液晶ポリマー(LCP)フィルムおよびラミネート:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Liquid Crystal Polymer (LCP) Films And Laminates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690701

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

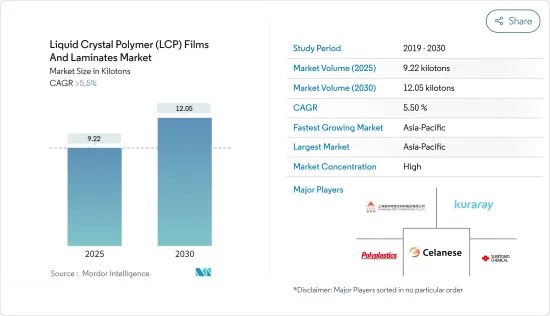

液晶ポリマー(LCP)フィルムおよびラミネート市場規模は、2025年に9.22キロトンと推定され、予測期間(2025-2030年)のCAGRは5.5%を超え、2030年には12.05キロトンに達すると予測されます。

COVID-19パンデミックは液晶ポリマー(LCP)フィルムおよびラミネート市場にマイナスの影響を与えました。全国的な封鎖と厳しい社会的遠ざけ措置により、さまざまな電子機器の製造活動が停止し、液晶ポリマー(LCP)フィルムおよびラミネート市場に影響を与えました。

しかし、液晶ポリマー(LCP)フィルムおよびラミネートのエレクトロニクス、自動車、包装用途での需要増加により、市場はその後大幅に回復しました。

主なハイライト

- 電気・電子部品の小型化需要の増加と自動車部品向け軽量材料の開発により、研究市場の需要増加が見込まれます。

- 液晶ポリマー(LCP)フィルムおよびラミネートの製造・加工コストが高いことが市場成長の妨げになると予想されます。

- ASEANとインドのエレクトロニクス市場の潜在的成長は、予測期間中に市場に成長機会をもたらすと予想されます。

- アジア太平洋地域は最大の市場であり、中国、インド、ASEAN諸国などの消費の増加により、予測期間中に最も急成長する市場になると予想されます。

液晶ポリマー(LCP)フィルムおよびラミネート市場動向

市場を独占するエレクトロニクス用途セグメント

- 液晶ポリマー(LCP)およびラミネートは、エレクトロニクス産業全体にその応用範囲を広げています。LCPフィルムは、低誘電率、高い防湿性、制御可能な熱膨張係数、高周波特性、非ハロゲン難燃性など、優れた電気的・機械的特性を備えています。

- テレワークや在宅勤務の普及が電子機器の需要を押し上げました。また、デジタル化投資の活発化によりデータ活用の高度化が進み、ソリューションサービスが拡大しました。このため、エレクトロニクス分野で使用されるLCPフィルムおよびラミネートの需要は増加すると予想されます。

- 世界のエレクトロニクス産業は著しい成長率を記録しました。日本電子情報技術産業協会(JEITA)によると、世界のエレクトロニクス・IT産業の生産額は、2021年の3兆3,600億米ドルに対し、2022年には3兆4,300億米ドルとなり、前年比1%の成長率を記録しました。さらに、2023年には前年比3%の成長率で3兆5,200億米ドルに達すると予想されています。

- アジア太平洋地域は、世界のエレクトロニクス生産の70%以上を占めています。韓国、日本、中国といった国々が電気部品を製造し、世界のさまざまな産業に供給しています。さらに、インドは2025年までに世界第5位の家電・エレクトロニクス産業になると予想されています。

- インドのエレクトロニクス・システム設計・製造(ESDM)部門は、2025年までに1,000億米ドル以上の経済価値を生み出すと予想されています。インドにおける電気・電子機器の生産は、Make in India、National Policy of Electronics、Net Zero Imports in Electronicsといった、国内製造業の成長にコミットする政府の政策により、急速に増加すると予想されています。エレクトロニクス産業の成長は、現在の研究市場を牽引すると予想されます。

- 同様に欧州では、ドイツのエレクトロニクス産業が著しい成長率を記録しました。ZVEIによると、ドイツのエレクトロニクス・デジタル産業の売上高は、前年の2,169億米ドル(2,000億ユーロ)に対し、2022年には2,435億米ドル(2,245億ユーロ)に達しました。このように、エレクトロニクス産業の成長は、同国の液晶ポリマー(LCP)フィルムおよびラミネートの市場需要を牽引すると予想されます。

- これらの要因から、予測期間中、エレクトロニクス用途分野が液晶ポリマー(LCP)フィルムおよびラミネート市場を独占すると予想されます。

市場を独占するアジア太平洋地域

- 予測期間中、アジア太平洋地域が液晶ポリマー(LCP)フィルムおよびラミネート市場を独占すると予測されます。液晶ポリマー(LCP)フィルムおよびラミネートの需要が高まっているのは、中国、日本、インドのエレクトロニクス産業と自動車産業です。

