セルライト治療の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Cellulite Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750336

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

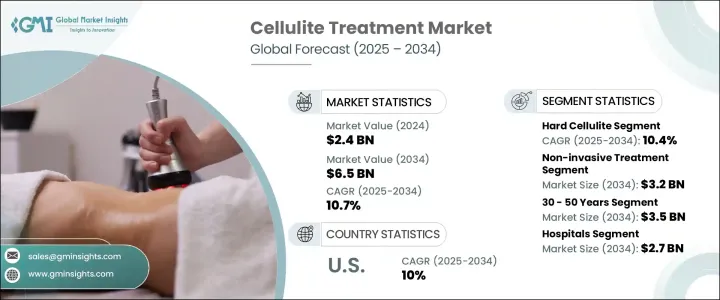

世界のセルライト治療市場は、2024年には24億米ドルと評価され、2034年にはCAGR 10.7%で成長し65億米ドルに達すると予測されています。

これは、消費者に最小限のダウンタイムでより効果的なソリューションを提供する、先進的な非侵襲的・低侵襲治療の人気が高まっていることが背景にあります。さらに、ボディの美容に関する消費者の意識の高まりと、より安全で侵襲性の低い治療への要望が、これらの処置の需要をさらに煽っています。セルライトは、一般的に大腿、臀部、腹部周辺に見られ、くぼみやシコリのある皮膚の外観をもたらす、広く美容上の悩みです。セルライトは主に女性に発生し、加齢、ホルモンバランスの乱れ、体重増加などの様々な要因によって誘発されたり悪化したりします。

加えて、座りっぱなしの日常生活、食生活の乱れ、血行不足などの生活習慣も開発の一因となります。セルライトは、脂肪沈着物が皮膚の下の結合組織を突き破って形成されるため、表面に凹凸が生じます。特に肥満や加齢の影響を受けている人々の間でセルライトの発生率が上昇しているため、セルライトを目立たなくし、より滑らかでハリのある肌を取り戻す効果的な治療に対する需要が高まっています。脂肪細胞を分解し、血流を促し、コラーゲンの生成を高めることに焦点を当てた治療が人気を集めています。これらの治療は、皮膚の下の脂肪分布を整形し、患部の全体的な質感と色調を改善することを目的としています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 24億米ドル |

| 予測金額 | 65億米ドル |

| CAGR | 10.7% |

市場は主に、非侵襲的治療、低侵襲治療、局所治療など、さまざまな治療タイプに区分されます。なかでも非侵襲性治療が最大の市場シェアを占め、CAGR 11.1%で成長し、2034年には32億米ドルに達すると予測されます。レーザー治療、音響波治療、高周波治療、超音波治療などのこれらの非外科的治療は、その無痛性、使いやすさ、回復時間の速さにより、非常に好まれています。これらは、大がかりな施術を受けずにセルライトを最小限に抑えたい人に、好ましい選択肢を提供します。非侵襲的治療は進化を続けており、効果的で快適かつ低リスクの解決策を求める消費者の需要増加に応えるため、企業はこれらの方法の改善に注力しています。

硬質セルライト分野は、2024年には11億米ドルと評価され、2034年には30億米ドルに達し、CAGR 10.4%で成長すると予想されています。硬質セルライトは、緻密な繊維組織を特徴とし、従来の治療に対する抵抗力が強いため、レーザー治療や高周波など、より高度な治療法が必要となります。活動的なライフスタイルを送る若年層における硬いセルライトの有病率の増加が、これらの特殊な治療に対する需要を牽引しています。このため、この頑固なセルライトに対処することを目的とした、革新的で効果的な治療法の開発が急増しています。

米国のセルライト治療市場は、2024年に7億6,370万米ドルと評価されたが、これは人口におけるセルライトの発生率の高さ、利用可能な治療法に対する認知度の高まり、非侵襲的な選択肢に対する強い嗜好に起因しています。さらに、米国はヘルスケアのインフラが確立されており、化粧品や美容治療に重点を置いているため、セルライト減少治療への需要が高まっています。

