|

|

市場調査レポート

商品コード

1750286

エレクトロクロミックと液晶ポリマーの市場機会と成長促進要因、産業動向分析、2025年~2034年予測Electrochromic and Liquid Crystal Polymer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| エレクトロクロミックと液晶ポリマーの市場機会と成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月13日

発行: Global Market Insights Inc.

ページ情報: 英文 300 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

エレクトロクロミックと液晶ポリマーの世界市場は、2024年には20億米ドルと評価され、自動車や建築などの産業におけるエネルギー効率の高いソリューションに対する需要の高まりにより、CAGR 8.1%で成長し、2034年には46億米ドルに達すると推定されています。

電気信号に反応して光学特性を変化させるエレクトロクロミック材料は、高度な窓技術に不可欠です。太陽エネルギーの吸収を管理し、まぶしさを最小限に抑えることで、エネルギーの最適化を可能にするスマートウィンドウは、自動車や建物において極めて重要です。これは、エネルギー管理を改善し、温室効果ガス排出量を削減するための世界の取り組みと一致し、空調の必要性を減らすのに役立ちます。産業界がより持続可能な技術を取り入れようとする中、エネルギー効率を向上させるエレクトロクロミック材料の役割は拡大し続けています。

自動車分野では、ドライバーの快適性と安全性を高めるため、バックミラーやサンルーフにエレクトロクロミック材料が使用されています。また、ADAS(先進運転支援システム)や自律走行技術の進化にも貢献しています。エレクトロクロミック材料は車内の温度を最適に保ち、省エネに貢献します。液晶ポリマー製品の需要増加は、高性能材料が必要とされる通信やエレクトロニクス産業にも後押しされています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 20億米ドル |

| 予測金額 | 46億米ドル |

| CAGR | 8.1% |

エレクトロクロミック材料分野は、2024年に9億150万米ドルの売上を計上しました。この材料は、電圧をかけると色や透明度を変える汎用性があり、窓、鏡、ディスプレイを通る熱や光の通過を制御できます。これらの材料はエネルギー効率が高く、機能的・審美的な環境におけるさまざまな用途に理想的です。PDLC(ポリマー分散型液晶)のような、より洗練された技術の開発は、より多くの色の選択肢とエネルギー効率の向上を提供することで、市場の可能性をさらに高めています。

スマート窓・ガラスは最大のアプリケーション・セグメントであり、28.3%のシェアを占めています。これらの窓は光と熱の通過を自動的に調整できるため、エネルギー効率の高い建物や自動車に対する需要の増加がこの動向を後押ししています。その結果、人工照明や空調への依存度が低下します。エレクトロクロミック・デバイスや液晶デバイスをスマート・ウィンドウに組み込むことで、世界の持続可能性目標の達成に貢献すると同時に、高級住宅や商業用不動産の快適性やプライバシーも向上します。

米国エレクトロクロミックと液晶ポリマー2024年の市場規模は4億8,280万米ドル。スマートガラスの設置に対する税額控除などの政府優遇措置が、商業ビルや住宅におけるエレクトロクロミック窓の採用促進に重要な役割を果たしています。これらの窓はエネルギー消費を約20%削減できるため、二酸化炭素排出量の削減に貢献し、持続可能なエネルギーソリューションへの移行を支援しています。

東レ、住友化学、ソルベイ、サンゴバン、AGCといったこの業界の企業は、研究開発に投資することで市場シェアを拡大することに注力しています。各社は、エレクトロクロミック製品の性能と価格の向上に取り組み、さまざまな産業で高まる需要に応えています。各社はまた、建築請負業者や自動車メーカーと戦略的パートナーシップを結び、新しい建築物や自動車モデルにこれらの先端材料が広く採用されるようにしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 市場イントロダクション

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国、2021-2024

- 主要輸入国、2021-2024

- 業界バリューチェーン分析

- 技術概要

- エレクトロクロミック材料

- 液晶ポリマー

- ポリマー分散液晶(PDLC)