- 中国や日本などの国々では、エレクトロニクス産業が著しい成長率を記録しており、シリコーンコーティング市場を牽引しています。中国のエレクトロニクス市場は2021年に10%増加したのに対し、2022年には13%増加しました。2023年の推定成長率は7%です。

- 日本は世界最大のエレクトロニクス企業の本拠地であり、さまざまな電子機器やデバイスの生産で大きなシェアを享受しています。電子情報技術産業協会(JEITA)によると、2022年の日本のエレクトロニクス産業の総生産額は約743億米ドル(11兆1,243億円)に達し、前年から8%近く上昇しました。

- さらに、液晶ポリマー(LCP)フィルムおよびラミネートの需要は、自動車産業や輸送産業で増加しています。インドはこの地域で第2位の自動車メーカーとなっています。OICAによると、2022年の自動車生産台数は545万台に達し、2021年の439万台から24%の伸びを示しました。このように、自動車生産台数の増加は、現在の研究市場を牽引すると予想されます。

- 液晶ポリマー(LCP)フィルムは包装産業にも応用されています。2022年3月、TCPL Packaging Ltd.は軟包装工場の生産能力を倍増させ、商業生産を開始しました。同社はまた、ゴア工場に新たな生産ラインを追加し、オフセット生産能力を拡大しました。これらの生産能力拡大により、市場関係者も予想される需要増に対応する態勢を整えています。

- このような要因から、予測期間中、アジア太平洋地域が液晶ポリマー(LCP)フィルム・ラミネート市場を独占すると見られています。

液晶ポリマー(LCP)フィルムおよびラミネートの産業概要

液晶ポリマー(LCP)フィルムおよびラミネート市場は、その性質上、部分的に統合されています。市場の主なプレーヤーには、Celanese Corporation、KURARAY、Polyplastics、Sumitomo Chemical Advanced Technologies、Shanghai PERT Composites、UENO FINE CHEMICALS INDUSTRY LTDなどがある(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 電気・電子部品の小型化需要の増加

- 自動車部品の軽量化材料の開発

- その他の促進要因

- 抑制要因

- 高い製造・加工コスト

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- LCPフィルム

- LCPラミネート

- 用途

- 自動車および輸送

- エレクトロニクス

- 医療機器

- その他の用途(産業機械、包装など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- タイ

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ロシア

- トルコ

- 北欧諸国

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Celanese Corporation

- KGK Chemical Corporation

- KURARAY CO. LTD.

- Panasonic Industry Co., Ltd.

- Polyplastics Co. Ltd.

- Rogers Corporation

- RTP Company

- Sumitomo Chemical Advanced Technologies

- Syensqo

- Toray Industries Inc.

- UENO FINE CHEMICALS INDUSTRY LTD.

第7章 市場機会と今後の動向

- ASEANとインドのエレクトロニクス市場における成長の可能性

- その他の機会

目次

The Liquid Crystal Polymer Films And Laminates Market size is estimated at 9.22 kilotons in 2025, and is expected to reach 12.05 kilotons by 2030, at a CAGR of greater than 5.5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the liquid crystal polymer (LCP) films & laminates market. The nationwide lockdowns and strict social distancing measures had resulted in a halt in the manufacturing activities of various electronics, thereby affecting the market for liquid crystal polymer (LCP) films & laminates.

However, the market has recovered significantly since then, owing to the rising demand for liquid crystal polymer (LCP) films & laminates in electronics, automotive, and packaging applications.

Key Highlights

- The increasing demand for miniaturization of electrical and electronic components and the development of lightweight materials for automobile components are expected to increase demand for the studied market.

- The high manufacturing and processing costs of liquid crystal polymer (LCP) films and laminates are expected to hinder the market's growth.

- The potential growth in the ASEAN and India electronics market is expected to create opportunities for the market during the forecast period.

- Asia-Pacific region represents the largest market and is also expected to be the fastest-growing market over the forecast period, owing to the increasing consumption from countries such as China, India, and ASEAN countries.

Liquid Crystal Polymer (LCP) Films & Laminates Market Trends

Electronics Application Segment to Dominate The Market

- Liquid crystal polymers (LCP) and laminates have widened their application scope across the electronics industry. LCP films offer excellent electrical and mechanical properties, such as a low dielectric constant, high moisture barriers, a controllable thermal coefficient of expansion, high-frequency properties, and non-halogen flame-retardant characteristics.

- The spread of telework and stay-at-home demand drove up the demand for electronic equipment. Solution services grew as more investments in digitalization promoted more sophisticated data use. Thus, the demand for LCP films and laminates used in the electronics segment is expected to increase.