セルライト治療の世界市場に参入している企業は、市場での地位を強化するために、製品の革新、パートナーシップ、地理的プレゼンス拡大などの戦略を採用しています。Venus Concept社、Soliton社(AbbVie社)、Cynosure社などの企業は、効果的な治療に対する需要の高まりに対応するため、最先端技術による製品提供の強化に注力しています。ヘルスケア・プロバイダーや美容クリニックとの提携や戦略的なマーケティング・キャンペーンにより、これらの企業はリーチを拡大しています。さらに、より高度で効率的なセルライト治療を生み出すための研究開発にも投資しており、市場での競争力を維持しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 美容施術に対する意識と需要の増加

- 非侵襲性および低侵襲性技術の進歩

- 非侵襲的および低侵襲的処置への嗜好の増加

- 皮膚科・美容クリニックの拡大

- 業界の潜在的リスク&課題

- 高額な治療費

- 潜在的な副作用に関する懸念の高まり

- 厳格な規制承認

- 促進要因

- 成長可能性分析

- パイプライン分析

- テクノロジーの情勢

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:セルライトタイプ別、2021年~2034年

- 主要動向

- 硬いセルライト

- 柔らかいセルライト

- 浮腫性セルライト

第6章 市場推計・予測:治療タイプ別、2021年~2034年

- 主要動向

- 非侵襲的治療

- レーザー治療

- 音波療法

- 高周波療法

- 超音波療法

- 低侵襲治療

- サブシジョン

- クライオリポライシス

- その他の低侵襲治療

- 局所治療

- 経口サプリメント

第7章 市場推計・予測:性別別、2021年~2034年

- 主要動向

- 女性

- 男性

第8章 市場推計・予測:年齢別、2021年~2034年

- 主要動向

- 30歳未満

- 30~50歳

- 50歳以上

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 皮膚科クリニック

- 美容とウェルネスセンター

- 家庭用

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Air Sculpt

- Alma Lasers

- Bausch Health

- Bionov

- Candela

- Cutera

- Cynosure

- El En. Group

- Endo International

- Hologic

- Merz Pharma

- Mesoestetic

- Revelle Aesthetics

- Sirona Biochem

- Soliton(Abbvie)

- Ulthera

- Zimmer Aesthetics

目次

The Global Cellulite Treatment Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 10.7% to reach USD 6.5 billion by 2034, driven by the increasing popularity of advanced non-invasive and minimally invasive treatments, which offer consumers more effective solutions with minimal downtime. Additionally, heightened consumer awareness regarding body aesthetics and the desire for safer, less invasive treatments have further fueled the demand for these procedures. Cellulite is a widespread cosmetic concern, commonly seen around the thighs, hips, and abdomen, resulting in the appearance of dimpled or lumpy skin. It primarily affects women and can be triggered or worsened by various factors, such as aging, hormonal imbalances, and weight gain.

Additionally, lifestyle factors like a sedentary routine, poor diet, and insufficient circulation can contribute to its development. As cellulite forms when fat deposits push through the connective tissue beneath the skin, it creates an uneven surface appearance. With the rising incidence of cellulite, especially among those affected by obesity and the aging process, there is an increased demand for effective treatments that can reduce its visibility and restore smoother, firmer skin. Treatments that focus on breaking down fat cells, stimulating blood flow, and boosting collagen production are gaining popularity. These treatments aim to reshape the fat distribution beneath the skin, improving the overall texture and tone of the affected areas.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $6.5 Billion |

| CAGR | 10.7% |

The market is primarily segmented into various treatment types, including non-invasive, minimally invasive, and topical treatments. Among these, the non-invasive segment holds the largest market share, projected to grow at a CAGR of 11.1%, reaching USD 3.2 billion by 2034. These non-surgical treatments, such as laser therapy, acoustic wave therapy, radiofrequency therapy, and ultrasound therapy, are highly favored due to their painless nature, ease of use, and rapid recovery times. They provide a preferred option for individuals looking to minimize cellulite without undergoing extensive procedures. The non-invasive treatments continue to evolve, with companies focusing on improving these methods to meet increasing consumer demand for effective, comfortable, and low-risk solutions.