- 技術の比較分析

- 市場力学

- 市場促進要因

- 市場抑制要因

- 市場機会

- 市場の課題

- 業界への影響要因

- 成長可能性分析

- 業界の潜在的リスク&課題

- 規制の枠組みと基準

- エレクトロクロミックデバイスのASTM規格

- エネルギー効率規制

- 建築基準法と認証

- 自動車業界の標準

- 製造プロセス分析

- エレクトロクロミック材料の製造

- 液晶ポリマー合成

- デバイス製造技術

- 原材料分析と調達戦略

- 価格分析

- 持続可能性と環境影響評価

- PESTEL分析

- ポーターのファイブフォース分析

第4章 競合情勢

- 市場シェア分析

- 戦略枠組み

- 合併と買収

- ジョイントベンチャーとコラボレーション

- 新製品開発

- 拡大戦略

- 競合ベンチマーキング

- ベンダー情勢

- 競合ポジショニングマトリックス

- 戦略的ダッシュボード

- テクノロジーの導入とイノベーションの評価

- 新規参入者の市場参入戦略

第5章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- エレクトロクロミック材料

- 無機エレクトロクロミック材料

- 有機エレクトロクロミック材料

- ハイブリッドエレクトロクロミック材料

- 液晶ポリマー(LCP)

- サーモトロピックLCPS

- リオトロピックLCPS

- ポリマー分散液晶(PDLC)

- 通常モードPDLC

- リバースモードPDLC

- 浮遊粒子装置(SPD)

