臨床ラボ検査の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Clinical Laboratory Tests Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750499

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

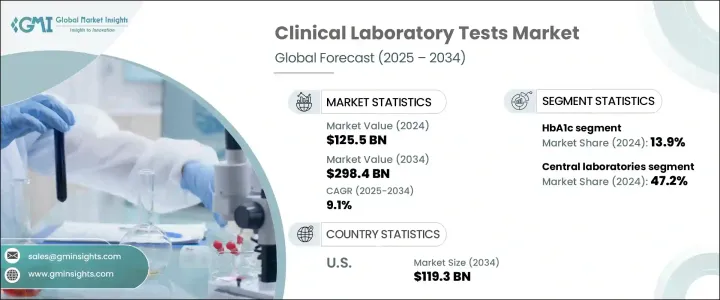

世界の臨床ラボ検査市場は、2024年に1,255億米ドルと評価され、慢性疾患の増加、世界人口の高齢化、早期発見と治療モニタリングのための診断検査への依存の高まりに後押しされ、CAGR 9.1%で成長し、2034年には2,984億米ドルに達すると予測されています。

臨床検査は医療上の意思決定に役立ち、ほとんどの診断ワークフローは試薬、分析装置、検体採取システムなどのツールに依存しています。特に先進地域における高齢化社会は、心臓病、がん、糖尿病などの慢性疾患に罹患しやすいため、検査需要に大きく寄与しています。

AIと自動化の導入により、検査の所要時間と精度が向上しました。最新の検査室は現在、機械学習とロボット工学をワークフローに組み込んで、手作業によるミスを減らし、業務効率を高め、増加するサンプル量を管理しています。個別化医療への動きは、精密な診断と多項目検査の需要を押し上げています。臨床検査は世界中で予防医療戦略の定期的な一部となっており、新興国でも定期的な健康診断がますます一般的になっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,255億米ドル |

| 予測金額 | 2,984億米ドル |

| CAGR | 9.1% |

2024年には、HbA1c検査が最大の市場シェアを占め、総売上高の13.9%を占める。これらの検査は、特に糖尿病患者の長期的な血糖コントロールのモニタリングに不可欠です。ポータブル分析装置や自動化システムなどの技術改良により、HbA1c検査はより身近で効率的なものとなっています。また、早期診断や疾病管理に対する社会的意識の高まりも、HbA1c検査の頻度を押し上げています。糖尿病患者が世界的に増加する中、定期的なモニタリングに対する需要は急増し続けており、この分野の持続的成長を牽引しています。

2024年には中央検査室部門が472億米ドルを占め、最大のシェアを占めました。これは高スループット診断能力、確立されたインフラ、病院や研究機関との強力な統合に支えられています。これらの検査施設は、遺伝子診断や分子診断を含む複雑な検査に対応できる設備を備え、幅広い地理的ネットワークで結果の一貫性を維持しています。費用対効果の高いソリューションと信頼性により、大規模な検査ニーズに適した選択肢となっています。

米国の臨床ラボ検査 2024年の市場規模は508億米ドルで、2034年には1,193億米ドルに達すると予測されています。一人当たりのヘルスケア支出が高いため、病院、診療所、研究所に最先端の診断技術が広く導入されています。慢性疾患、感染症、加齢に伴う健康状態の増加は、タイムリーで正確なラボ検査の必要性をさらに高めています。分子診断、個別化医療、早期疾患検出ツールへの依存の高まりは、全国の臨床ワークフローを再構築しています。

この分野の主要企業には、シーメンス・ヘルティニアーズ、バイオメリュー、アジレント・テクノロジー、イルミナ、サーモフィッシャーサイエンティフィック、アボット・ラボラトリーズ、ホロジック、バイオ・ラッド・ラボラトリーズ、QIAGEN、ダナハー、パーキンエルマーなどがあります。市場での存在感を高めるため、各社はヘルスケアプロバイダーとの提携、検査自動化の拡大、AIベースのプラットフォームへの投資に注力しています。また、検査メニューの多様化、小規模診断企業の買収、世界な販売網の拡大も目指しています。規制遵守、製品イノベーション、コスト効率の高いソリューションは、進化する診断状況において競争力を維持するために引き続き不可欠です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患および感染症の蔓延

- 診断技術の進歩

- 高齢化人口の増加

- 業界の潜在的リスク&課題

- 熟練した研究室スタッフの不足

- 厳しい規制シナリオ

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 国別の対応

- 業界への影響

- 供給側の影響(製造コスト)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(消費者へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(製造コスト)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 技術的情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:テストタイプ別、2021 –2034