The hard cellulite segment was valued at USD 1.1 billion in 2024 and is expected to reach USD 3 billion by 2034, growing at a CAGR of 10.4%. Hard cellulite, which is characterized by dense, fibrous tissue and is more resistant to traditional treatments, requires more advanced treatment methods, such as laser therapy and radiofrequency. The increasing prevalence of hard cellulite among younger individuals who lead active lifestyles has driven demand for these specialized treatments. This has led to a surge in the development of innovative and effective therapies aimed at addressing this more stubborn form of cellulite.

U.S. Cellulite Treatment Market was valued at USD 763.7 million in 2024, attributed to the high occurrence of cellulite in the population, the growing awareness of available treatments, and the strong preference for non-invasive options. Furthermore, the U.S. benefits from a well-established healthcare infrastructure and a focus on cosmetic and aesthetic treatments, which have boosted the demand for cellulite reduction therapies.

Companies in the Global Cellulite Treatment Market are adopting strategies such as product innovation, partnerships, and expanding their geographic presence to strengthen their market position. Firms like Venus Concept, Soliton (AbbVie), and Cynosure are focusing on enhancing their product offerings with cutting-edge technology to meet the growing demand for effective treatments. Collaborations with healthcare providers and cosmetic clinics, along with strategic marketing campaigns, have enabled these companies to expand their reach. Additionally, they are investing in research and development to create more advanced and efficient cellulite treatments, ensuring they maintain a competitive edge in the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing awareness and demand for aesthetic procedures

- 3.2.1.2 Growing advancement in non-invasive and minimally invasive technologies

- 3.2.1.3 Increasing preference for non-invasive and minimally invasive procedures

- 3.2.1.4 Expansion of dermatology and aesthetic clinics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Growing concerns related to potential side effects

- 3.2.2.3 Strict regulatory approvals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pipeline analysis

- 3.5 Technology landscape

- 3.6 Regulatory landscape

- 3.7 Trump administration tariffs

- 3.7.1 Impact on trade

- 3.7.1.1 Trade volume disruptions

- 3.7.1.2 Retaliatory measures

- 3.7.2 Impact on the Industry

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.2.1.1 Price volatility in key materials

- 3.7.2.1.2 Supply chain restructuring

- 3.7.2.1.3 Production cost implications

- 3.7.2.2 Demand-side impact (selling price)

- 3.7.2.2.1 Price transmission to end markets

- 3.7.2.2.2 Market share dynamics

- 3.7.2.2.3 Consumer response patterns

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.3 Key companies impacted

- 3.7.4 Strategic industry responses

- 3.7.4.1 Supply chain reconfiguration

- 3.7.4.2 Pricing and product strategies

- 3.7.4.3 Policy engagement

- 3.7.5 Outlook and future considerations

- 3.7.1 Impact on trade

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Cellulite Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hard cellulite

- 5.3 Soft cellulite

- 5.4 Edematous cellulite

Chapter 6 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Non-invasive treatment

- 6.2.1 Laser treatment

- 6.2.2 Acoustic wave therapy

- 6.2.3 Radiofrequency therapy

- 6.2.4 Ultrasound therapy

- 6.3 Minimally invasive treatment

- 6.3.1 Subcision

- 6.3.2 Cryolipolysis

- 6.3.3 Other minimally invasive treatment

- 6.4 Topical treatments

- 6.5 Oral supplements

Chapter 7 Market Estimates and Forecast, By Gender, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Female

- 7.3 Male

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Below 30 years

- 8.3 30 - 50 years

- 8.4 Above 50 years

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Dermatology clinics

- 9.4 Beauty and wellness centers

- 9.5 Home-use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Air Sculpt

- 11.2 Alma Lasers

- 11.3 Bausch Health

- 11.4 Bionov

- 11.5 Candela

- 11.6 Cutera

- 11.7 Cynosure

- 11.8 El En. Group

- 11.9 Endo International

- 11.10 Hologic

- 11.11 Merz Pharma

- 11.12 Mesoestetic

- 11.13 Revelle Aesthetics

- 11.14 Sirona Biochem

- 11.15 Soliton (Abbvie)

- 11.16 Ulthera

- 11.17 Zimmer Aesthetics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日