- その他

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- スマートウィンドウとガラス

- 建築用窓

- 自動車の窓とサンルーフ

- 航空機の窓

- 船舶の窓

- 電子部品

- コネクタ

- 回路基板

- アンテナ

- マイクロエレクトロニクスパッケージ

- ディスプレイと視覚デバイス

- スマートディスプレイ

- ウェアラブルディスプレイ

- 標識と情報表示

- 自動車部品

- ミラー

- 照明システム

- センサーとコントロール

- 構造部品

- 医療機器

- 航空宇宙および防衛用途

- その他

第7章 市場規模・予測:最終用途産業別、2021年~2034年

- 主要動向

- 建設・アーキテクチャ

- 住宅

- 商業ビル

- 公共施設

- 産業施設

- 自動車・輸送

- 乗用車

- 商用車

- 電気自動車

- 鉄道と公共交通機関

- エレクトロニクスおよび通信

- 家電

- 通信機器

- コンピューティングとITハードウェア

- 5Gインフラ

- 航空宇宙および防衛

- ヘルスケアと医療

- エネルギーと発電

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他の中東・アフリカ

第9章 企業プロファイル

- Saint-Gobain

- AGC

- Gentex Corporation

- Gauzy

- Halio

- ChromoGenics

- Polytronix

- Research Frontiers

- Celanese Corporation

- Solvay

- Toray Industries

- Sumitomo Chemical Company

- Kuraray

- Murata Manufacturing

- Chiyoda Integre

- RTP Company

- SABIC

- Ynvisible Interactive

- Crown Electrokinetics

- Smart Glass Group

- Smart Films International

- Corning Incorporated

- Continental

- Panasonic Holdings Corporation

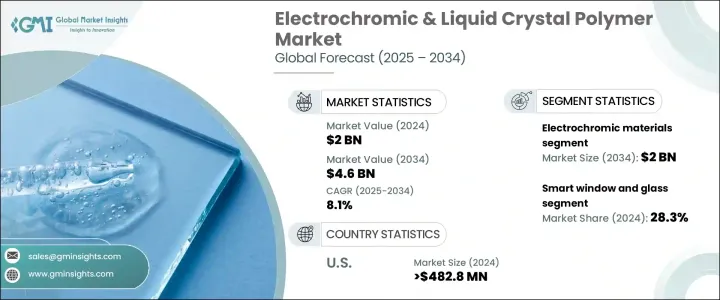

The Global Electrochromic and Liquid Crystal Polymer Market was valued at USD 2 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 4.6 billion by 2034, driven by the increasing demand for energy-efficient solutions in industries like automotive and construction. Electrochromic materials, which change their optical properties in response to electrical signals, are essential for advanced window technologies. Smart windows are crucial in vehicles and buildings, enabling energy optimization by managing solar energy absorption and minimizing glare. This helps reduce the need for air conditioning, aligning with global efforts to improve energy management and lower greenhouse gas emissions. As industries seek to incorporate more sustainable technologies, the role of electrochromic materials continues to expand in improving energy efficiency.

In the automotive sector, these materials are used in rearview mirrors and sunroofs to enhance driver comfort and safety. They also contribute to the evolution of advanced driver-assistance systems (ADAS) and autonomous driving technologies. Electrochromic materials help maintain an optimal temperature inside vehicles, contributing to energy savings. The increasing demand for liquid crystal polymer products is also fueled by the telecommunications and electronics industries, where high-performance materials are required.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 8.1% |

The electrochromic materials segment generated USD 901.5 million in 2024, attributed to the materials' versatility in changing colors or transparency when voltage is applied, allowing them to control heat and light passage through windows, mirrors, and displays. These materials are highly energy-efficient, making them ideal for various applications in both functional and aesthetic settings. The development of more sophisticated technology, such as PDLC (polymer-dispersed liquid crystal), further enhances the market's potential by offering more color options and increased energy efficiency.

Smart windows and glass hold the largest application segment, representing 28.3% share. The increasing demand for energy-efficient buildings and vehicles has driven this trend, as these windows are capable of automatically regulating light and heat passage. This results in reduced reliance on artificial lighting and air conditioning. The integration of electrochromic or liquid crystal devices in smart windows helps meet global sustainability goals while also improving comfort and privacy in high-end residential and commercial real estate.

United States Electrochromic and Liquid Crystal Polymer Market generated USD 482.8 million in 2024. Government incentives like tax credits for installing smart glass have played a key role in promoting the adoption of electrochromic windows in commercial and residential buildings. These windows can reduce energy consumption by approximately 20%, contributing to reducing carbon emissions and supporting the transition toward sustainable energy solutions.

Companies in this industry, such as Toray Industries, Sumitomo Chemical Company, Solvay, Saint-Gobain, and AGC, focus on expanding their market share by investing in research and development. They are working on enhancing the performance and affordability of electrochromic products to meet the growing demand across various industries. Companies are also forging strategic partnerships with building contractors and vehicle manufacturers to ensure widespread adoption of these advanced materials in new constructions and vehicle models.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Report scope and objectives

- 1.2 Research design and approach

- 1.3 Data collection methods

- 1.3.1 Primary research

- 1.3.2 Secondary research

- 1.4 Market estimation and forecasting methodology

- 1.5 Assumptions and limitations

- 1.6 Data validation and triangulation techniques

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Market Introduction

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021-2024 (USD Mn)

- 3.3.2 Major importing countries, 2021-2024 (USD Mn)

- 3.4 Industry value chain analysis

- 3.5 Technology overview

- 3.5.1 Electrochromic materials

- 3.5.2 Liquid crystal polymers

- 3.5.3 Polymer dispersed liquid crystals (PDLC)

- 3.5.4 Comparative analysis of technologies

- 3.6 Market dynamics

- 3.6.1 Market drivers

- 3.6.2 Market restraints

- 3.6.3 Market opportunities

- 3.6.4 Market challenges

- 3.7 Industry impact forces

- 3.7.1 Growth potential analysis

- 3.7.2 Industry pitfalls & challenges

- 3.8 Regulatory framework & standards

- 3.8.1 ASTM standards for electrochromic devices

- 3.8.2 Energy efficiency regulations

- 3.8.3 Building codes & certifications

- 3.8.4 Automotive industry standards

- 3.9 Manufacturing process analysis

- 3.9.1 Electrochromic materials production

- 3.9.2 Liquid crystal polymer synthesis

- 3.9.3 Device fabrication techniques

- 3.10 Raw material analysis & procurement strategies

- 3.11 Pricing analysis

- 3.12 Sustainability & environmental impact assessment

- 3.13 Pestle analysis

- 3.14 Porter's five forces analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis

