ビタミンK2市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)

Vitamin K2 Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750277

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

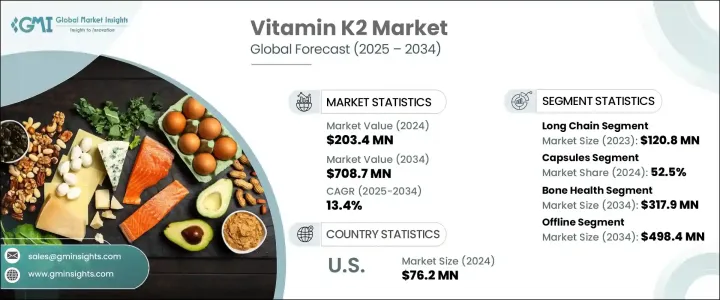

世界のビタミンK2市場は、2024年に2億340万米ドルと評価され、骨粗鬆症、心臓病、特定のがんなどの慢性疾患の増加により、13.4%のCAGRで成長し、2034年には7億870万米ドルに達すると推定されています。

特に心血管と骨の健康維持におけるビタミンK2の利点に対する意識の高まりが、あらゆる年齢層におけるサプリメント消費の増加に大きな役割を果たしています。より多くの消費者が栄養と予防医療に注目する中、ターゲットとなるサプリメントの需要は増加の一途をたどっています。骨密度の健康や骨粗鬆症のような症状の管理が重視されるようになったことも、ビタミンK2製品の消費を加速させています。

さらに、新生児のビタミンK欠乏症、特に晩発性出血のリスクをめぐる医学的懸念の高まりにより、医療当局は出生時のサプリメント摂取の推奨を強化しています。このため、小児医療におけるビタミンK2の使用は増加し、乳幼児の健康に焦点を当てたセグメントが急速に立ち上がりつつあります。乳幼児期の栄養の重要性に対する保護者や介護者の意識が高まるにつれ、乳幼児向けに調整された安全で効果的、かつ忍容性の高いビタミンK2製剤に対する需要が拡大しています。小児用サプリメントは現在、点滴や内服液のような、投与が容易で新生児のニーズに特化したより優しい形態で提供されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 2億340万米ドル |

| 市場規模予測 | 7億870万米ドル |

| CAGR | 13.4% |

長鎖型であるMK-7は、その優れた吸収性と体内での半減期の長さから、2024年の製品カテゴリーを支配しました。MK-7は、骨脆弱性の管理や心血管リスクの低減に好んで使用する医療専門家の間で信頼を得ています。骨折の予防と骨密度の改善におけるMK-7の役割を支持する臨床調査の増加は、特に自然な解決策を求める高齢者の間で、その人気をさらに後押ししています。オーガニックで植物由来のサプリメントに対する認識が高まるにつれ、天然成分由来のMK-7に対する需要も増加の一途をたどっています。

剤形別ではカプセルが市場をリードし、2024年のシェアは52.5%でした。カプセルの処方における柔軟性と吸収率の高さが、この成長に寄与しています。ソフトジェルは、ビタミンK2のような脂溶性栄養素のバイオアベイラビリティを向上させる能力が高く評価されており、コンプライアンス向上と迅速な作用が期待されています。また、保健当局によるソフトジェルフォーマットに対する規制上の裏付けも、市販サプリメントでの使用拡大を後押ししています。

米国のビタミンK2市場は、2024年には7,620万米ドルと評価され、特に高齢者の間で骨の健康に対する関心が高まり、幅広い啓蒙キャンペーンが行われています。オンライン販売チャネルの成長により、ビタミンK2製品がより身近になり、消費者は幅広い選択肢と便利な配送オプションを手に入れることができます。さらに、骨や心臓の問題を予防する役割について一般市民を教育する取り組みが、同国での市場拡大を引き続き後押ししています。

Zenith Nutrition、Carlyle Nutritionals、Doctor's Best、Health Veda Organics、Vlado's Himalayan Organics、Amway Nutrilite、NattoPharma、Pharma Cure Laboratories、Kappa Biosciences(Balchem Corporation)、WOW Lifesciences、Smarter Vitamins、Innovix Labs、Phi Naturals、Mary Ruth OrganicsといったビタミンK2世界市場の主要企業は、市場での地位を高めるために戦略的アプローチを採用しています。これには、クリーンラベルやオーガニック製品の開発、健康強調表示を検証するための科学調査への投資、デジタルでのプレゼンス拡大、世界なリーチを拡大するための流通パートナーシップの形成などが含まれます。また、バイオアベイラビリティ(生物学的利用能)の向上や独自の送達形態による製品の差別化にも注力しています。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 高齢化と生活習慣病の増加

- 骨と心臓血管の健康に対する意識の高まり

- 予防医療への移行の増加

- 業界の潜在的リスクと課題

- 規制上の課題と品質に関する懸念

- 代替製品の入手可能性

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 貿易への影響

- ポーターのファイブフォース分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業別の市場シェア分析

- 主要企業の競合分析

- 競合ポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品種類別(2021~2034年)

- 主要動向

- 短鎖型(MK--4)

- 長鎖型(MK-7)

第6章 市場推計・予測:剤形別(2021~2034年)

- 主要動向

- カプセル

- タブレット

- ドロップ

- その他の剤形

第7章 市場推計・予測:適応症別(2021~2034年)

