively with conventional animal- and plant-based proteins. Whole algae proteins are becoming increasingly popular due to their balanced amino acid profile and high nutrient density. Their presence is growing in sports nutrition, meal replacements, and functional snacks. Algae-derived omega-3 fatty acids are also becoming integral in health-focused product lines, especially for infant formulas and heart health supplements.

Europe Algae-based Ingredients Market held a 30% share in 2024, driven by its proactive stance on sustainability and innovation in green technologies. Regulatory frameworks across the region, such as those supporting carbon-neutral practices and plant-based product development, have created a fertile environment for adopting algae-based ingredients. Governments and private stakeholders are investing heavily in bioeconomy initiatives, encouraging the exploration of algae as a viable alternative to synthetic and animal-derived compounds. In the food and beverage sector, manufacturers are turning to algae to meet rising consumer demand for vegan, allergen-free, and nutrient-dense ingredients.

Key market participants include Corbion, Aliga Microalgae, Bioriginal Food and Science Corp, Cargill Inc, and Marine Hydrocolloids. These companies are pursuing aggressive strategies to strengthen their market position. They are focusing on sustainable production practices and developing eco-friendly, scalable cultivation systems. Several firms are investing in R&D to enhance the bioavailability and functionality of algae-based compounds. Strategic partnerships with food and cosmetic brands are being formed to expand product reach. Additionally, players are exploring clean-label formulations and launching innovative products such as algae protein powders, fortified oils, and skincare actives to appeal to a broader consumer base.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Key manufacturers

- 3.1.2 Distributors

- 3.1.3 Profit margins across the industry

- 3.1.4 Supply chain and distribution analysis

- 3.1.4.1 Raw material sourcing

- 3.1.4.2 Production and manufacturing

- 3.1.4.3 Cold chain infrastructure

- 3.1.4.4 Distribution channels

- 3.1.4.5 Supply chain challenges and optimization

- 3.1.4.6 Sustainable practices

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.3.2 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.4 Impact forces

- 3.4.1 Growth drivers

- 3.4.1.1 Government initiatives to boost algae products production

- 3.4.1.2 Increasing utilization and growing demand from nutraceutical industry

- 3.4.1.3 Technological advancements in freezing techniques

- 3.4.1.4 Rising consumer awareness and acceptance of algae-based product

- 3.4.2 Industry pitfalls & challenges

- 3.4.2.1 Cold chain infrastructure challenges

- 3.4.2.2 Environmental impact on algae cultivation

- 3.4.3 Market opportunity

- 3.4.1 Growth drivers

- 3.5 Raw material landscape

- 3.5.1 Manufacturing trends

- 3.5.2 Technology evolution

- 3.6 Pricing analysis and cost structure

- 3.6.1 Pricing trends (USD/Ton)

- 3.6.1.1 North America

- 3.6.1.2 Europe

- 3.6.1.3 Asia Pacific

- 3.6.1.4 Latin America

- 3.6.1.5 Middle East Africa

- 3.6.2 Pricing factors (raw materials, energy, labor)

- 3.6.3 Regional price variations

- 3.6.4 Cost structure breakdown

- 3.6.5 Profitability analysis

- 3.6.1 Pricing trends (USD/Ton)

- 3.7 Regulatory framework and standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Company heat map analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Recent developments & impact analysis by key players

- 4.7.1 Company categorization

- 4.7.2 Participant’s overview

- 4.7.3 Financial performance

- 4.8 Product benchmarking

Chapter 5 Market Estimates & Forecast, By Source, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Microalgae

- 5.2.1 Spirulina (arthrospira)

- 5.2.2 Chlorella

- 5.2.3 Dunaliella

- 5.2.4 Haematococcus

- 5.2.5 Schizochytrium

- 5.2.6 Nannochloropsis

- 5.2.7 Other microalgae

- 5.3 Macroalgae (seaweed)

- 5.3.1 Red seaweed (rhodophyta)

- 5.3.2 Brown seaweed (phaeophyceae)

- 5.3.3 Green seaweed (chlorophyta)

- 5.3.4 Other macroalgae

- 5.4 Cyanobacteria (blue-green algae)

- 5.4.1 Aphanizomenon flos-aquae

- 5.4.2 Other cyanobacteria

Chapter 6 Market Estimates & Forecast, By Ingredient Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Proteins & amino acids

- 6.3 Whole algae protein

- 6.3.1 Protein concentrates

- 6.3.2 Protein isolates

- 6.3.3 Peptides & amino acids

- 6.4 Lipids & fatty acids

- 6.4.1 Omega-3 fatty acids (DHA/EPA)

- 6.4.2 Polar lipids

- 6.4.3 Other lipids

- 6.5 Carbohydrates & fibers

- 6.5.1 Alginates

- 6.5.2 Carrageenan

- 6.5.3 Agar

- 6.5.4 Fucoidan

- 6.5.5 Other carbohydrates & fibers

- 6.6 Pigments & antioxidants

- 6.6.1 Chlorophyll

- 6.6.2 Phycocyanin

- 6.6.3 Astaxanthin

- 6.6.4 Fucoxanthin

- 6.6.5 Other pigments & antioxidants

- 6.7 Vitamins & minerals

- 6.8 Whole algae ingredients

- 6.9 Other ingredient types

Chapter 7 Market Estimates & Forecast, By Form, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Powder

- 7.3 Liquid

- 7.4 Gel

- 7.5 Flakes

- 7.6 Tablets & capsules

- 7.7 Other forms

Chapter 8 Market Estimates & Forecast, By Production Method, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Open pond systems

- 8.3 Closed systems

- 8.4 Photobioreactors

- 8.5 Fermenters

- 8.6 Other closed systems

- 8.7 Hybrid systems

- 8.8 Wild harvesting (for macroalgae)

- 8.9 Other production methods

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Food & beverage

- 9.2.1 Bakery & confectionery

- 9.2.2 Dairy & dairy alternatives

- 9.2.3 Meat & seafood alternatives

- 9.2.4 Beverages

- 9.2.5 Snacks & convenience foods

- 9.2.6 Sauces, dressings & condiments

- 9.2.7 Other food applications

- 9.3 Dietary supplements

- 9.3.1 Protein supplements

- 9.3.2 Omega-3 supplements

- 9.3.3 Antioxidant supplements

- 9.3.4 General health supplements

- 9.3.5 Other supplement types

- 9.4 Animal feed

- 9.4.1 Aquaculture feed

- 9.4.2 Poultry feed

- 9.4.3 Swine feed

- 9.4.4 Pet food

- 9.4.5 Other animal feed

- 9.5 Cosmetics & personal care

- 9.5.1 Skincare

- 9.5.2 Haircare

- 9.5.3 Other cosmetic applications

- 9.6 Pharmaceuticals

- 9.7 Biofuels & bioenergy

- 9.8 Other applications

Chapter 10 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Food & Beverage Industry

- 10.3 Nutraceutical Industry

- 10.4 Animal Feed Industry

- 10.5 Cosmetics & Personal Care Industry

- 10.6 Pharmaceutical Industry

- 10.7 Energy Industry

- 10.8 Other End Use Industries

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 AEP Colloids

- 12.2 AgarGel

- 12.3 Aliga Microalgae

- 12.4 Bioriginal Food & Science Corp

- 12.5 Cargill Inc.

- 12.6 Corbion

- 12.7 CP Kelco U.S. Inc

- 12.8 Gino Biotech

- 12.9 Hispanagar SA

- 12.10 KIMICA

- 12.11 Marine Hydrocolloids

- 12.12 Taiwan Chlorella Manufacturing Company

- 12.13 Triton