- 4.2 Strategic framework

- 4.2.1 Mergers & acquisitions

- 4.2.2 Joint ventures & collaborations

- 4.2.3 New product developments

- 4.2.4 Expansion strategies

- 4.3 Competitive benchmarking

- 4.4 Vendor landscape

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

- 4.7 Technology adoption & innovation assessment

- 4.8 Market entry strategies for new players

Chapter 5 Market Size and Forecast, By Technology, 2021-2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Electrochromic materials

- 5.2.1 Inorganic electrochromic materials

- 5.2.2 Organic electrochromic materials

- 5.2.3 Hybrid electrochromic materials

- 5.3 Liquid crystal polymers (LCP)

- 5.3.1 Thermotropic LCPS

- 5.3.2 Lyotropic LCPS

- 5.4 Polymer dispersed liquid crystals (PDLC)

- 5.4.1 Normal mode PDLC

- 5.4.2 Reverse mode PDLC

- 5.5 Suspended particle devices (SPD)

- 5.6 Other

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Smart windows & glass

- 6.2.1 Architectural windows

- 6.2.2 Automotive windows & sunroofs

- 6.2.3 Aircraft windows

- 6.2.4 Marine windows

- 6.3 Electronic components

- 6.3.1 Connectors

- 6.3.2 Circuit boards

- 6.3.3 Antennas

- 6.3.4 Microelectronic packaging

- 6.4 Displays & visual devices

- 6.4.1 Smart displays

- 6.4.2 Wearable displays

- 6.4.3 Signage & information displays

- 6.5 Automotive components

- 6.5.1 Mirrors

- 6.5.2 Lighting systems

- 6.5.3 Sensors & controls

- 6.5.4 Structural components

- 6.6 Medical devices & equipment

- 6.7 Aerospace & defense applications

- 6.8 Other

Chapter 7 Market Size and Forecast, By End Use Industry, 2021-2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Construction & architecture

- 7.2.1 Residential buildings

- 7.2.2 Commercial buildings

- 7.2.3 Institutional buildings

- 7.2.4 Industrial facilities

- 7.3 Automotive & transportation

- 7.3.1 Passenger vehicles

- 7.3.2 Commercial vehicles

- 7.3.3 Electric vehicles

- 7.3.4 Railways & mass transit

- 7.4 Electronics & telecommunications

- 7.4.1 Consumer electronics

- 7.4.2 Telecommunications equipment

- 7.4.3 Computing & IT hardware

- 7.4.4 5g infrastructure

- 7.5 Aerospace & defense

- 7.6 Healthcare & medical

- 7.7 Energy & power generation

- 7.8 Others

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Saint-Gobain

- 9.2 AGC

- 9.3 Gentex Corporation

- 9.4 Gauzy

- 9.5 Halio

- 9.6 ChromoGenics

- 9.7 Polytronix

- 9.8 Research Frontiers

- 9.9 Celanese Corporation

- 9.10 Solvay

- 9.11 Toray Industries

- 9.12 Sumitomo Chemical Company

- 9.13 Kuraray

- 9.14 Murata Manufacturing

- 9.15 Chiyoda Integre

- 9.16 RTP Company

- 9.17 SABIC

- 9.18 Ynvisible Interactive

- 9.19 Crown Electrokinetics

- 9.20 Smart Glass Group

- 9.21 Smart Films International

- 9.22 Corning Incorporated

- 9.23 Continental

- 9.24 Panasonic Holdings Corporation