- 主要動向

- 骨の健康

- 心臓の健康

- 血液凝固

- その他の適応症

第8章 市場推計・予測:流通チャネル別(2021~2034年)

- 主要動向

- オフライン

- 薬局・ドラッグストア

- スーパーマーケット/ハイパーマーケット

- その他のオフラインストア

- オンライン

第9章 市場推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Amway Nutrilite

- Carlyle Nutritionals

- Doctor's Best

- Health Veda Organics

- Innovix labs

- Kappa Biosciences(Balchem Corporation)

- Mary Ruth Organics

- NattoPharma

- Pharma Cure Laboratories

- Phi Naturals

- Smarter Vitamins

- Vlado's Himalayan Organics

- WOW Lifesciences

- Zenith Nutrition

目次

The Global Vitamin K2 Market was valued at USD 203.4 million in 2024 and is estimated to grow at a CAGR of 13.4% to reach USD 708.7 million by 2034, driven by the rising occurrence of chronic illnesses such as osteoporosis, heart disease, and certain cancers. The growing awareness of vitamin K2's benefits, especially in maintaining cardiovascular and bone health, has played a major role in increasing supplement consumption across all age groups. As more consumers focus on nutrition and preventive care, demand for targeted supplements continues to rise. The increased emphasis on bone density health and the management of conditions like osteoporosis is also accelerating the uptake of vitamin K2 products.

Furthermore, growing medical concern surrounding vitamin K deficiency in newborns, particularly the risk of late-onset bleeding, have prompted healthcare authorities to strengthen recommendations for supplementation at birth. This has led to an uptick in the use of vitamin K2 in pediatric care, opening a rapidly emerging segment focused on infant health. As awareness increases among parents and caregivers about the importance of early-life nutrition, the demand for safe, effective, and well-tolerated vitamin K2 formulations tailored for infants is expanding. Pediatric supplements are now being offered in gentler forms such as drops or oral solutions, which are easy to administer and designed specifically for neonatal needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $203.4 million |

| Forecast Value | $708.7 million |

| CAGR | 13.4% |

The long-chain form, MK-7, dominated the product category in 2024 due to its superior absorption and extended half-life in the body. MK-7 has gained trust among healthcare professionals who now prefer it for managing bone fragility and reducing cardiovascular risk. Increased clinical research supporting the role of MK-7 in preventing fractures and improving bone mineral density has further propelled its popularity, particularly among aging adults seeking natural solutions. As awareness of organic, plant-based supplements grows, demand for MK-7 sourced from natural ingredients continues to rise.

The capsules segment led the market in terms of dosage form, holding 52.5% share in 2024. The flexibility in formulating capsules, combined with their high absorption rate, has contributed to this growth. Soft gel variants are praised for their ability to improve the bioavailability of fat-soluble nutrients like vitamin K2, resulting in better compliance and faster action. Regulatory backing for soft gel formats from health authorities also supports their expanding use in over-the-counter supplements.

United States Vitamin K2 Market was valued at USD 76.2 million in 2024, driven by the rising interest in bone health, especially among older adults, alongside broader awareness campaigns. The growth of online sales channels has made vitamin K2 products more accessible, offering consumers a wider selection and convenient delivery options. Additionally, efforts to educate the public on the role in preventing bone and heart issues continue to drive market expansion in the country.

Key players in the Global Vitamin K2 Market such as Zenith Nutrition, Carlyle Nutritionals, Doctor's Best, Health Veda Organics, Vlado's Himalayan Organics, Amway Nutrilite, NattoPharma, Pharma Cure Laboratories, Kappa Biosciences (Balchem Corporation), WOW Lifesciences, Smarter Vitamins, Innovix Labs, Phi Naturals, and Mary Ruth Organics are employing strategic approaches to enhance their market position. These include the development of clean-label and organic products, investment in scientific research to validate health claims, expanding their digital presence, and forming distribution partnerships to boost global reach. Many also focus on product differentiation through enhanced bioavailability and unique delivery forms.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing aging population and lifestyle related disorders

- 3.2.1.2 Rising awareness of bone and cardiovascular health

- 3.2.1.3 Increasing shift toward preventive healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory challenges and quality concerns

- 3.2.2.2 Availability of alternative products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Short chain (MK--4)

- 5.3 Long chain (MK-7)

Chapter 6 Market Estimates and Forecast, By Dosage Form, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Capsules

- 6.3 Tablets

- 6.4 Drops

- 6.5 Other dosage form

Chapter 7 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Bone health

- 7.3 Heart health

- 7.4 Blood clotting

- 7.5 Other indications

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Offline

- 8.2.1 Pharmacies and drug stores

- 8.2.2 Supermarkets/ hypermarkets

- 8.2.3 Other offline stores

- 8.3 Online

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amway Nutrilite

- 10.2 Carlyle Nutritionals

- 10.3 Doctor's Best

- 10.4 Health Veda Organics

- 10.5 Innovix labs

- 10.6 Kappa Biosciences (Balchem Corporation)

- 10.7 Mary Ruth Organics

- 10.8 NattoPharma

- 10.9 Pharma Cure Laboratories

- 10.10 Phi Naturals

- 10.11 Smarter Vitamins

- 10.12 Vlado's Himalayan Organics

- 10.13 WOW Lifesciences

- 10.14 Zenith Nutrition

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日