- 主要動向

- 全血球数

- HbA1c

- 代謝パネル

- 肝臓パネル

- 腎臓パネル

- 脂質パネル

- 心臓血管パネル

- その他のテストの種類

第6章 市場推計・予測:最終用途別、2021 –2034

- 主要動向

- 中央研究所

- プライマリクリニック

- 病院

- その他の用途

第7章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- Abbott Laboratories

- Agilent Technologies

- Beckman Coulter

- Becton、Dickinson and Company

- bioMerieux

- Bio-Rad Laboratories

- F. Hoffmann-La Roche

- Grifols

- Hologic

- Illumina

- PerkinElmer

- QIAGEN

- QuidelOrtho

- Siemens Healthineers

- Thermo Fisher Scientific

目次

The Global Clinical Laboratory Tests Market was valued at USD 125.5 billion in 2024 and is estimated to grow at a CAGR of 9.1% to reach USD 298.4 billion by 2034, fueled by rising chronic disease cases, the aging global population, and the increasing reliance on diagnostic testing for early detection and treatment monitoring. Laboratory testing helps in medical decision-making, with most diagnostic workflows depending on tools like reagents, analyzers, and specimen collection systems. Aging populations, especially in developed regions, contribute significantly to testing demand due to their susceptibility to chronic illnesses such as heart disease, cancer, and diabetes.

Adoption of AI and automation has improved test turnaround time and accuracy. Modern laboratories now integrate machine learning and robotics into workflows to reduce manual errors, boost operational efficiency, and manage rising sample volumes. The move toward personalized medicine pushes demand for precise diagnostics and multi-analyte tests. Clinical testing has become a regular part of preventive healthcare strategies worldwide, and regular health screenings are becoming increasingly common, even in emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $125.5 Billion |

| Forecast Value | $298.4 Billion |

| CAGR | 9.1% |

In 2024, HbA1c tests accounted for the largest market share, contributing 13.9% of total revenue. These tests are essential for monitoring long-term blood glucose control, particularly in patients with diabetes. Technological improvements such as portable analyzers and automated systems have made HbA1c testing more accessible and efficient. Growing public awareness around early diagnosis and disease management has also pushed the frequency of these tests. With diabetes cases rising globally, demand for regular monitoring continues to surge, driving sustained growth for this segment.

The central laboratories segment held the largest share in 2024, accounting for USD 47.2 billion, supported by high-throughput diagnostic capabilities, well-established infrastructure, and strong integration with hospitals and research institutions. These labs are equipped to handle complex tests, including genetic and molecular diagnostics, and maintain consistency in results across wide geographical networks. Their cost-effective solutions and reliability make them the preferred option for large-scale testing needs.

U.S. Clinical Laboratory Tests Market was valued at USD 50.8 billion in 2024 and is projected to reach USD 119.3 billion by 2034, driven by multiple structural and technological factors. High per capita healthcare spending enables widespread integration of cutting-edge diagnostic technologies across hospitals, clinics, and research labs. The rising incidence of chronic illnesses, infectious diseases, and age-related health conditions further amplifies the need for timely and accurate laboratory testing. Increasing reliance on molecular diagnostics, personalized medicine, and early disease detection tools is reshaping clinical workflows nationwide.

Key players in this space include Siemens Healthineers, bioMerieux, Agilent Technologies, Illumina, Thermo Fisher Scientific, Abbott Laboratories, Hologic, Bio-Rad Laboratories, QIAGEN, Danaher, and PerkinElmer. To strengthen market presence, companies are focusing on partnerships with healthcare providers, expanding laboratory automation, and investing in AI-based platforms. They also aim to diversify test menus, acquire smaller diagnostic firms, and increase their global distribution networks. Regulatory compliance, product innovation, and cost-effective solutions remain critical to staying competitive in the evolving diagnostic landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic and infectious diseases

- 3.2.1.2 Advancements in diagnostic technologies

- 3.2.1.3 Growing geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Shortage of skilled laboratory personnel

- 3.2.2.2 Stringent regulatory scenario

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Complete blood count

- 5.3 HbA1c

- 5.4 Metabolic panel

- 5.5 Liver panel

- 5.6 Renal panel

- 5.7 Lipid panel

- 5.8 Cardiovascular panel

- 5.9 Other test types

Chapter 6 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Central laboratories

- 6.3 Primary clinics

- 6.4 Hospitals

- 6.5 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 Agilent Technologies

- 8.3 Beckman Coulter

- 8.4 Becton, Dickinson and Company

- 8.5 bioMerieux

- 8.6 Bio-Rad Laboratories

- 8.7 F. Hoffmann-La Roche

- 8.8 Grifols

- 8.9 Hologic

- 8.10 Illumina

- 8.11 PerkinElmer

- 8.12 QIAGEN

- 8.13 QuidelOrtho

- 8.14 Siemens Healthineers

- 8.15 Thermo Fisher Scientific

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日