- The global electronics industry registered a significant growth rate. According to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was valued at USD 3.43 trillion in 2022, registering a growth rate of 1% year on year, compared to USD 3.36 trillion in 2021. Moreover, the industry is expected to reach USD 3.52 trillion, with a growth rate of 3% year on year, by 2023.

- Asia-Pacific accounts for more than 70% of global electronics production. Countries like South Korea, Japan, and China manufacture electrical components and supply them to various industries globally. Additionally, India is expected to become the world's fifth-largest consumer electronics and appliances industry by 2025.

- India's electronics system design and manufacturing (ESDM) sector is expected to generate over USD 100 billion in economic value by 2025. Electrical and electronics production in India is expected to increase rapidly due to government initiatives with policies, such as Make in India, National Policy of Electronics, and Net Zero Imports in Electronics, which offer a commitment to growth in domestic manufacturing. The growing electronics industry is expected to drive the current studied market.

- Similarly, in Europe, the German electronics industry registered a significant growth rate. According to the ZVEI, Germany's electro and digital industry turnover accounted for USD 243.5 billion (EUR 224.5 billion) in 2022 as compared to the USD 216.9 billion ( EUR 200 billion) turnover registered in the previous year. Thus, the growth in the electronics industry is expected to drive the market demand for Liquid Crystal Polymer (LCP) Films and laminates in the country.

- Owing to all these factors, the electronics application segment is expected to dominate the market for liquid crystal polymer (LCP) films & laminates during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the market for liquid crystal polymer (LCP) films & laminates during the forecast period. The rising demand for liquid crystal polymer (LCP) films & laminates is rising from the electronics and automotive industries in China, Japan, and India.

- In countries like China and Japan, the electronics industry has registered a significant growth rate, thereby driving the market for silicone coatings. The Chinese electronics market increased by 13% in 2022 compared to 2021, when the market saw a 10% rise. The estimated growth rate for 2023 is 7%.

- Japan is home to the world's largest electronics companies and enjoys a significant share in the production of various electronic equipment and devices. According to the Japan Electronics and Information Technology Industries Association (JEITA), in 2022, the total production value of the electronics industry in Japan amounted to around USD 74.3 billion (JPY 11,124.3 billion), showcasing a rise of nearly 8% from the previous year.

- Furthermore, the demand for liquid crystal polymer (LCP) films & laminates is increasing in the automotive and transportation industries. India has become the second-largest automotive vehicle manufacturer in the region. According to OICA, the total production volume of automotive vehicles reached 5.45 million units in 2022, indicating a growth of 24% as compared to 4.39 million units registered in 2021. Thus, the increasing production volume of automotive vehicles is anticipated to drive the current studied market.

- Liquid crystal polymer (LCP) films also find applications in the packaging industry. In March 2022, TCPL Packaging Ltd. doubled its flexible packaging plant capacity, which has now gone into commercial production. The company also expanded offset capacity by adding a new production line at the Goa plant. With these capacity expansions, market players are also poised to manage the expected higher demand.

- Due to all such factors, the Asia-Pacific region is expected to dominate the market for liquid crystal polymer (LCP) films and laminates during the forecast period.

Liquid Crystal Polymer (LCP) Films and Laminates Industry Overview

The liquid crystal polymer (LCP) films and laminates market is partially consolidated in nature. Some of the major players in the market include (not in any particular order) Celanese Corporation, KURARAY CO. LTD., Polyplastics Co. Ltd., Sumitomo Chemical Advanced Technologies, Shanghai PERT Composites Co. Ltd, and UENO FINE CHEMICALS INDUSTRY LTD, amongst others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Miniaturization of Electrical and Electronic Components

- 4.1.2 Development of Lightweight Materials for Automobile Components

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Manufacturing and Processing Costs

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 LCP Films

- 5.1.2 LCP Laminates

- 5.2 Application

- 5.2.1 Automotive and Transportation

- 5.2.2 Electronics

- 5.2.3 Medical Devices

- 5.2.4 Other Applications (Industrial Machinery, Packaging, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Malaysia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Turkey

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Celanese Corporation

- 6.4.2 KGK Chemical Corporation

- 6.4.3 KURARAY CO. LTD.

- 6.4.4 Panasonic Industry Co., Ltd.

- 6.4.5 Polyplastics Co. Ltd.

- 6.4.6 Rogers Corporation

- 6.4.7 RTP Company

- 6.4.8 Sumitomo Chemical Advanced Technologies

- 6.4.9 Syensqo

- 6.4.10 Toray Industries Inc.

- 6.4.11 UENO FINE CHEMICALS INDUSTRY LTD.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Potential in Growth in ASEAN and India Electronics Market

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日